| ON DECK FOR TUESDAY, MAY 28 |

KEY POINTS:

- US Ts and gilts play catch-up post-holidays

- Oil continues to rise on OPEC+ speculation, tensions

- The ECB will welcome two-handled inflation expectations

- Will US consumer confidence follow UofM higher?

- Fed- and ECB-speak offers nothing new, so far

- Canadian producer prices on tap

- Hooray for Canadian bank earnings!!

US Treasuries and particularly gilts are slightly outperforming as they catch up to yesterday’s rally in EGBs as expected following yesterday’s ECB comments that drove richer EGBs across benchmarks. Villeroy had remarked that a cut in July after cutting in June shouldn’t be ruled out. Oil prices continue to rally on speculation toward the outcome of Saturday’s OPEC+ meeting; WTI was up by about a buck yesterday and another buck today to about US$79.

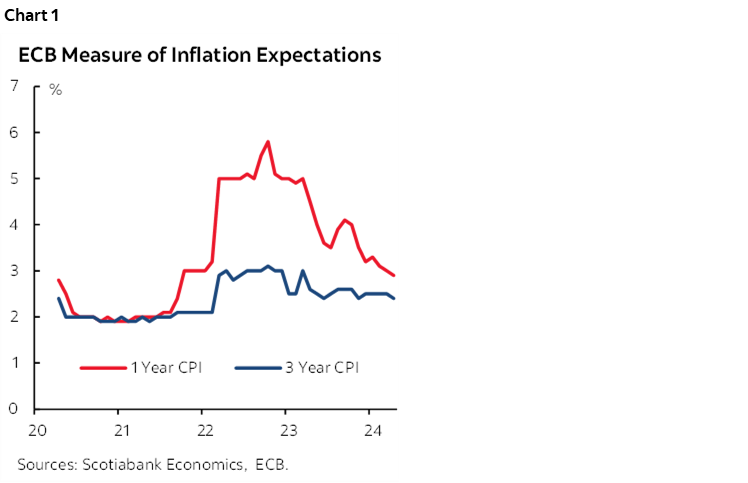

Eurozone Inflation Expectations Converge

Both of the ECB’s measures of inflation expectations are now two-handled (chart 1). The 1-year consumer gauge fell a tick to 2.9% in April and the 3-year also fell a tick to 2.4%. There was no material market reaction. Further convergence of the measures toward a two-handled pace will be welcomed by ECB officials into their decision and guidance one week from Thursday.

Little Impact So Far from Fed- and ECB-Speak

Comments from the Fed’s Bowman, Kashkari, and Mester offered nothing new. A little more Fed-speak is on tap, but they can’t possibly have much to say that is new or isn’t priced as we await Friday’s PCE and the following Friday’s nonfarm payrolls plus perhaps a mild expected downward revision to Q1 GDP on Thursday. We’ll also hear from Kashkari again (9:55amET) and both Cook and Daly (1:05pmET).

The day’s ECB speakers are so far offering nothing new (Schnabel) with others (Centeno and Knot) on the docket. Key is whether others join or contradict Villeroy’s openness to back-to-back cuts after ECB Chief Econ Lane sounded more cautious yesterday morning. Centeno (7amET) and Knot (9:15amET) are on tap.

Will US Consumer Confidence Following UMich?

Consensus expects a mild down tick for US consumer confidence (10amET). I’m among the minority of forecasters thinking we could see a slight further gain in keeping with UofM sentiment’s 1.7 point jump last Friday. Does it matter? Well yes to markets as surprises can be impactful, but I always put more emphasis upon how people actually act in terms of spending behaviour than what they say which can be highly reactionary.

Canadian Producer Prices to Post Sizeable Jumps

Not much is expected by way of market effects from Canadian producer prices (8:30amET) but they could fan inflation risk further up the supply chain. They rarely garner the same influence as either CPI or producer price measures in other countries. The raw materials index reflects mostly known info from commodity prices and is therefore the least impactful measure; it is likely to post another sharp jump driven in part by energy prices during April. The industrial price index is also likely to post another significant rise but is not well connected to CPI and reflects very different drivers.

Hooray for Canadian Bank Earnings!

BNS (obviously my employer) Q2 earnings either slightly beat (EPS, ROE, revenues) or met (provisions) analysts’ expectations. Adjusted EPS landed at $1.58, two cents above consensus. Let’s see the reaction into the open after the share price gained a bit yesterday. BMO and National are due out tomorrow followed by RBC and CIBC on Thursday and then Laurentian and Canadian Western Bank on Friday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.