| ON DECK FOR MONDAY, MARCH 4 |

KEY POINTS:

- A quiet start to a lively week ahead following marketing in Asia

- Observations on this past week’s key global macro developments…

- …including CDN GDP, US core PCE, EZ core CPI, Japanese core CPI

- Canada’s Week Ahead: BoC, Jobs, productivity

- US Week Ahead: Powell, Supreme Court, Super Tuesday, SOTU, nonfarm

- Asia Week Ahead: Ueda, China’s Congress, Chinese CPI, AU GDP, Negara

- Europe Week Ahead: ECB, Q4 wages, UK Budget

- LatAm Week Ahead: BCRP, Mexican & Colombian CPI

Regular publishing resumes this week after a week of marketing in Asia including Taipei, Bangkok, Singapore and Tokyo. Four countries in five days with two red eyes straight into meetings and about two dozen meetings with fixed income, FX and corporate clients arranged by my fantastic Scotia colleagues in the region. The pace was hectic but rewarding.

The overall region’s potential is enormous both in terms of their own markets and appetite for foreign markets. There were rich discussions on the global economy, global central banks and market opportunities with a particular focus upon the US and Canada. In fact, the level of interaction was the highest I’ve seen to date with a long list of key points of discussion and advice. Plus, frankly, you can’t cover countries and regions that are significantly driven by commodities—like Canada and LatAm—without a view on Asia.

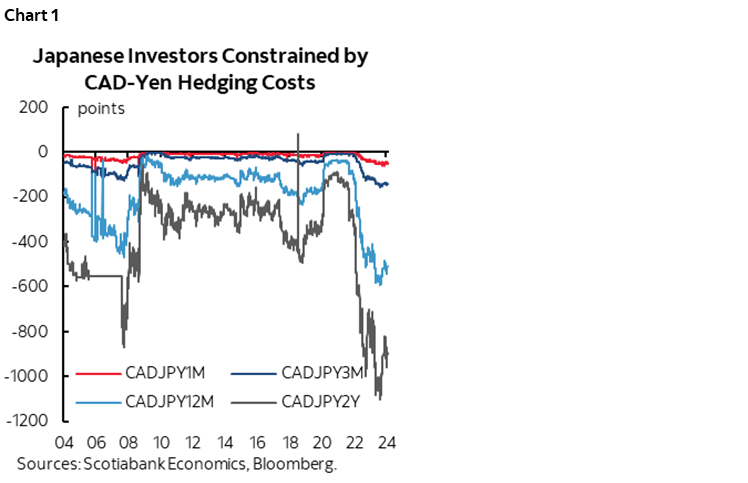

The opportunities to investors in both directions are impressive. Japanese investors are constrained by high hedging costs out of the yen (chart 1) as the opposite—negative hedging costs—attracts foreign inflows. That won’t last indefinitely and hinges upon some combination of if and when the BoJ hikes and how many times, plus when the Fed, BoC and others might start to ease. Foreign central banks need to be careful toward this future wall of money that could begin coming out of Japan when such a moment may arrive.

There is nothing to note by way of developments in markets to start the week. Instead, I’ll highlight observations on last week’s macro developments and provide a brief outline of key developments that are expected this week.

OBSERVATIONS ON THIS PAST WEEK’S DEVELOPMENTS

Below are some of my opinions on this past week’s developments.

