| ON DECK FOR WEDNESDAY, MARCH 6 |

KEY POINTS:

- Markets await Powell, the BoC, data

- BoC: Hold, patient, and no QT guidance yet

- Powell’s testimony has every reason to preach patience...

- ....and will defer QT discussion to the March FOMC meeting

- US ADP, JOLTS and Beige Book on tap

- Canada might get a transitory lift to productivity

- Canadian consumer credit quality remains strong

Well it’s official now. Nikki Haley dropped out and now Americans will have to choose between two old polarizing white guys who can’t remember each other’s names. It’s a fine state of affairs. Fortunately markets will spend today more focused upon some adults in the room as we start to liven up market developments over the back half of this week and starting with communications from the Federal Reserve and the Bank of Canada.

POWELL’S TESTIMONY—WHAT, ME RUSH??

Federal Reserve Chair Powell will deliver his semi-annual monetary policy testimony before the House Financial Services Committee today (10amET). He will deliver opening remarks that will be available at the start and then go into back-and-forth banter with members of the Committee. It could well be impactful to markets and often has been in the past.

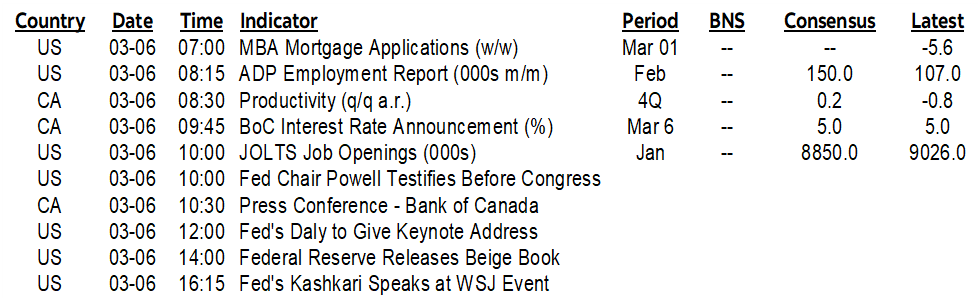

In fact, Fed Chair Powell’s testimony is likely to carry the heaviest potential influence to global markets today and lands smack in the middle of the BoC’s communications. Patience is expected to be the word of the day. Core PCE just lit up. Payrolls entered the year on strong footings with upward revisions. Average hourly earnings posted the strongest monthly rise since March 2022. GDP is tracking another decent gain in Q1 that continues to advance the resilience theme. The consumer is in fine shape; extraordinarily strong shape I’d say and even on credit quality as we’re only coming gently off of basically next to no defaults when money was being given away especially on the mortgage book (chart 1).

Nothing screams out any urgency for the Fed to cut rates. Scotiabank Economics continues to lead consensus on the Fed as others push out; I never believed in March or May as a cut call. That said, I’m more worried about fewer rather than more cuts than our 100bps of cuts starting in Q3 and that needs an awful lot to go right and starting soon.

Overall, expect Powell to refer to the dots in December that showed 75bps of easing this year and it wouldn’t be surprising if he guided that there was a higher bar set against doing more than in favour of doing less.

I would also expect Powell to indicate that QT and overall balance sheet management is going a.o.k. thus far. I think he’ll continue to defer to the FOMC dialogue on March 19th–20th in terms of what to do, but the tone of their communications seems to lean toward further discussion thereafter, versus an imminent policy decision.

BANK OF CANADA—TWEAKING INTO SPRING

The Bank of Canada will only deliver a statement (that should be here), sans any forecasts or MPR (9:45amET). Macklem and Rogers will deliver the now customary press conference even after non-MPR meetings like this one instead of the previous approach that rotated a speech and presser the day after across Governing Council members following non-MPR meetings (10:30amET). I expect statement tweaks and the overall message to be that relatively little has changed in their minds compared to the late January MPR.

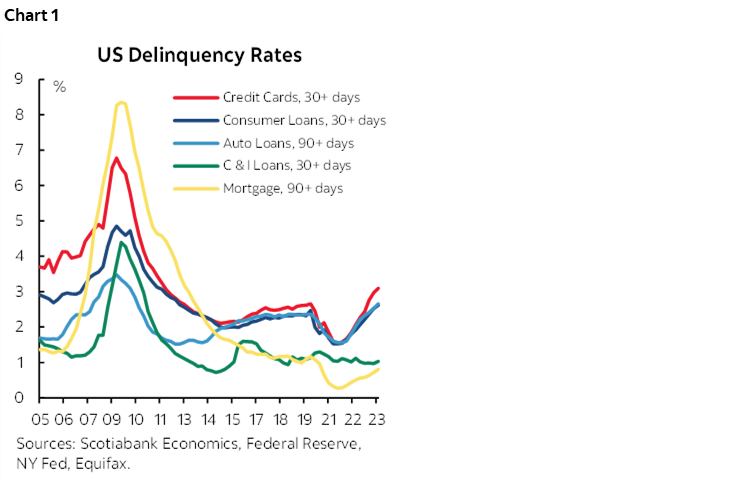

Key will be the final paragraph that will likely repeat guidance that they are “still concerned about risks to the outlook for inflation” and wish to see further and sustained easing in core inflation and to repeat emphasis upon what they are focused upon in that regard. After all, trimmed mean and weighted median m/m SAAR have only had one soft month thus far after a long string of hot increases (chart 2). The assault on these measures by some shops is futile imo as these measures have their attractive features and in any event they are the BoC’s preferred gauges as stated right up front in each MPR and in every speech and press conference. Plus, Macklem always says they are monitoring a whole range of evidence as it feeds into their views on inflation and inflation risk.

