| ON DECK FOR WEDNESDAY, MAY 29 |

KEY POINTS:

- Bonds and stocks extend cheapening bias

- Kashkari bombed US Treasury auctions with more ahead today...

- ...but markets need to update their bond market playbooks if Trump gets re-elected

- WTI crosses above $80 for first time this month

- Australian CPI surprises higher again, RBA priced for a very long hold

- Bonds unimpressed by German CPI

- More US, Canadian auctions on tap after yesterday’s weak US auctions

- Mixed Canadian bank earnings

- Is Freeland rolling a Trojan Horse to the BoC’s gates?

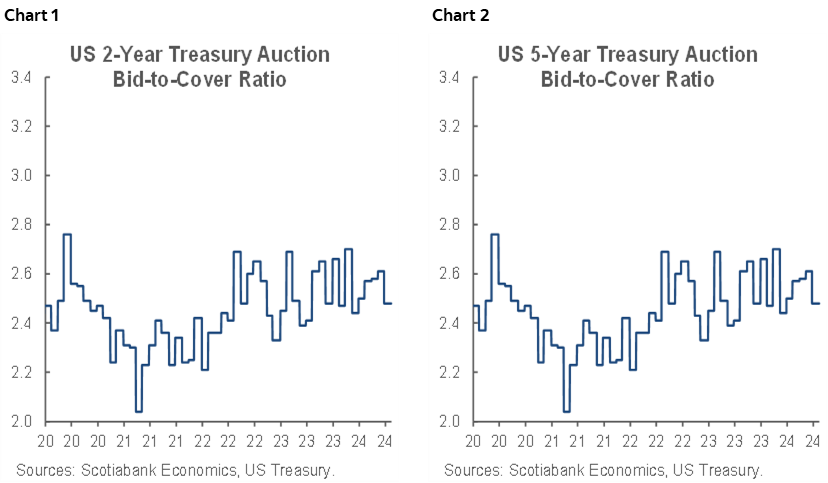

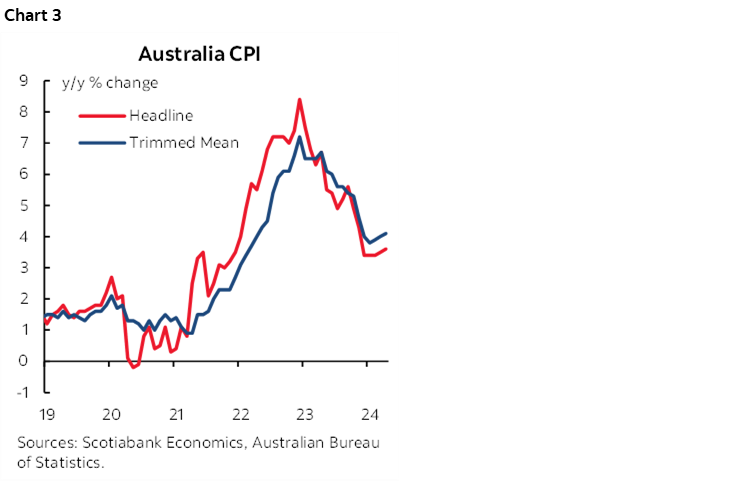

Sovereign bonds and equities are mildly cheaper this morning and the dollar is stronger with most of the moves being an extension of yesterday’s sell off that was driven by strong US data (consumer confidence), soft Treasury auctions and Fed-speak (Kashkari). More auctions are on tap today that will further test appetite for US debt after yesterday’s 2s bid-to-cover fell to 2.41 from 2.66 the last time, and the 5s bid-to-cover fell to 2.3 from 2.39. Those are hardly disasters (charts 1, 2) but reflected Kashkari’s comments that low probability hikes still remain on the table for him and an “indefinite” pause is possible. He spoke just hours ahead of the auctions. I’m pretty sure Treasury won’t be sending Kashkari a box of chocolates and a bouquet of roses today and have a real problem with Fed officials who talk too much torpedoing debt sales.

Still, all of this is child’s play compared to what could happen if Trump gets elected. He talks a lot, so who knows what he might actually do, but if he delivers on tax cuts for everyone and funds them with deficits then the US deficit-to-GDP ratio of about 6% now would be set to increase to its biggest imbalance outside of crisis points like the GFC and pandemic. Don’t like US 10s at 4.56%? Try 6%++. Is the 30-year fixed mortgage rate that’s well over 7% hurting? Starting thinking double digits in your scenarios. The NY money folks who still support Trump have to update their playbooks and stop thinking it’s the same bond market it was circa 2016. Today’s focus is all about inflation risk and supply pressures.