Canadian GDP and the BoC’s Path to Spring

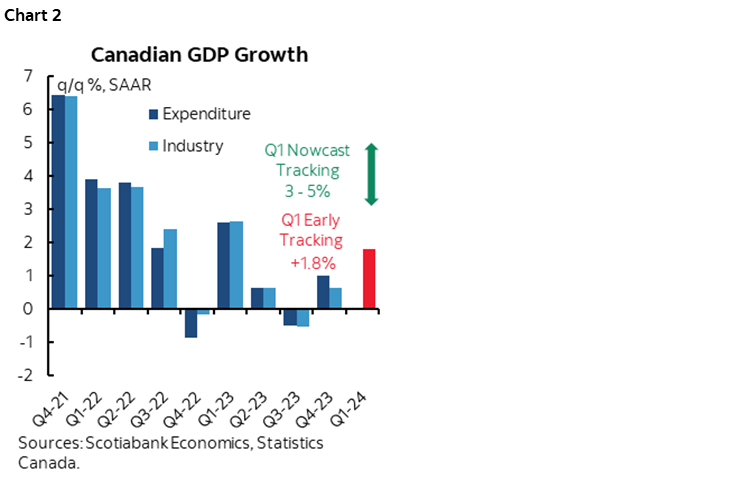

Canada is putting in place the ingredients for a significant rebound in the economy into Q1. This is highly preliminary, given that it’s early in terms of data, but q1 GDP is tracking growth of 3–5% q/q SAAR using our nowcast depending upon a range of assumptions. It’s tracking about 1.8% q/q SAAR if we only use the monthly gdp figures from Q4 and January and assume that February and March are flat just to focus the effects upon what we know. See chart 2. A lot of data still lies ahead and so this tracking is at a highly preliminary stage.

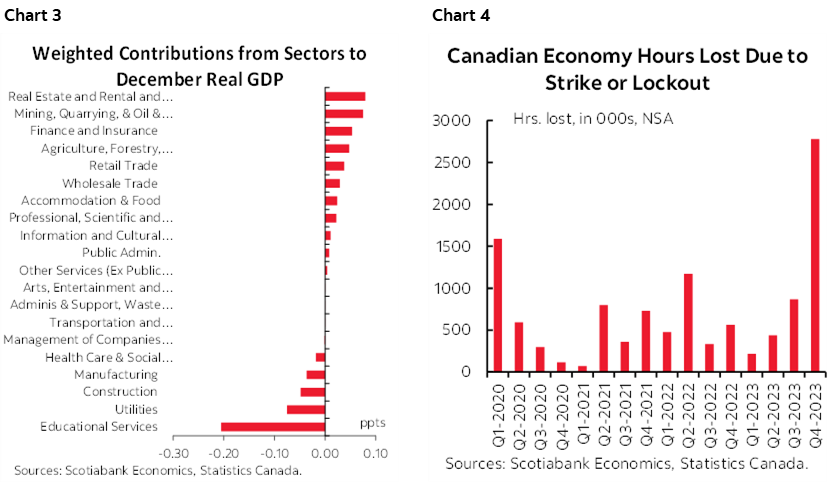

I felt that a lot of the commentary on newswires couldn’t see the forest for the data. December GDP was flat for transitory reasons like strikes and abnormally mild weather probably due to El Nino and we can see the effects in terms of how education and utilities were the biggest drags on December GDP resulting in a weighted drag effect of 0.3 ppts for the month (chart 3). All of Q4 was soft because of strikes that hit hours worked and hence GDP plus there was another inventory drag. Contributions to soft December GDP included weak output at utilities that were due to weather and strikes that walloped the public sector in Quebec. They hit hours worked along with all the other q4 strikes (chart 4). That also disrupted final domestic demand. Nevertheless, hours worked are tracking a surge of 2.6% q/q SAAR into Q1 and that’s a plus for Q1 GDP. This will be updated again when we get February hours worked on Friday.

With the caveat that we need more data, the implication is that the BoC may be facing an awkward Spring at least for the cut fanatics. Q1 GDP may be strong when it lands toward the end of May. The housing market is probably going to be strong into Spring. Major Canadian governments will probably be adding more fiscal stimulus this budget season. January core inflation m/m SAAR was probably soft for temporary reasons and could well rebound. If all that plays out, then forget cuts. Pay and push out. Keep a piece of your minds open to the opposite. This week’s BoC statement will be a snoozer, a cut in April would be about the dumbest thing the central bank could do, and let’s just see how the 22bps of a cut by June evolves from here but count me highly skeptical.