To change that final paragraph could risk being seen as a signal to set up an April cut. That’s highly unlikely to occur. It would go against everything they’ve said about needing a three-step process: more soft data on core inflation; then they’ll evaluate if they think it will stick; then they’ll court a dialogue on when to ease. That’s been a feature of their communications since late last year.

Further, cut into the Spring housing market when shelter’s one-quarter weight in the basket is already hot and may face further upside with spillover effects on related types of consumption?? Macklem said he can’t fix affordability with the tools he has, but he also said he can’t ignore shelter. His mandate is 2% over the medium-term, not 2% ex-shelter which is a quarter of the CPI basket after removing mortgage interest. Plus, cut into the middle of the Budget season as governments ramp up spending? Oh that would be precious; out of control fiscal largesse reinforced by monetary easing and here we go again in terms of adding to inflation risk. Cut given tracking of a Q1 rebound in GDP? Cut given good reason to think that January’s m/m core readings were temporarily weighed down?

In my view the BoC could easily and materially lag the Fed and the Fed’s not even ready to go and won’t be for a while yet. Inflation risk is higher in Canada than the US given much stronger immigration and overall G10-leading population growth in Canada, severe housing shortages, soaring wages and tumbling productivity, and relative fiscal policy. US fiscal policy is set until sometime after a new Congress is established, but Canada’s remains expansionary with Canada’s election not until next year and the government’s polling best characterized as a dumpster fire. Plus, the BoC is already 50bps behind the Fed with a similar neutral rate range and a weaker currency; cutting before the Fed and more quickly would make C$20 notes nice bathroom wallpaper. As for GDP, the US has the upper hand, but Canada’s economy is stronger than GDP indicates and, in any event, Canada has not opened up anywhere nearly enough slack in order to offset the other more dominant drivers of inflation risk.

I don’t expect anything material on the BoC’s QT plans today. DepGov Gravelle—the BoC’s markets guy—delivers a speech on normalization of the balance sheet on March 21st. It’s not the Governor’s strong suit. It’s also not his style to scoop his Deputy, to manage down instead of to his level and up, to compete against his subordinate, or to conflict. One thing you can say about Macklem is that he’s a secure, classy guy and strikes me as a good manager rather than a total bureaucrat.

DATA DISTRACTIONS

Beyond Powell and the BoC, there is also a significant line-up of data that could be impactful to markets. Some of that data could well mess up market reactions to the day’s two main events before we forget they ever happened and move onto nonfarm payrolls and Canadian jobs.

- US ADP private payrolls (8:15amET): The consensus guesstimate sits at +150k and I’m similar at +160k. This measure of job growth has definitely been slowing toward about the 100–150k range of monthly changes. ADP is nevertheless a notoriously poor indicator of what to expect for private nonfarm payrolls that are due out on Friday. ADP can spark a market reaction, until the real McCoy lands.

- US JOLTS (10amET): Job vacancies unexpectedly increased over the past couple of months and that rattled a few cages by challenging the narrative that cooling job openings indicated that the labour market was coming back into balance and away from excess demand. January’s reading will help to further inform this trend.

- Canadian labour productivity (8:30amET): I went with +0.6% q/q SA nonannualized. If that happens, then it would be the first quarterly gain since 2022Q1 and that one was the only quarterly gain in the past thirteen quarters. Pathetic? You bet. The reason for a possible Q4 increase is that hours worked fell due to strikes and there was a modest gain in the business sector’s component of the 1% q/q gain in GDP.

- Fed’s Beige Book (2pmET): This used to matter a lot more back when FOMC officials spoke a lot less. It can still be a somewhat useful source of regional anecdotes on the performance of the US economy but it will probably get buried behind the day’s other more important developments.

CANADIAN HOUSEHOLD CREDIT QUALITY IS HOLDING STRONG

On a separate note that is indirectly related to the BoC, what’s going on with Canadian credit quality? This report from Equifax Canada drove media coverage that made it sound like we’re in deep trouble. Nonsense. The report is quoting massive percentage changes in still very low percentage delinquency rates and making it sound like it’s really truly awful out there.

For example, they say the Canadian mortgage delinquency rate has risen by a whopping 52%. Wow, sounds like we have a crisis, right? That’s a really big number.

Until you read that it went from 0.09% a year ago to 0.14% now. Going from nothing to, well, still nothing is hardly a crisis. That's right. 0.14%. Remember what it hit in the US during the GFC? Yeah that would be 8.35%. 835bps versus 14bps. Crisis, you say. Hmph.