Across other developments, Australia’s curve got slammed by higher than expected inflation (again) that has markets thinking the RBA is on a very long pause, while German headline inflation was a little softer than expected and markets didn’t really care. Higher oil prices are negating some of the German sentiment as WTI crossed above US$80 with another gain this morning. Canadian bank earnings are disappointing this morning.

RBA Priced for Extended Hold

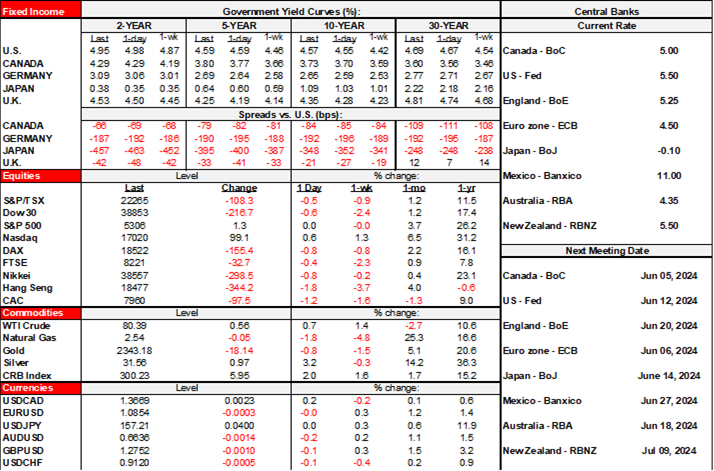

Australian yields were up by double digits with 2s 11bps cheaper through 10s being 14bps cheaper in the wake of another upside surprise in CPI for April. CPI increased by 3.6% y/y (3.5% prior, 3.4% consensus). Trimmed mean CPI increased to 4.1% y/y from 4% prior which is the highest since November (chart 3). This extends the pattern of upside surprises after Q1 figures surprised higher on April 23rd when trimmed mean CPI was up by 1% q/q (0.8% consensus) and weighted median CPI increased by 1.1% q/q (0.9% consensus), both nonannualized.

This was the last inflation report before the June 18th RBA decision. Q1 GDP and employment figures are also ahead of that meeting. Futures are pricing no rate change this year and wiped out about 12bps of cuts by year-end post-CPI. Markets are only pricing just over a quarter point cumulative cut two-years out from now.

Markets Ignored Weaker than Expected German CPI

German CPI landed at 0.1% m/m (0.2% consensus) with the EU-harmonized measure on the screws at 0.2%. Individual states had previously reported soft figures earlier this morning. Hesse, North Rhine Westphalia and Brandenburg all posted 0% m/m change in CPI, Bavaria and Saxony landed at 0.1% and Baden Wuerttemberg registered a 0.2% pop.

When the German states released the soft figures, it temporarily drove the German 2-year yield about 3bps lower, but all of that has since been reversed toward mild net cheapening in bear steepener fashion across EGBs this morning.

The German figures kick off the path to Friday’s Eurozone tally. We’ll get Italy and Spain tomorrow such that there should be little residual market risk by the time France and the Eurozone tally land on Friday.

The figures are unlikely to impact expectations for next week’s ECB meeting. ECB officials seem fairly committed to a June cut and haven’t done much to lean against pricing despite strong wage settlements and a mildly rebounding economy. Further, they haven’t even been acknowledging the fact that January’s m/m core NSA reading was less of a seasonally unadjusted decline than normal for the month, February’s m/m core NSA reading was the second hottest February on record and then March was in line average months of March. Trend core inflationary pressures have not gone away in the Eurozone.

More Auctions on Tap

More auctions are on tap today including US 2yr FRNs (11:30amET) and 7s (1pmET) plus Canada 30s (12pmET) are on tap. Canadian 10s30s remain kinked as auction supply can’t keep up with demand.

Canadian bank earnings continue to arrive. BMO posted a large miss with adjusted EPS at C$2.59 ($2.77 consensus). National Bank posted a notable beat with adjusted EPS at C$2.54 ($2.41 consensus).