US core PCE and the Fed

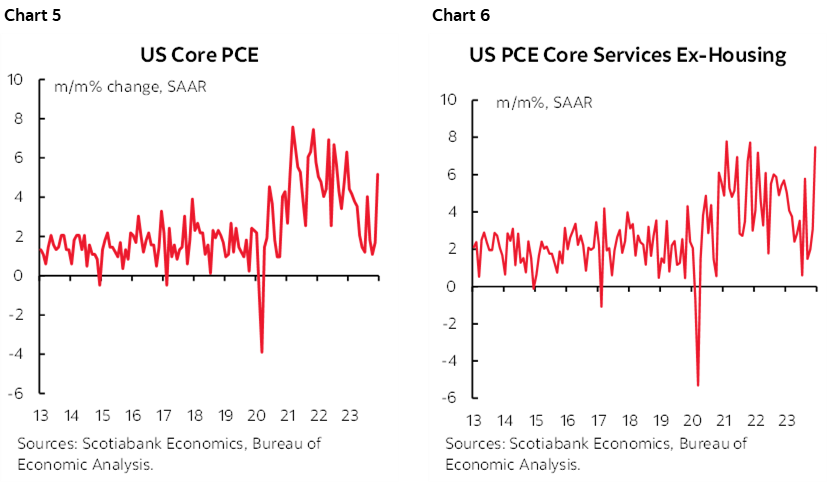

The Fed’s preferred inflation gauge accelerated to 0.4% m/m SA in January, matching consensus and my estimate for the hottest reading in about a year since last January’s 0.5% print (chart 5). Key was the heat in core services ex-housing (chart 6). That had a fleeting effect upon pricing for the June meeting that was scaled back to 17bps before Friday’s soft data on ISM-manufacturing and a downward revision to UMich sentiment popped pricing back up to about 23bps. ISM-mfrg and UMich??? Gimme a break, talk about second or third tier data. The May meeting only has 6bps priced and it’s unlikely they will have the comfort to ease at that meeting given renewed warnings on core PCE, wages, nonfarm and solid tracking for Q1 GDP growth that lands just days before. A lot of data precedes the June meeting including four core PCE prints and four readings on nonfarm payrolls and wages. Still, watch Powell’s testimony this week that may well lay the groundwork for being in no rush to do much of anything in the nearer term.

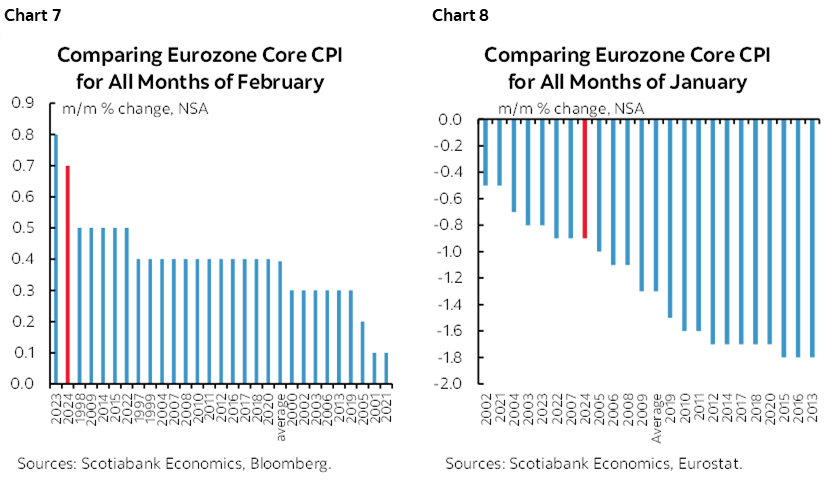

Eurozone core CPI and the ECB

Once again, February’s core CPI reading was among the hottest on record in seasonally unadjusted terms as published. Chart 7 shows that the 0.7% m/m NSA increase was the second hottest on record when comparing like months of February over time. This follows the similar observation in January (chart 8). The outcome reduced pricing for a cut by the April meeting toward a very low probability and knocked a few basis points off of pricing for a cut by the June meeting. June remains contingent upon Q1 wage settlements as the data won’t arrive until then.

