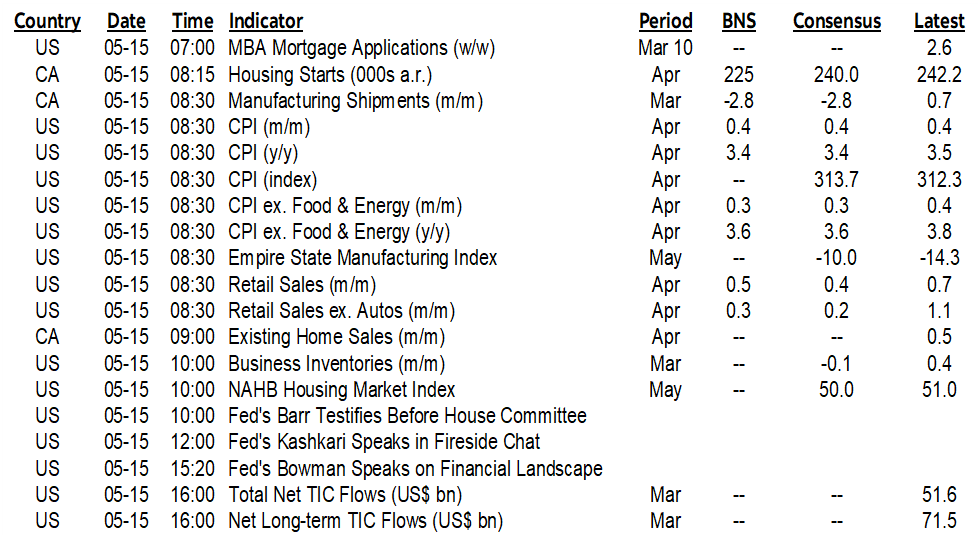

| ON DECK FOR WEDNESDAY, MAY 15 |

KEY POINTS:

- Improved market confidence in 2024 Fed cuts is sensitive to CPI update

- US core CPI is expected to be another warm one

- The simultaneous release of US retail sales could dirty the market reaction to CPI

- Australian wage growth remains strong

- The PBOC stayed on hold

- Swedish inflation had no effect on Riksbank pricing

- Colombia, Peru to update GDP

- Canada faces light releases

US CPI (8:30amET) will be the main focal point, but it’s not the only thing to consider today. Nor is it the last CPI report before the FOMC prints its next dot plot on June 12th as another one arrives that morning with the flexibility for Committee members to revise their forecasts that morning. June is ruled out for a move, but the dots could be impacted by the pair of releases.

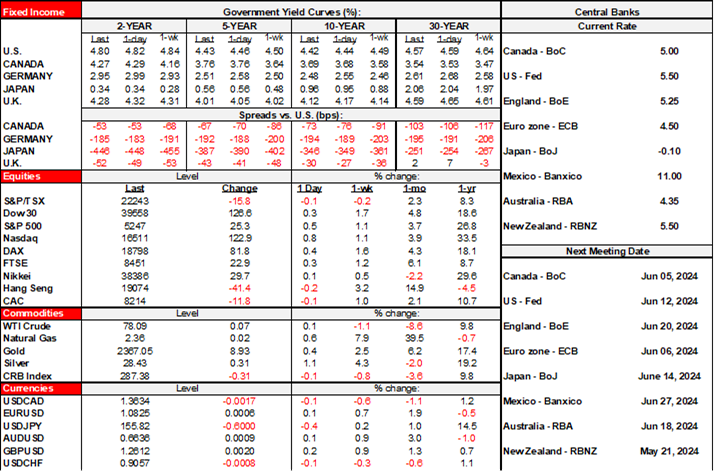

As for markets, they are less inclined to give up on cooler inflation and rate cuts now than they were when 2s breached 5% at the beginning of the month; 2s have since rallied by almost a quarter point. Cumulative pricing for Fed cuts this year has gone from about one 25bps cut at the start of May to about two now with cuts priced to start in September.

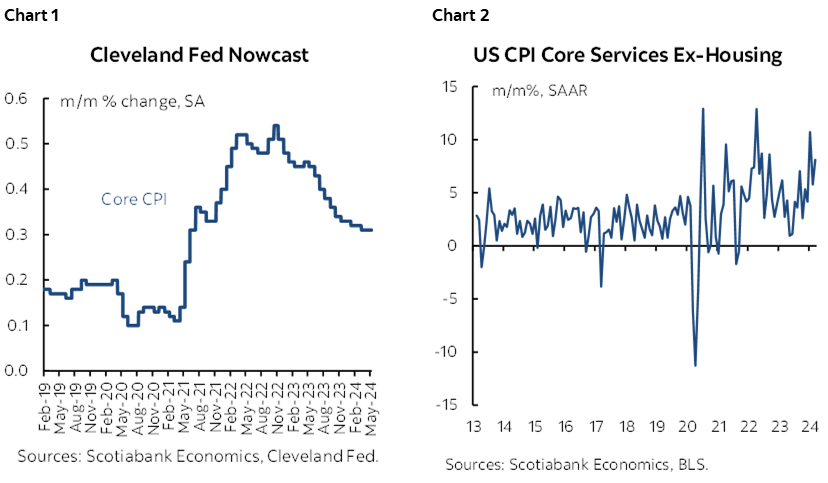

Is There too Much Agreement on US Core CPI?

This time around my estimates for US headline and core CPI are in line with consensus and nowcasts like the Cleveland Fed’s (chart 1). So, 0.4% m/m SA for headline and 0.3% for core. Drivers are offered in my week ahead article with the greatest uncertainty focused upon core services CPI (chart 2). Out of 66 forecasters (yes, that many…) only two went with a higher core number at 0.4% and three went with 0.2. Key will probably be core services inflation that has been on a tear this year and we have much lighter estimation capabilities for that component than on the goods side. The Committee has ruled out June imo, but there may be more risk to July pricing if the number lands weaker than stronger given how little is priced even for that meeting.

Simultaneous Release of US Retail Sales Could Dirty the Market Reaction

US nominal retail sales are poised for an update at the exact same time as CPI which could complicate the market reactions to both readings. Higher gasoline prices and vehicle sales should be enough to drive a top line gain. Another gain in core sales could be tough to deliver given a high jumping off point with a 1% m/m rise in March and proxies for underlying sales.

Light Overnight Developments

Here’s a short summary of other overnight developments:

- Australian wage growth cooled but continues to run at a rate that makes it difficult to achieve the RBA’s 2–3% inflation target range on a sustainable basis. Wages were up by 0.8% q/q SA nonannualized (3.3% q/q SAAR) in Q1 and the prior quarter was revised up to 1% q/q SA nonannualized (4.1% q/q SAAR). Chart 3.

- The PBOC left its 1-year Medium-Term Lending Facility Rate unchanged at 2.5% as expected.

- Swedish inflation had no effect on expectations for coming decisions by the Riksbank including on June 27th after they initiated cutting last week. Underlying inflation ex-energy was on the screws at 0.4% m/m.

- Eurozone employment was up by 0.3% q/q in Q1. Eurozone industrial output beat expectations at 0.6% m/m (0.4% consensus) and the prior month’s 0.8% rise was revised up to 1%.

Light Developments in Canada, LatAm

Other expected developments will include GDP figures out of Peru (11amET) and Colombia (12pmET) that might face a high bar to matter to local markets after US CPI.

Canada faces light data including housing starts for April (8:15amET) and manufacturing shipments during March that were previously guided to have dropped by –2.8% m/m (8:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.