| ON DECK FOR THURSDAY, MARCH 7 |

KEY POINTS:

- Yen surge dominates overnight markets

- Wages, Board member comments add to the BoJ’s imperfect case for hiking

- The ECB should be in no rush to ease given core inflation persistence…

- ...and pending key Q1 wage figures

- US job cuts remain compatible with net job growth, may be more seasonal than usual

- Is Canadian trade momentum carrying into Q1?

- Mexican CPI lands on the screws thanks to a running head start

- German factory orders tanked

- Bank Negara held

- Saint Powell winds up again

Markets await the ECB’s messaging after further developments in Japan added to speculation that the BoJ may hike this month. Any reactions will no doubt quickly give way to focusing upon tomorrow’s US and Canadian jobs and wages. There is little spillover from the BoC’s communications but it’s continuing yesterday’s reaction by putting a small bid to CAD that is nevertheless underperforming after yesterday’s rally and given broad USD softness this morning. Canada’s rates curve is basically unchanged after yesterday’s cheapening in 2s but that’s being retained.

BoJ Fever

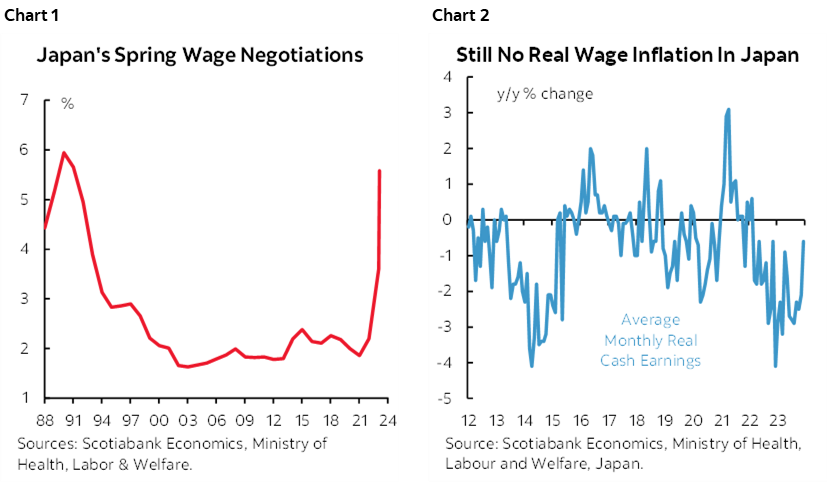

BoJ fever got a little hotter overnight. Wages were the reason. Rengo said that the average wage gain being sought by its member unions this year is 5.85%. That’s much higher than last year and higher than initially sought. It’s the strongest back-to-back gains being sought since the early 1990s (chart 1). Some member unions are seeking about a percentage point more than that figure. We’ll get tentative results next week. There is also more evidence of broadening wage gains beyond just the biggest companies subject to the Spring Shunto negotiations. Nominal labour earnings were up 2% y/y in January (consensus 1.2%). In real terms that works out to -0.6% (-1.5% consensus). At least that’s progress, but let’s not get carried away here (chart 2).

The data prompted more sentiment that the BoJ could hike and end negative rates this month. A BoJ Board member fanned this perspective with his remarks.

When I was in Japan last week there was dominant sentiment that now is the best opportunity that the BoJ will get to end the pernicious effects of negative rates and seize upon confidence building arguments that deflation is gone. I hope they’re right because the consequences to being yet another false start by the BoJ could be devastating. The fear was this opportunity would slip away if and when the Fed begins to ease. Clearly that fear is being tamped down each time a Fed official speaks and favours later and less cutting.

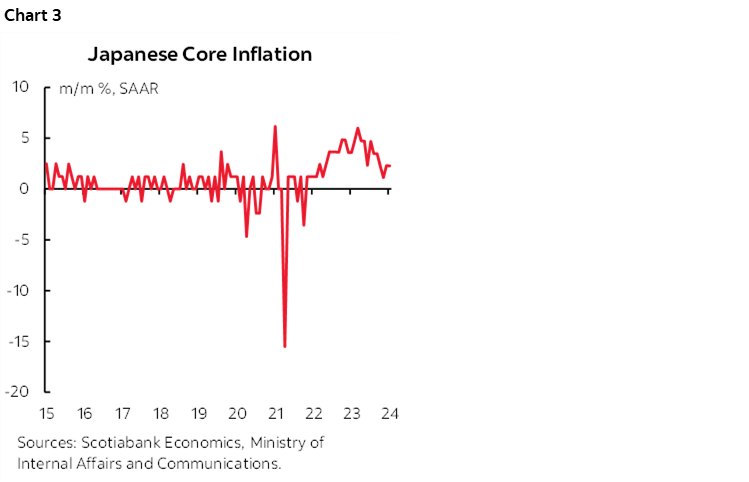

Still, there are doubts about whether the BoJ should be hiking. What if wage growth is only temporary? There has to be more trickle through to smaller businesses. There has to be greater evidence that would pass through to core inflation when core inflation m/m has been decelerating from the peak (chart 3). Then there is weak productivity since at some point one would think shareholders may ask c-suites to give their heads a shake if large wage gains are granted absent any productivity rationale for doing so. And of course there is the yen-Fed connection as well.