Japanese core inflation and the BoJ

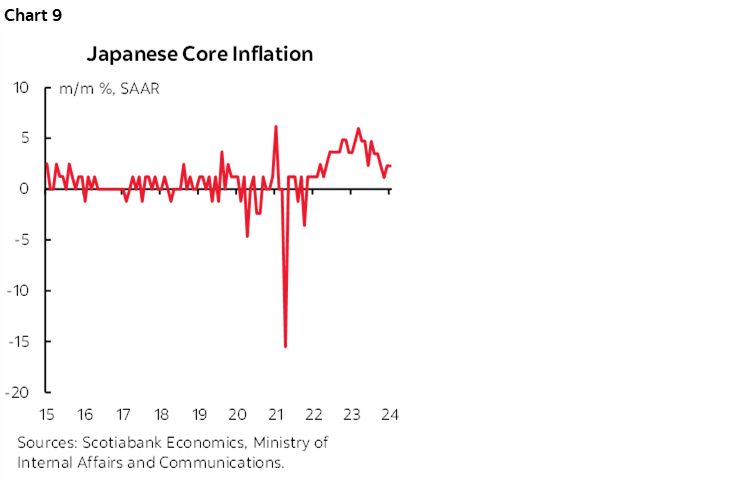

Core CPI inflation landed at 2.3% m/m SAAR again in January, matching December’s reading (chart 9). The marked deceleration from the peak last year may have stabilized over the past three months at a moving average of 1.9% m/m SAAR.

Japanese core inflation and the BoJ

Core CPI inflation landed at 2.3% m/m SAAR again in January, matching December’s reading (chart 9). The marked deceleration from the peak last year may have stabilized over the past three months at a moving average of 1.9% m/m SAAR.

Markets are significantly priced for a 10bps hike by the April 26th meeting and fully priced for June. Governor Ueda’s remark last week was somewhat ambiguous when he said “We are not yet in a position to foresee the achievement of a sustainable and stable inflation target. We will continue to seek confirmation whether the virtuous cycle between wages and price began to turn.” That may suggest that the decision continues to rest upon the outcome of the annual Shunto round of wage negotiations, or it could indicate a preference for further evidence that this will translate into durable underlying pressure on core inflation that could take longer to assess.

The widespread opinion during meetings with Japanese clients last week was that negative rates will end soon as the BoJ seizes a limited window of opportunity to hike before the Fed has greater conviction to begin easing perhaps by later this year. Arguments against hiking include whether the lagging pass through effects of prior yen weakness and higher oil prices on core inflation are fading, that Japan’s economy is now in technical recession, whether wage growth is merely going through a transitory acceleration and one that isn’t passing through to small businesses and average inflation-adjusted earnings, and a history of mistimed moves relative to the Fed. I suppose there may be an animal spirits argument for declaring deflation to be over and the era of negative rates with it if it drives confidence, but only if the claims turn to reality versus the damage that could be caused if that doesn’t happen.

THIS WEEK AHEAD’S MAIN DEVELOPMENTS

I will briefly summarize key expected developments in lieu of a Global Week Ahead this week.

Canada—BoC, Jobs in Focus

- The Bank of Canada issues a statement on Wednesday (9:45amET) followed by a full press conference held by Governor Macklem and SDG Rogers at 10:30amET. They shouldn’t even bother to issue a statement this time, but they must. It should be three words: ‘See ya later.’ No tee up is expected because, well, one of the dumbest things they could do would be to cut in April in the heat of the Spring housing market and government budget season when they’ve clearly signalled a need for much more evidence of softening core inflation than just one month and given robust Q1 GDP tracking as noted above.

