| ON DECK FOR FRIDAY, MAY 3 |

KEY POINTS:

- Apple lends a constructive tone to risk assets…

- …for nonfarm payrolls to make or break

- Leading indicators point to another solid US jobs report

- Norges Bank pushes out rate cut guidance

- ISM-services, Fed-speak to close it all out

Leafs versus Boston, Game 7. Saturday night. Who cares about the rest of what follows!

In case you do, markets are starting off in risk-on fashion with equities broadly higher and the dollar broadly softer. Sovereign bond yields are little changed with a slight bid across EGBs and the longer ends in US Ts and gilts. Oil is flat and precious metals are a touch softer.

Apple’s after-market earnings are helping market sentiment on the combination of the results, a hike in dividend and stock buybacks.

Norges Bank Pushes Out Cut Guidance

Overnight developments were very light. Norges Bank offers a loose reference for other central banks like the BoC that are significantly influenced by commodity markets. Norges held at 4.5% as universally expected but also sounded like it is in less of a rush to ease which many had expected. New forecasts are due with the June 20th decision, but for now, the verbal guidance pushed out prior guidance for when to expect easing and retained bidirectional willingness to tighten or ease depending on the data. Key points included:

“….the policy rate will likely be kept at today’s level for some time ahead.”

“Price inflation is slowing but is still markedly above target. Business costs have increased sharply in recent years, and high wage growth and a weaker krone are contributing to keeping inflation elevated.”

“The data so far could suggest that a tight monetary policy stance may be needed for somewhat longer than previously envisaged.” Recall that at the March meeting they had said “the policy rate will be held steady in the period to autumn before it is gradually lowered.”

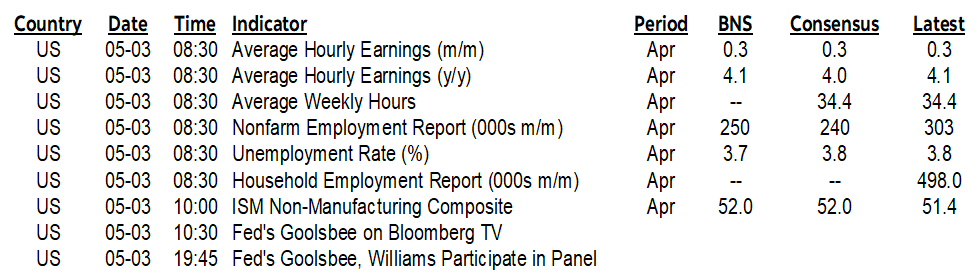

Nonfarm Payrolls Preview

Nonfarm payrolls will dominate the rest of the global market session. Job growth has been on fire this year. 303k nonfarm payroll positions were created in March after 270k in February and 256k in January. That average 276k monthly pace in Q1 picked up from 212k in Q4 which itself was lifted by the start of the acceleration with December’s 290k rise.

Most advance readings suggest ongoing, resilient hiring at a fairly brisk pace. Here are highlights of expectations for the change in payrolls and other metrics:

Scotia: 250k

Consensus median: 240k

Consensus mean: 234k (little skewness)

