| ON DECK FOR WEDNESDAY, MARCH 27 |

KEY POINTS:

- Yen intervention guidance heats up

- Sweden’s Riksbank turns incrementally dovish

- Spanish core inflation was unspectacular

- Australian trimmed mean CPI picks up

- SARB is likely to sound hawkish

- Ontario’s whining about the BoC is somewhat rich

- Likes and dislikes about the BoC’s productivity emergency

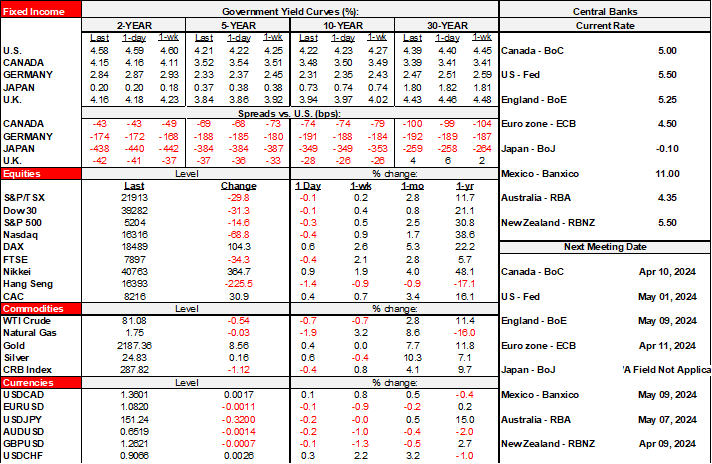

A smattering of developments abroad is offering little by way of macro drivers of market activity while there is nothing on deck in the US or Canada.

Speculation toward potential yen intervention continues to intensify. Masato Kanda with the MoF said “The recent weakening of the yen cannot be said to be in line with fundamentals, and it is clear that speculative moves are behind the yen’s fall. We will take appropriate action against excessive moves without ruling out any options.” This followed a meeting between the BoJ, the MoF and the Financial Services Agency. At 151.2, the yen is toward previous intervention territory and slightly appreciated after a volatile overnight session.

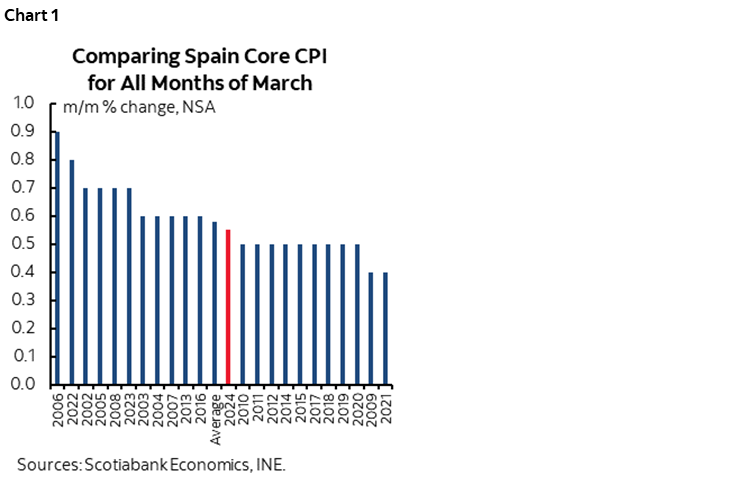

Spain offered a first hint at where Eurozone CPI may be going. We won’t get the EZ add-up until next week, but Spain’s core reading of 3.3% y/y (3.5% prior, 3.4% consensus) was a touch weaker than expected and the m/m core reading seemed in line with seasonal norms (chart 1). France and Italy are out on Friday. Recall that m/m core EZ CPI has been hot of late which should merit ongoing caution by the Eurozone on top of waiting for Q1 wage data before the June meeting. Spanish 2s largely shook off the reading and went on to cheapen by 1–2bps post data.

Australian trimmed mean CPI picked up to 3.9% y/y in February from 3.8% the prior month. Headline CPI was unchanged at 3.4% y/y. The alternative core measure that only excludes fuel, fruit and vegetables and holiday travel was up 3.9% y/y from 4.1% the prior month.