- Friday brings out the updated February tallies for jobs, wages and other key labour market data. I’ve estimated a jump in jobs of +25k, a dip in the UR to 5.6%, and a rebound in m/m SA wage growth.

- Q1 productivity (Wednesday) may stabilize after prior large declines as the drop in hours worked and modest gain in business sector GDP reinforce one another.

US—Politics, the Fed and Key Data

Key events this week will include the following in chronological order:

- The US Supreme Court is expected to deliver a decision on something major today. Articles I’ve read indicate several signs that it could be regarding Trump’s eligibility for the ballot in Colorado ahead of their primary tomorrow. I’d be thoroughly surprised if the robes declare him to be ineligible.

- Super Tuesday is tomorrow. Who cares. A replay of Trump versus Biden seems to be in the bag.

- ISM-services for February arrives tomorrow. Most expect a softer reading, but most expected that when it surprised higher the prior month as well.

- Fed Chair Powell delivers his semi-annual testimony on monetary policy before both chambers of Congress at 10amET on Wednesday and Thursday. The general tone is likely to counsel patience and no rush to cut.

- President Biden delivers his State of the Union speech on Thursday. Expect strident fist-pumping ahead of November’s election but it’s a speech that is longer on hyperbole and hypothetical targets and short on concrete plans.

- Friday’s nonfarm payrolls are forecast to rise by 210k with a slight dip in the UR to 3.6% and solid wage growth of 0.3% m/m SA after the prior month’s 0.6% surge.

Asia-Pacific—Real Versus Fake Deflation

Several key developments are ahead this week:

- BoJ Governor Ueda will briefly appear tonight at a Fintech Summit (11pmET) to deliver what is billed as a ‘special message’ with numerous key officials present. It could be nothing, or it could be a lot. The appearance comes along with a report from Kyodo that the government—including PM Kishida—is considering officially stating that deflation is over but it may or may not be stated now or in subsequent communications. The symbolism of declaring deflation to be over could be informative to BoJ policy expectations in the nearer term.

- China begins its annual National People’s Congress in Beijing including the ‘Two Sessions.’ They’ll probably announce a 2024 GDP growth target of 5% again. Limited, targeted efforts to prop up growth are expected to be guided. Less is expected by comparison to last year’s game of musical chairs as key positions changed hands.

- China updates CPI for February on Friday night (ET). China was never in deflation to begin with in terms of the economist’s definition, but it is expected to end the media’s definition with the y/y rate popping back to the plus side of the ledger partly as the base effects that drove prior weakness in y/y readings are turning.

- Australia’s Q4 GDP arrives tomorrow evening (ET) and is expected to post mild growth of 0.2% q/q SA with some expecting no growth. The economy is decelerating.

- Japanese real cash earnings are expected to continue falling in y/y terms when January’s print is released on Wednesday evening (ET).

- Bank Negara Malaysia is expected to hold at 3% on Thursday.

Europe—The ECB’s Non-Event

- The ECB delivers a fresh statement and updated forecasts on Thursday. No policy changes are expected. Core inflation is delivering warning shots against premature easing so far this year as noted above. President Lagarde is likely to push back against any rush to ease while officials wait for key Q1 wage figures that arrive only by the June meeting.

- Eurozone Q4 GDP revisions on Friday will contain figures for wages in Q4, but again, the seasonality behind the collective bargaining exercises has the ECB focused upon Q1 data when it arrives months from now.

- The UK delivers its Spring Budget on Wednesday. Modest targeted stimulus is expected with a UK general election to be held not later than the end of next January.

LatAm—Peru to Cut Again

- Peru’s central bank is expected to cut 25bps again on Thursday.

- Colombia updates CPI for February on Thursday. It’s expected to jump by another 1% m/m NSA or so across both headline and core. That wouldn’t be terribly unusual compared to the normal pattern for February over time.

- Mexico core CPI for February will be updated on Thursday and is expected to rise by about 0.5% m/m NSA which would be fairly normal for a month of February.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.