| ON DECK FOR FRIDAY, MAY 17 |

KEY POINTS:

- Curves mildly cheapen on Fed– and ECB-speak

- Chinese equities rally in response to a package of property market measures

- Reasons to be skeptical toward what China announced

- Chinese macro readings were mixed

- More Fed-speak on tap today

- Canadian bond markets shut early today ahead of Victoria Day

The sound of crickets chirping away will take Canadian bond markets into an early close at 1pmET today ahead of the Victoria Day long weekend. There is no early close in equities (or Economics!). China is a focal point as a property market package was introduced on the heels of mixed data. The yuan initially reacted to the package by appreciating a touch, but then reversed all of that perhaps on a combination of second thoughts and broad USD strength. Chinese stock indices rallied by about 1% across the Shanghai, Shenzhen and Hang Seng composites. I’m not optimistic that China’s package will achieve material success.

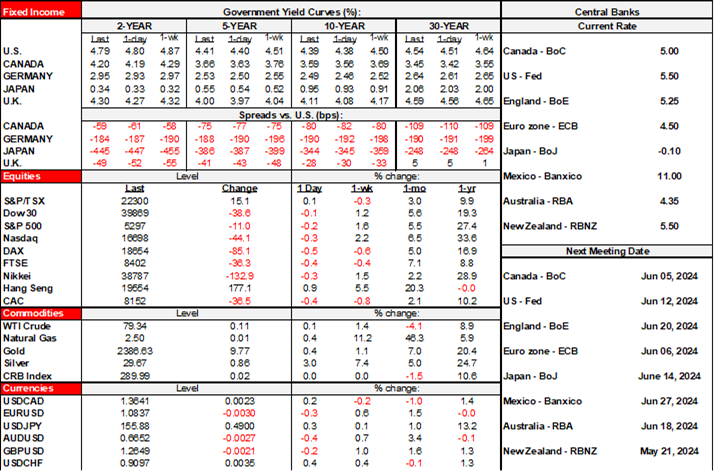

Fed- and ECB-speak are motivating slight curve cheapening and small reductions in rate cut pricing. Yesterday’s remarks by Fed-speakers were not terribly new, but reinforced the notion that they are in no rush to cut. ECB Executive Board Member Schnabel said “a rate cut in July does not seem warranted” as she leaned against going back-to-back in June and July.

China’s property market measures included the following steps:

- minimum down payments were cut by five percentage points to 15% for first-time home buyers and 25% for second homes.

- the minimum mortgage rate floor has been eliminated. Progressive steps to lower the floor have contributed to lowering the rate from about 5½% in early 2022 to 3.7% in 2024Q1 and it may go lower yet.

- Local governments are advised to buy unsold new homes and convert them to affordable housing. The PBOC will provide 300 billion yuan (about US$42B) of funding to 21 state lenders at 1.75% in order to lend to regional state-owned enterprises across local governments.

Will it work? Does it pose inflation risk to the world economy as some headlines are screaming? We’ll see, but I’m skeptical. When combined with earlier efforts to pressure banks to lower their loan spreads, a risk is that the willingness to lend will erode as the reward goes down and the risk goes up.

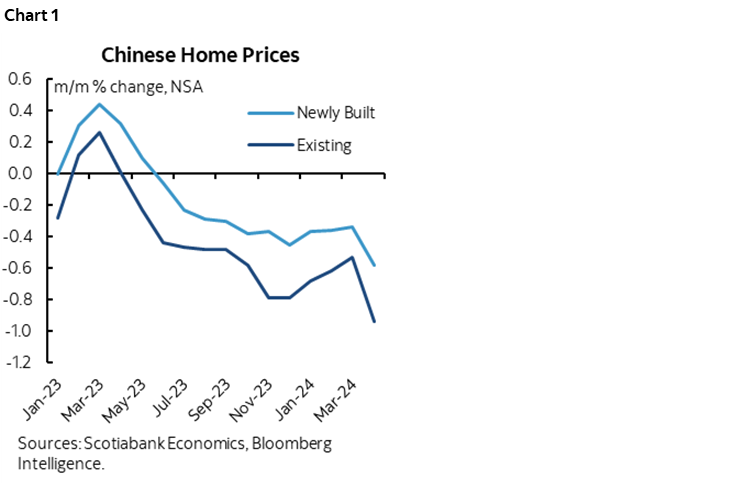

A second risk is whether potential buyers will take the bait which depends upon their outlook for Chinese property prices and their broader financial health. Chinese new home prices have fallen for 11 consecutive months in m/m terms and resale home prices have fallen for twelve straight months, presenting the catch-a-falling-knife dilemma for homebuyer sentiment (chart 1).

The impact on loan quality is another matter.

Further, if local governments do indeed start buying a material number of unsold homes, then it could further pressure their struggles with heavy debt loads with assets of uncertain value and spark more concern toward that space. That said, the size of the PBOC program to encourage state lenders to provide funding to local governments to buy homes is pretty modest in a bigger picture sense.

I’m also not sure that I understand what they are trying to do in engineering a paper swap to buy unsold new homes and convert them into, umm, other unsold ‘affordable’ homes?

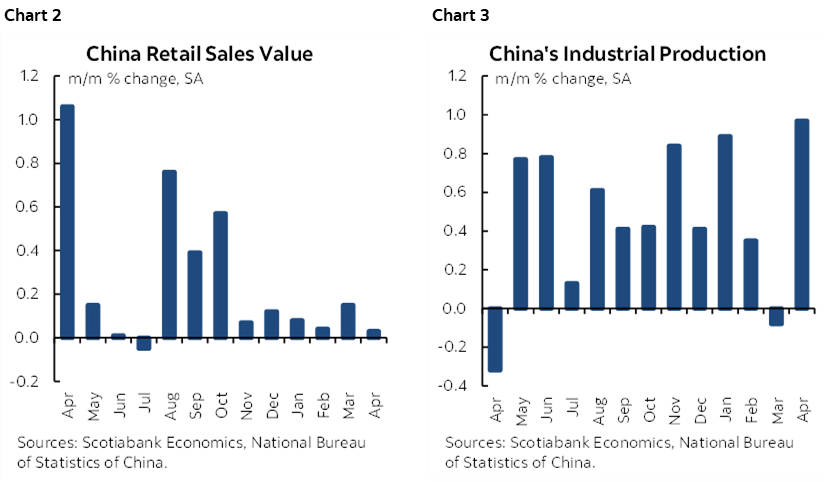

China also updated monthly macro readings that got lost behind the policy announcements. Retail sales were flat at 0% m/m SA and have not posted material growth in any month since last October (chart 2). Industrial output was up by 1% m/m SA for the strongest gain since September 2020 (chart 3). The jobless rate edged two-tenths lower to 5%.

We’ll hear from a few Fed speakers this morning but there are no planned releases. Governor Waller (10:15amET), Minneapolis Fed President Kashkari (10:15amET) and San Fran Fed President Daly (12:15pmET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.