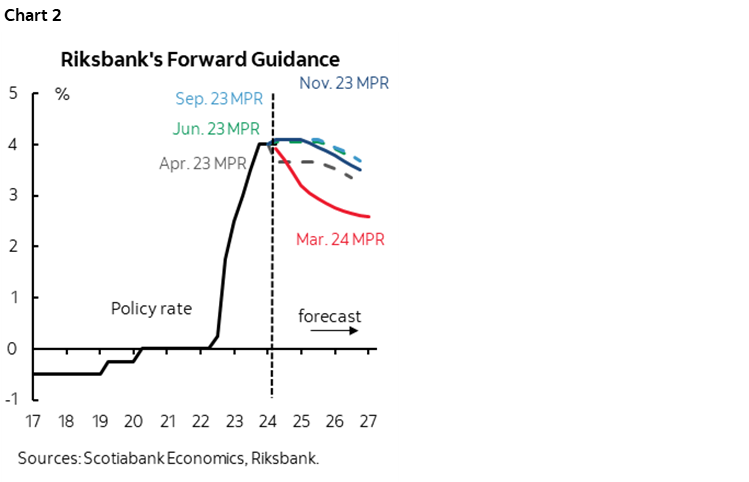

Sweden’s Riksbank backed up previously dovish talk with more explicit guidance that it could cut in the near term. While holding the repo rate at 4% as expected, guidance explicitly stated that “the policy rate may well be cut in May or June.” That follows previous guidance in February that a cut in the first half of the year “cannot be ruled out.” Inflation has been falling faster than the Riksbank expected and the economy slipped into recession. Markets were already pricing over 50% odds of a cut at the May meeting and post-statement moved that up to pricing about 21–22bps of a quarter point cut. The Riksbank’s projected policy rate path was revised markedly lower (chart 2).

SARB, on the other hand, has been dealing with firming inflation that is testing the upper end of the 3–6% inflation target range with core running at 5% and rising. A hawkish bias is likely a little later this morning (9amET).

Canada and the US face empty macro calendars today. The only Canadian budgets left are Manitoba on April 2nd and the Federal Government on April 16th and then that whole little cottage industry goes back to sleep. Fed Governor Waller delivers his economic outlook after the market close (6pmET).

