| ON DECK FOR THURSDAY, MAY 16 |

KEY POINTS:

- Market reaction to US CPI stabilizes

- Was the bump in US jobless claims temporary?

- FOMC officials are unlikely to celebrate US CPI

- Australian job growth rebounds, markets not impressed

- The BoJ should tread carefully as Japan's economy contracts

- Minor US releases on tap

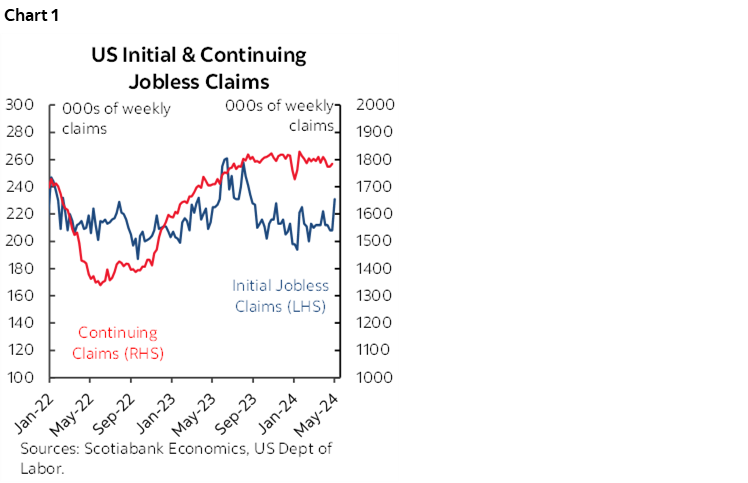

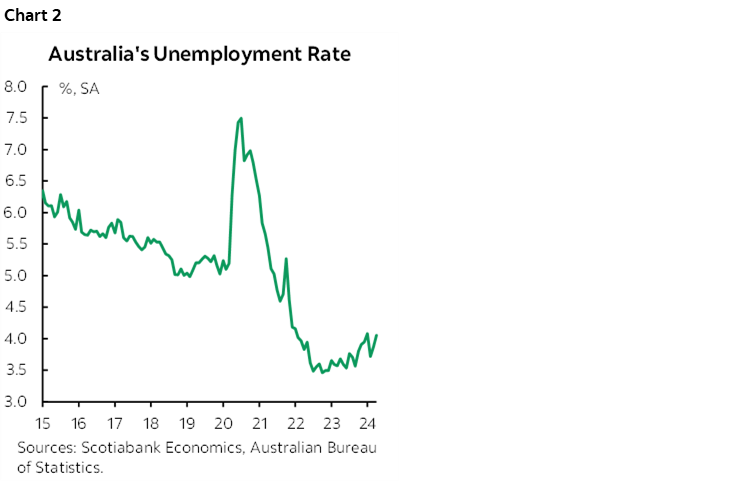

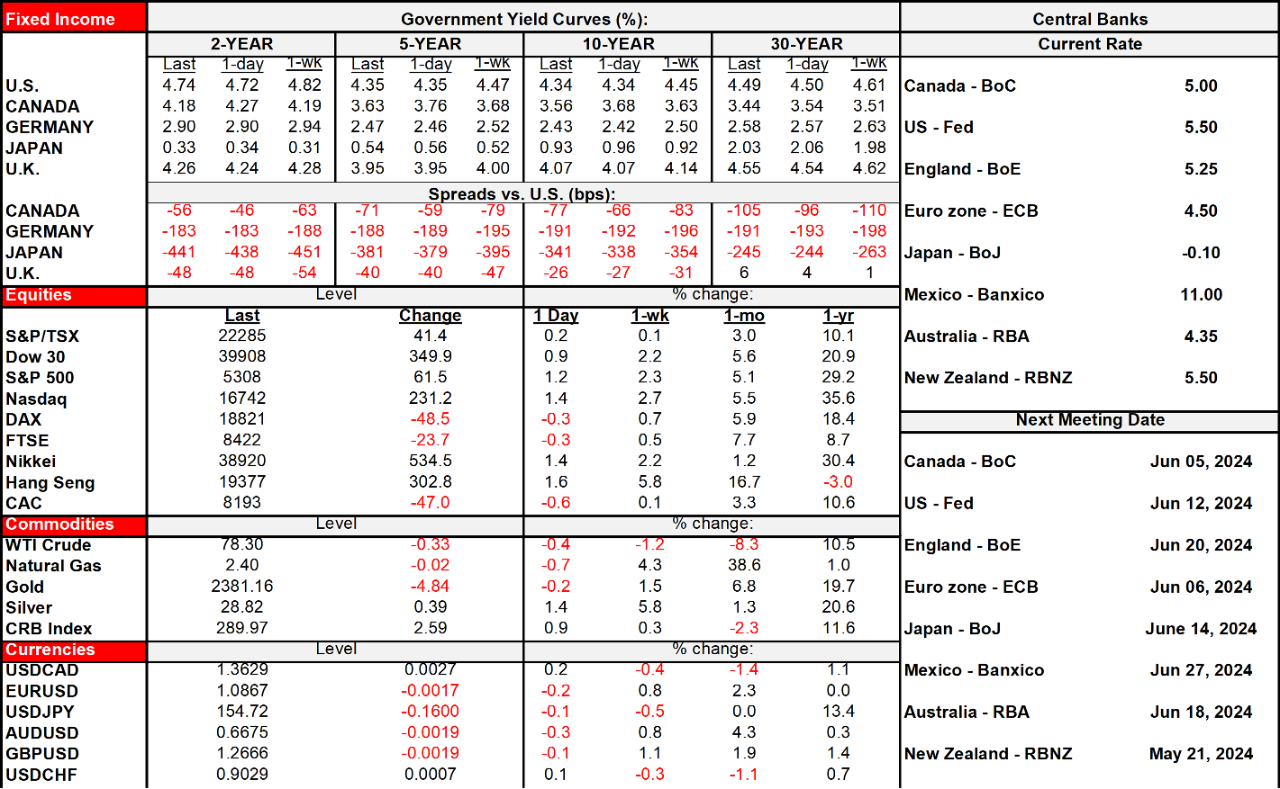

Reaction to yesterday's US CPI figures (recap here) has stabilized with US Treasuries holding firm with a slight cheapening bias. Asia-Pacific bonds rallied in lagging reaction. Australia's curve outperformed on US CPI spillover effects and a rise in the unemployment rate plus soft details behind a solid job gain. Japan's economy is very weak.