High-low: 280k / 145k (most within 200–270k

Std Dev: 28k

90% confidence interval: +/-130k

UR: 3.8% unchanged / Scotia 3.7%

Wages: 0.3% m/m SA

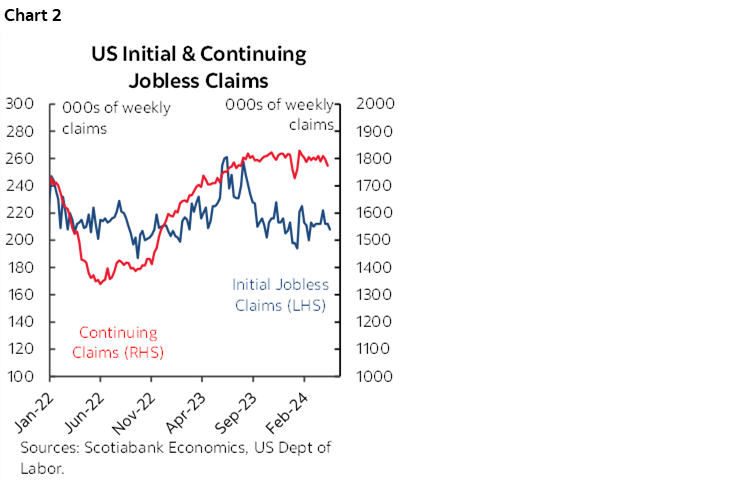

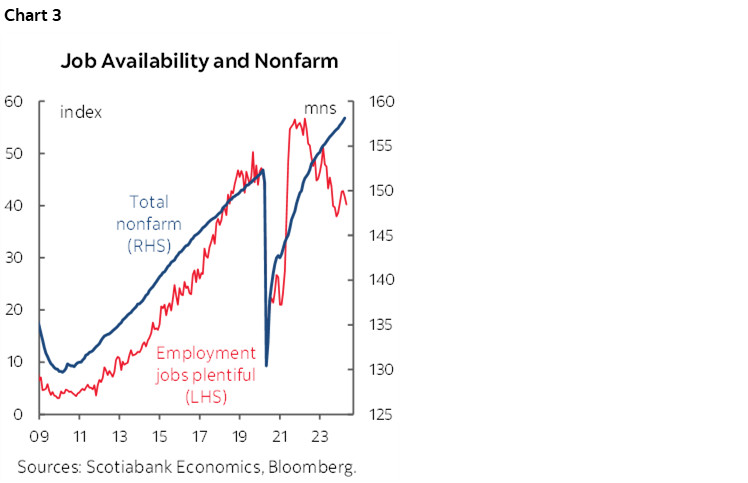

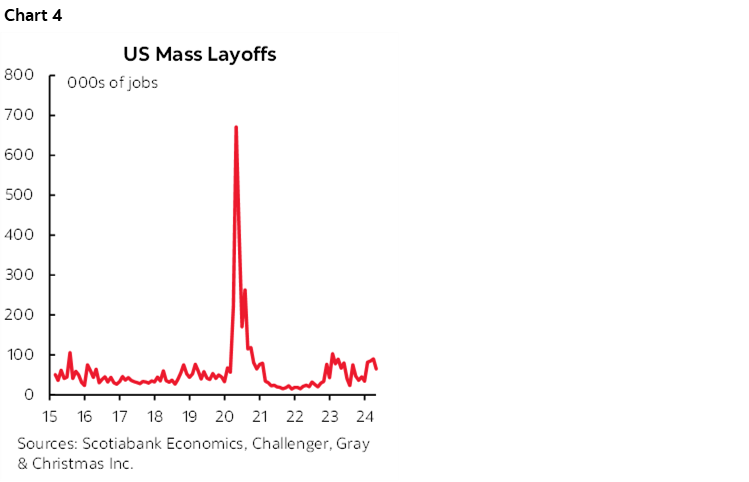

Leading indicators are mixed but generally point to a still highly resilient US job market.

- JOLTS job openings fell in March either because of solid job growth and/or fewer postings to fill into April (chart 1).

- initial jobless claims remain low (chart 2).

- consumer confidence jobs plentiful fell 1.5 points to 40.2 (chart 3).

- layoffs eased to the lowest level since December (chart 4).

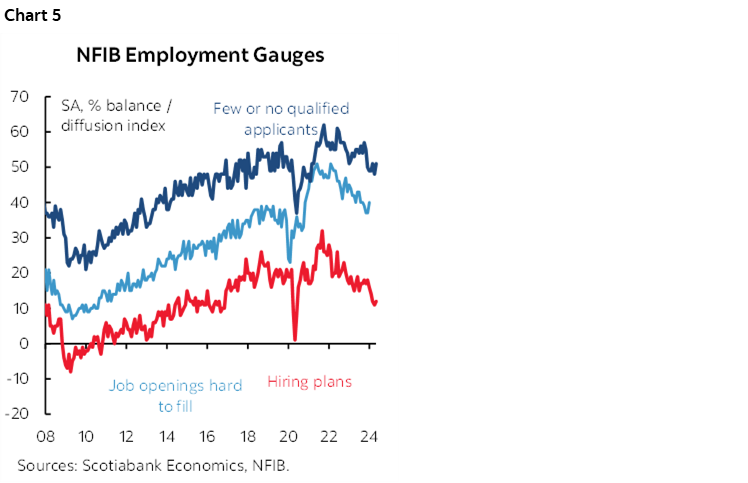

- NFIB small business hiring plans increased a touch but remain on a downward trend (chart 5).

- NFIB small business job openings hard to fill went up 3 points to the highest since December (chart 5 again).

- ISM-mfrg employment increased 1.2 points but is still contracting

- ADP payrolls were solid at 192k

No Canadian Jobs This Time

Remember that Canada’s jobs report is off-cycle this time and arrives next Friday. I went with +25k for that one.

ISM-services and Fed-Speak

The last words will go to ISM-services for April (10amET) that could be impactful with most expecting a stable to slightly improved reading, and Chicago Fed President Goolsbee (10:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.