ON DECK FOR THURSDAY, MARCH 28

KEY POINTS:

- Bonds sell off on hawkish Fed, BoE comments

- Canadian GDP to inform rebound prospects

- Fed’s Waller struck a somewhat hawkish note, with an asterisk

- BoE’s Haskel hawkishly disagrees with Governor Bailey

- Dovish comments from ECB’s Panetta were ignored by markets

- US GDP-r, PCE-r, claims, pending home sales on tap

- Early bond close in Canada and the US ahead of Good Friday

Hawkish comments from officials at the Fed and the BoE are contributing a rates sell off this morning. Dovish remarks by an ECB official are being ignored and perhaps justifiably. Other overnight developments were light and included German retail sales that were weak (-1.9% m/m, +0.4% consensus). Canadian GDP is the main focus into the N.A. session.

Fed’s Waller is in No Rush to Cut—Sort Of

Federal Reserve Governor Waller sounded relatively hawkish last night, but with an asterisk. His speech title “There’s Still No Rush” was a pretty big hint at what it would contain (here). He said “the risk of waiting a little longer to ease policy is small and significantly lower than acting too soon and possibly squandering our progress on inflation.” He also said “In my view, it is appropriate to reduce the overall number of rate cuts or push them further into the future in response to the recent data.”

He also said that he wants to “see at least a couple months of better inflation” before cutting. Ok, well, we’ll get three core PCE readings before the June decision including tomorrow’s and so technically Waller’s guidance is not incompatible with a June cut if all goes just peachily. Productivity appeared 26 times in his speech which apparently indicates its importance to him while stating “I am not convinced that the recent boom in productivity growth will continue” while going through a few arguments to state his case.

BoE’s Haskel Conflicts with Bailey

There is a bun fight going on at the BoE. After Governor Bailey struck a dovish sounding tone last Thursday by saying cuts were ‘in play’, the FT quoted Jonathan Haskel—an external MPC member—as saying that “I think cuts are a long way off.” He went on to say “what we really care about is the persistent and the underlying inflation.”

Why Dovish ECB-Speak Was Ignored

By contrast, ECB-speak was relatively dovish. Governing Council Member Fabio Panetta said that “Risks for price stability have decreased and the conditions for monetary loosening are coming about” while also noting “the rapid reduction of inflation.” His remarks didn’t really impact markets because they’re already priced for a June cut. His remarks could nevertheless be challenged. Eurozone core CPI m/m NSA has been registering relatively hot readings including February’s that was the second hottest month of February on record as we await the March readings and then wage figures before the June meeting.

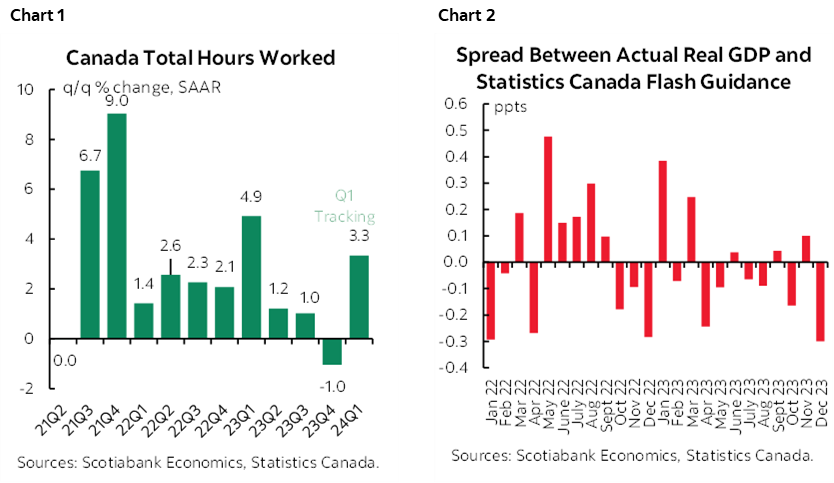

Canadian GDP—Tracking a Possible Rebound

Canada’s GDP figures for January and February will be the main thing on the macro calendar today (8:30amET). The figures are likely to feed into the rebound narrative. One key is what’s happening to hours worked (chart 1). 0.4% m/m SA is expected for January based upon Statcan’s initial ‘flash’ guidance that was provided on February 29th and little reason to depart from it based upon data since then. There is always revision risk based upon more complete information that Statcan has (chart 2).

More important may be the flash guidance for February GDP. I think momentum could be sustained but there are a lot of unobservable parts of the picture. Hours worked were up by another 0.3% m/m in February after a 0.6% surge in January. Housing starts were up by 13.6% m/m. Home sales took a breather after two prior gains so that may dent ancillary services. Flash guidance for wholesale and manufacturing activity offered solid nominal gains amid uncertainty toward translating that into volumes and value-added activity.

OTHER STUFF

Canadian bond markets face an early close at 1pmET today before being shut for Good Friday. There is no official early close for the TSX ahead of being shut for Good Friday.

UK GDP revisions were basically a non-event. US GDP and core PCE revisions are also on tap but expected to leave growth at or close to 3.2% and core inflation at or close to 2.1% q/q (8:30amET) along with other light US data including weekly jobless claims (8:30amET) and pending home sales during February (10amET).

The US bond market also faces an early 2pmET close ahead of Good Friday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.