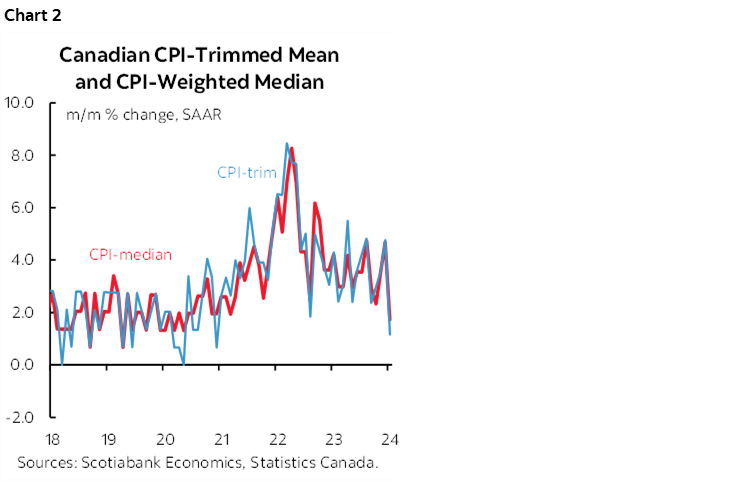

CBA data shows the share of mortgages in arrears by 90+ days has gone from a record low of 14bps in September 2022 to 18bps now (chart 3). Gosh, is it still safe to go outside?

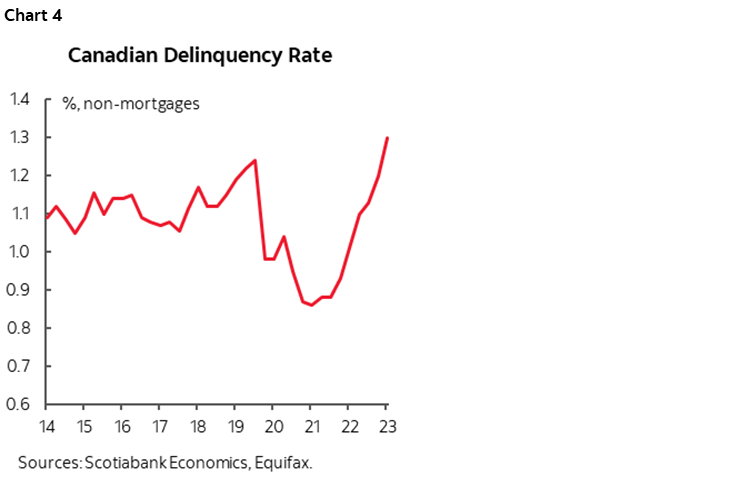

As for non-mortgage loans the 90+ arrears ratio has gone from 1% to 1.3% over the past year. Equifax quotes that as a massive 28.9% rise. That’s still a fraction of the rate in the US now, let alone during the GFC. Chart 4 shows that the delinquency rate has gone from a low of about 0.9% to 1.3%. It’s basically just over 1% and toward pre-pandemic levels but off the bottom during the pandemic when heavy fiscal supports and very low rates drove even lower defaults.

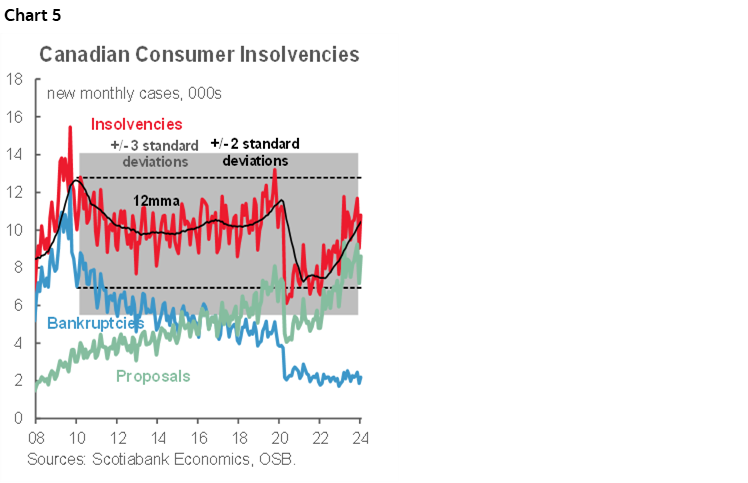

Chart 5 shows the pattern in terms of consumer insolvencies, proposals and bankruptcies. Bankruptcies remain at record lows. Yes, record lows. Proposals to work with lenders have risen and that’s driven a surge in total insolvencies that combine the two. This is how the Canadian banking system works by way of lenders and borrowers arriving at solutions to manage payments stress. Extending amortization, backing into gains in home equity, consolidating debts, trimming discretionary spending etc are among the options in a system that is largely devoid of the unwise strategic default option that makes the US banking system an oddity. Canada’s banking system is based upon a much more collaborative and stable approach.

And in any event, the narrative that deteriorating credit quality should drive immediate rate cuts misses the plot. The entire point to tightening monetary policy is to inflict pain upon the economy in an effort to cool things down and reduce inflationary pressures. In my opinion, we are not yet anywhere closer to being in the clear in terms of declaring victory against inflation risk.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.