There will be two key issues to monitor into the North American market session.

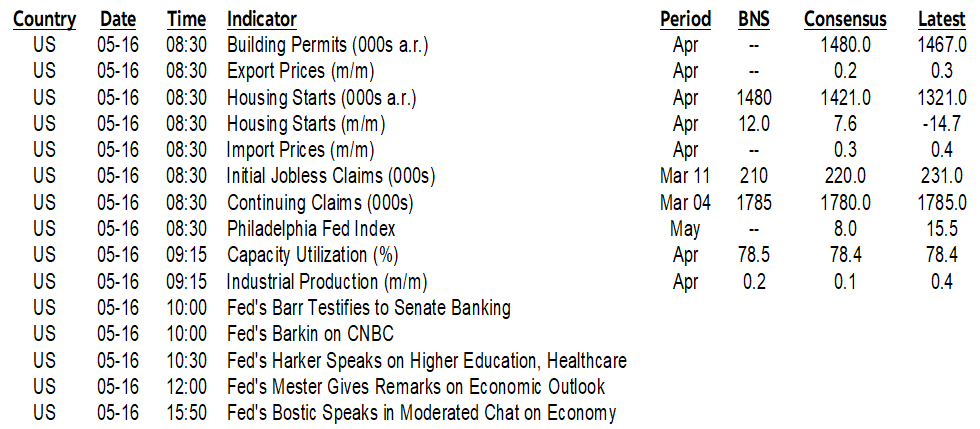

US Jobless Claims—A Temporary Bump?

Was the upward bump in US initial jobless claims (8:30amET) just distorted by spring break timing in parts of the country like New York where public school employees are allowed to file for benefits during the break? That's one theory. Or did the modest jump signal the beginning of a mildly deteriorating trend for the US labour market? We’re approaching the nonfarm reference period (pay period including the 12th day of each month) and the household survey’s reference week that includes the 12th, so the answer could matter to the next round of jobs figures for May.

FOMC Officials Probably Won't Celebrate CPI

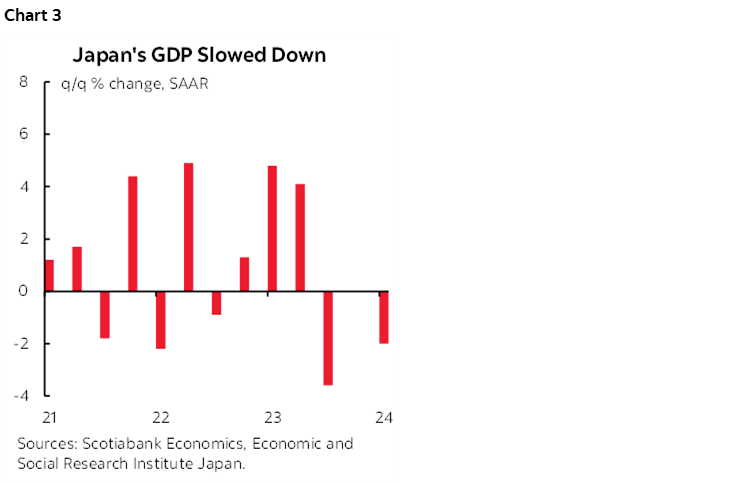

How will FOMC officials react to CPI? We’ll hear from several today including Vice Chair Barr (10amET), Richmond President Barkin (10amET), Philadelphia President Harker (10:30amET), Cleveland President Mester (12pmET) and Atlanta’s Bostic (3:50pmET).

The US also updates housing starts (8:30amET) and industrial production (9:15amET).

There were a couple of notable overnight releases.

Markets Not Impressed By Australia's Job Beat

Australia created 38,500 jobs last month which was stronger than consensus expectations for 24k. Details were soft with all of that gain in part-time jobs (+44.6k) as full-time jobs fell by about 6k. The trend has been very volatile so far this year with +11k more jobs in January, +118k in February, and -6k in March. The unemployment rate crossed 4% to 4.1% from an upwardly revised 3.9% the prior month. Chart 2.

The BoJ Should Tread Carefully

Japan’s economy is very weak. Q1 GDP contracted by more than expected (-2% q/q SAAR, -1.2% consensus) and the prior quarter was revised down to no growth from 0.4% following a contraction of -3.6% in Q3 that was revised down from -3.2% (chart3). The Q1 details were soft as consumption (-0.7% q/q SA non annualized, -0.2% consensus) and business spending (-0.8% q/q SA nonannualized, -0.5% consensus) were weaker than expected and both were revised a bit lower.

Further tightening of monetary policy may expose the BoJ to another episode of policy error imo. The economy is very soft. Core inflation continues to be on a declining trend. The effects of prior gains in oil prices and yen weakness on core inflation are waning. Furthermore, there is no evidence that last year’s Shunto wage gains for <20% of workers are driving broader wage gains while it’s too early to tell for this year’s Shunto gains.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.