| ON DECK FOR FRIDAY, MAY 10 |

KEY POINTS:

- Canadian jobs to start the data march to the June BoC

- Are US consumer expectations still holding at a high level?

- UK GDP beat, but looked less impressive under the hood…

- ...while the way Q1 ended sets up Q2 momentum

It’s jobs Friday in Canada and that’s the main focal point. US consumer sentiment and consumer inflation expectations often offers some degree of market risk. The gilts front-end is outperforming this morning partly on continued spillover effects from yesterday’s BoE decision and perhaps because a GDP beat was of low quality despite the celebratory tone in the press.

Canadian Jobs Start the Data March to the June BoC

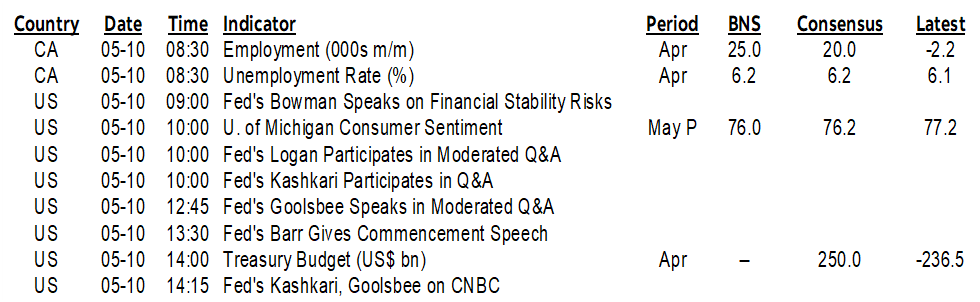

Canada could post a rebound in job growth during April (8:30amET) off the prior month's distorted flatness that was dragged down by youths due to March break timing in big parts of the country relative to the LFS reference week (chart 1). Breadth, wages, hours worked, the UR, labour force expansion and population growth are among the other readings that will matter. Please see the global week ahead for further views on the rebalancing of the Canadian labour market and wage pressures.

Is US Consumer Sentiment Still Strong?

US UofM sentiment for May (10amET) will further inform whether the rise in the expectations component to its highest level since 2021 is durable. Also watch the 1- and 5-10 year inflation expectations readings that have both been riding at or above 3%.

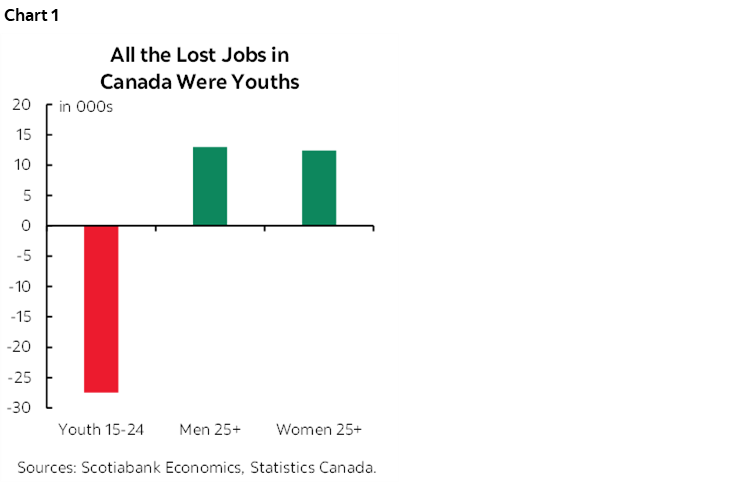

UK GDP Looks Less Impressive Under the Hood

The UK economy grew more than expected in Q1 on the surface, but the details were less impressive. GDP was up by 0.6% q/q SA nonannualized (0.4% consensus) which at least temporarily ends the technical recession that occurred with back-to-back declines in 23Q3 and Q4 while posting the strongest growth since 2021Q4 (chart 2). The rub lies in the facts that consumption added only 0.1% to growth in weighted terms, government spending added just under 0.1 ppts, business investment added 0.1 ppts, exports knocked 0.3 ppts off of GDP growth, and lower imports added a weighted ¾% to growth through less of a leakage effect. Inventories fell at a quicker pace which dragged an estimated -½% on growth which is likely the flip side of softer imports.

Q1 ended on a brighter note for the UK economy though and that could carry sounder momentum into Q2 but with an important caveat. GDP was up by 0.4% m/m in March (0.1% consensus) with industrial output up 0.2% m/m (-0.5% consensus), services up 0.5% (0% consensus), manufacturing up 0.3% (consensus -0.5%) and construction down -0.4% m/m (+0.5% consensus). The caveat behind the strong services reading reflects uncertainty toward the role of the earlier than usual Good Friday and Easter holiday effect that started on March 30th this year and its effects on related spending and travel may not have been fully offset by SA factors.

US macro risk will be quiet, other than UofM. Election year politics is behind headlines that Biden is planning tariffs on China perhaps to be announced next week and levied on electric vehicles, batteries, solar equipment etc. Biden isn’t as much of an anti-free trader as Trump’s moronic views, but the rich part of Biden’s action is the finger wagging at China’s subsidies. The US heavily subsidizes EV buyers and producers itself. So does Canada.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.