ECB Waiting Until at Least June

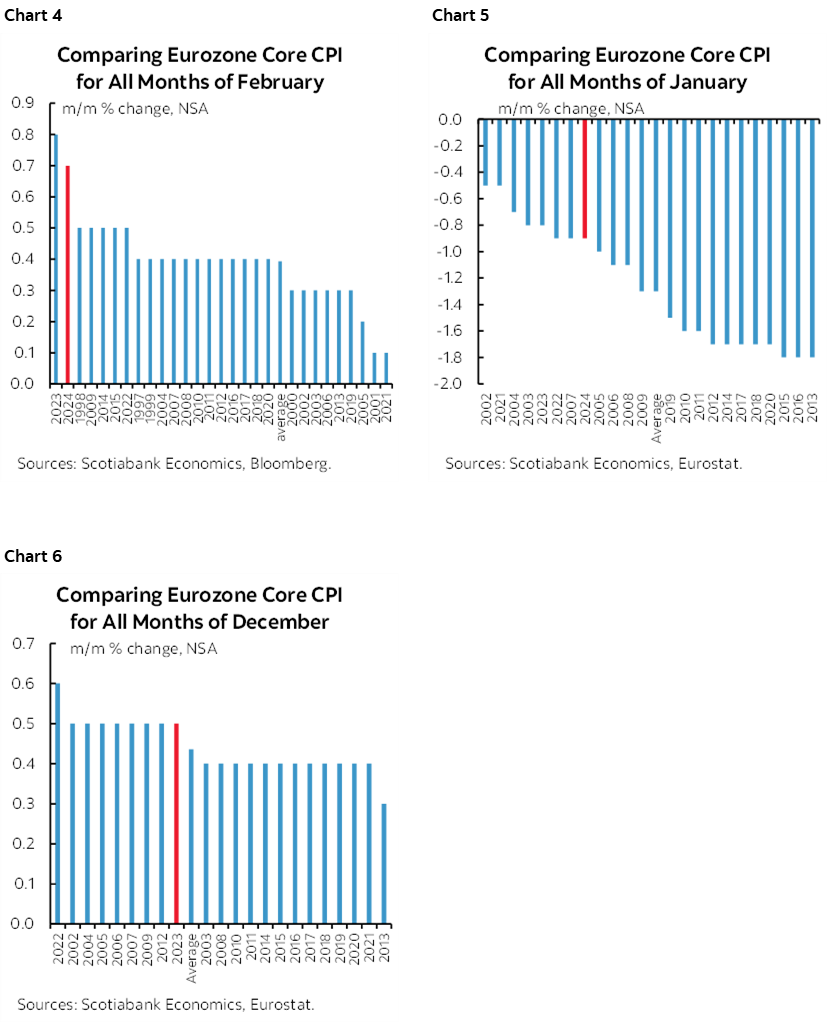

For the third time this week, we’ll hear from another central bank that says it is in no rush to do much of anything. The ECB will stand pat and likely continue to guide that they will prefer waiting for Q1 wage figures that arrive around the June meeting. The statement lands at 8:15amET and President Lagarde hosts her press conference at 8:45amET. The staff forecasts get releases at 9:45amET. The Q1 figures are particularly important to the ECB given the seasonality of collective bargaining exercises. On top of that is the fact that m/m core inflation is sending warning signs that it’s premature to ease up as each of the past three months of m/m core CPI figures indicate that inflationary pressures remain very much alive in the Eurozone (charts 4–6). The ECB’s updated forecasts may inform current policy attitudes and rate cut timing, but they could change by June when we get more evidence on these factors. And in any event, always, always take what central banks forecast for inflation with a mountain of salt.

German factory orders reversed the prior month’s optimism amid an extremely volatile data. Orders fell by -11.3% m/m in January, nearly doubling the consensus estimate for the drop. Part of the reason was that the prior month was revised up to a gain of 12% from 8.9%.

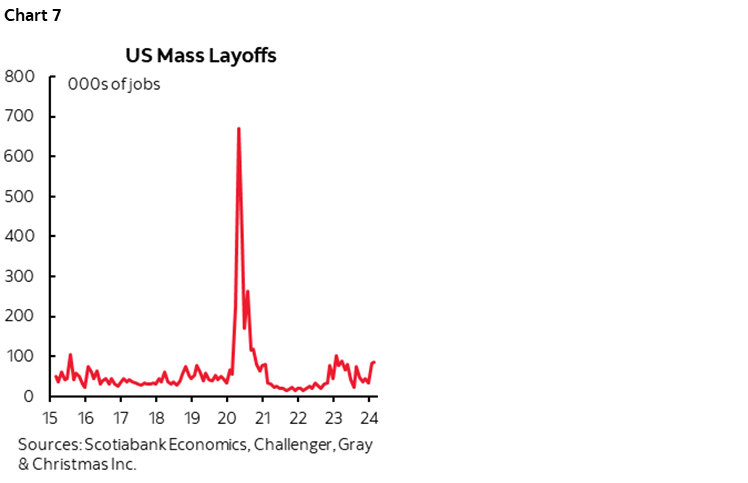

US Challenger job cut announcements landed at 84.6k last month. That's very close to the 82.3k the prior month and signals a pick up in the pace (chart 7). Still, the numbers remain compatible with net job growth. Cuts are higher than prior months but around where they were at this time last year. I still think some of that is not fully controlled by SA factors as new fiscal years kick off with trimming announcements following the prior massive wave of hiring announcements.

Bank Negara Malaysia held at 3% on currency concerns as expected.

Mexican inflation landed on the screws in February with headline at 4.4% y/y and core at 4.6%. It usually does, given that bi-weekly inflation gives a running head start for forecasters.

Modest data risk also lies in store. Watch Canadian trade figures to see if Q4 net trade momentum as a GDP driver is carrying into Q1 (8:30amET). The US trade deficit is unlikely to offer a material surprise to expectations for about a –US$63.4B tally given that we already know the merchandise component onto which a usually stable services balance will be tacked. The US also updates weekly claims (8:30amET).

And of course, Chair Powell must have a Saint’s patience as he winds up for another run at Congressional testimony today, this time before the Senate Banking Committee (10amET). It can sometimes add fresh surprises but is usually a replay with different actors.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.