Other than auctions, the rest of the N.A. session faces little macro calendar-based risk. US weekly mortgage applications fell by 5.7% w/w last week mostly due to refis (-13.6%) but also a third consecutive mild drop in purchase applications (-1.1% w/w). The Richmond Fed’s manufacturing index will further inform ISM-manufacturing expectations. NY Fed’s Williams speaks at 1:45pmET and he’s usually a more circumspect and careful speaker than, say, Kashkari. The Fed’s Beige Book lands at 2pmET, but few still care in the age in which Fed officials simply talk too much.

OTTAWA’S TROJAN HORSE GIFT TO THE BANK OF CANADA

Canadian Finance Minister Freeland says she’s done everything right to set up the BoC for rate cuts. Her exact words yesterday were that she has “been very mindful of acting in such a way that would create conditions that support the decline in inflation, or creating conditions that would make it possible for the bank to bring interest rates down.” There are four cautions here.

For one, because of front-loaded spending in prior announcements and the recent Budget, her government is still part of the cabal of Canadian governments across all levels that is adding ongoing fiscal stimulus long after it is no longer needed. The BoC’s own April forecasts showed government spending adding 0.7ppts to growth in each of this year and next before incorporating the Federal Budget but after including the effects of the provincial budgets. That number may push a little higher in the July MPR when it incorporates the Federal budget. Federal program spending is on a long-term upward path with much of that front-loaded in prior announcements. The proposed hike in capital gains taxes won’t materially offset this spending surge especially if its guesstimated revenues are spent later on rather than going toward a lower deficit as some appear to assume, while also assuming that the hike actually sees the light of day pending still missing legislation. Ongoing fiscal easing is fighting prospects for monetary easing and so Freeland’s halo is a touch tilted.

A second caution is that the ‘conditions’ to which she refers may include soft core inflation this year. If so, then we need to be very careful this soft patch proves to be a durable one. The government’s efforts to apply pressures on grocers and telecommunications companies to reduce prices are very likely yielding only temporary influences. Just like temporary influences from El Nino on price categories like clothing and footwear and airfare. C-suite bullying by government will eventually be overcome by the need to focus on shareholders because if we extrapolate the price declines in categories like internet services and cell phone services then they’ll soon become basically free.

A third caution is that the government’s other initiatives to combat inflation are conflicting and at a minimum are not bearing fruit and very possibly never will. They seek to build more homes, but with an unattainable target of about 4 million homes built by 2031 when Canada might see at best half that number being built. They have announced plans to curtail temporary immigration and hence bring population growth down to 1% or so by next year, but this requires agreement with provinces and other stakeholders such as educational institutions and such agreement has yet to be achieved. In the meantime, population continues to expand very rapidly, permanent resident immigration targets remain high, and the housing shortfall that existed before the surge in immigration is being compounded by runaway population growth that is funnelling into rental markets that have no supply to offer.

The bigger caution, however, is that Freeland and Co are very possibly laying a trap for the Bank of Canada in my opinion. They’re pushing a Trojan Horse to the front door of 234 Wellington Street. Inside this apparent gift that is comprised of the aforementioned questionable efforts lurks an army of Liberal and NDP strategists and free spenders eyeing near-certain electoral disaster next year given current moribund polling numbers. So, offer the illusory gift of helping out the BoC now while beseeching the BoC to take the bait and begin cutting now with a probably fake promise that fiscal policy will be prudent going forward, scout’s honour, whether boy or girl. Then, come the Fall update or Winter Budget, spring even more fiscal stimulus with monetary and fiscal stimulus combining to ignite the economy into 2025. Why do I think so?

Because show me a government that spends less into an election when it’s as down in the dumps as this one is according to pollsters! All deficit and issuance projections at this stage are to be taken with a mountain of salt. There are very decent odds that we’ll see fiscal policy driven by acts of desperation if the Liberal/NDP government’s polling remains this bad. All desperate governments do so across all political stripes.

The Bank of Canada must keep in mind the prospect for further fiscal easing and avoid walking blindly into a trap of combined aggressive fiscal and monetary easing that could reignite inflationary pressures all over again. After hard fought efforts to bring inflation risk down, the Feds may be setting a trap for the BoC to be complicit in driving renewed risk all over again. In my opinion, the government wouldn’t much care about the consequences to Canadians after their heavy spending and excessive immigration contributed to the pandemic-era’s inflation as the government’s sole focus will be upon staying in power. This awareness should either get reflected in great caution around when to begin easing and at what pace, and/or by thinking about the distinct possibility that monetary easing stops in its tracks if Ottawa heaps on even more fiscal stimulus into an election year.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.