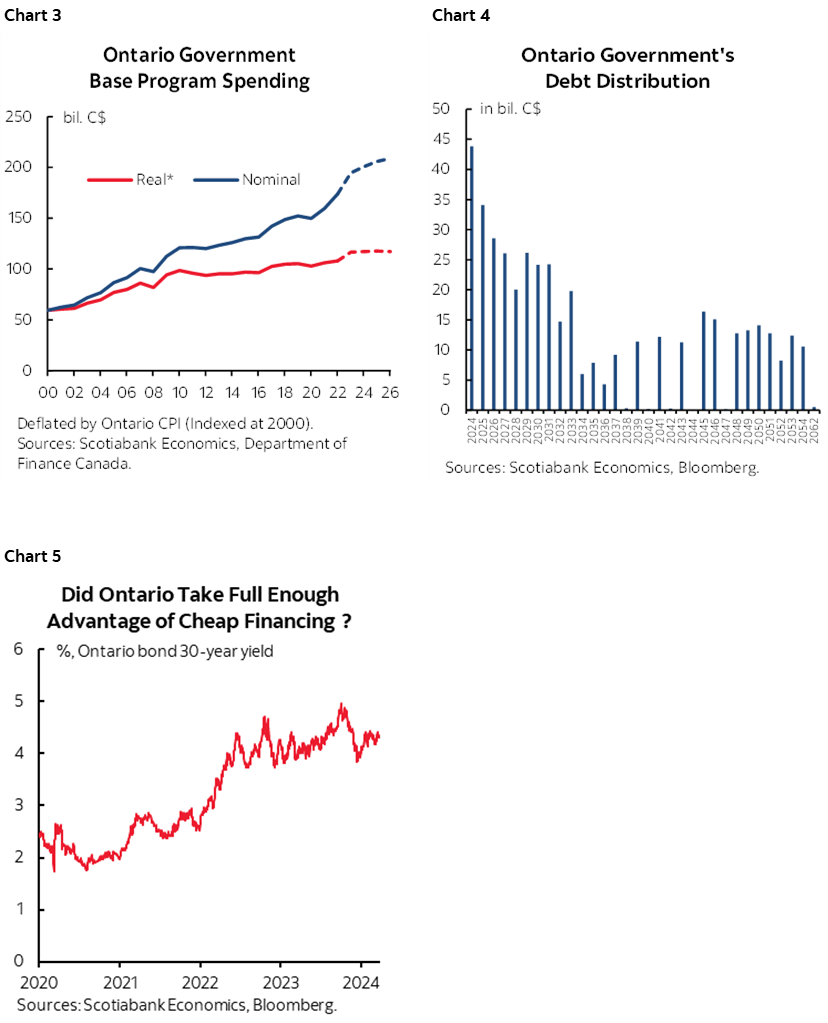

Yesterday’s Ontario Budget heaped on more spending. Gosh, what a surprise... The BoC says more spending complicates their task of getting inflation back toward 2% on a durable basis. The Ford government says that the BoC’s rate hikes complicates their task of being fair to Ontarians which forces them to spend more. How to settle this? Spending over time and as forecast by the Government is shown in chart 3. No wonder that Ontario wants the BoC to lower rates soon given its debt distribution and the refi wave that lies ahead (chart 4). With the benefit of hindsight but also given some opinions at the time, they might have taken fuller advantage of very low yields in the pandemic as sub-2% yields for long-term debt have since given way to around 4.3% now (chart 5). It’s a bit rich for Ontario to so stridently criticize monetary policy for the pressures on interest expense that it is facing especially since it’s not just the BoC versus broader forces governing the global and domestic bond markets. Go here for a recap of what the Budget delivered.

THE BoC’S PRODUCTIVITY SPEECH—LIKES AND DISLIKES

Failure to address longstanding poor productivity will carry three consequences that all Canadians have to understand as they make their choices.

- There will be a continued erosion of the standard of living at least in relative terms to countries that do a better job at it, if not in absolute terms.

- A further erosion of Canada’s relative competitiveness including within NAFTA and to Mexico plus the southern US. Mexico has not seen the rise in unit labour costs (productivity-adjusted employment costs) that Canada has experienced. More jobs would leave Canada over time and go to more competitive jurisdictions including the southern US and elsewhere.

- More inflation and higher borrowing costs for longer. Expanding the supply side through increased productivity is—all else equal—disinflationary and makes it more possible to have lower borrowing costs.

The Bank of Canada deserves credit for raising the importance of this issue in yesterday’s speech (here). It’s not that they said anything especially new, but their comments on productivity problems had previously been buried into press conferences and paragraphs within broader speeches. Furthermore, the BoC has wrongly called potential improvements in productivity in the past and so it was time for a bit of a come-clean stance. I’d flag one like and one dislike about the speech.

I liked the fact that the speech resisted any direct or indirect blame game at the expense of immigration policies, although in fairness nobody would have expected the BoC to court a headline blaming immigration. I’ve long written that a population shock has to be evaluated over time. The first-round effect may be lower real GDP per capita as the population surge outpaces output. The second and subsequent rounds may yield a very different outcome. It takes time—especially in a country like Canada—to integrate new arrivals. It takes time for them to have their foreign credentials recognized, to do what they have to in order to potentially meet Canadian requirements, to get a job, to start a business, to find a place to live whether to rent or buy, to start spending and to get integrated into the overall system. It could easily be that those effects are still ahead of us and Canada’s history demonstrates how difficult it can be to become fully integrated.

What I didn’t like about the speech was the finger wagging at businesses that was lacking balance which is unfortunately typical of Ottawa these days. The speech said “if I had to pick a biggest concern in this area, I’d say it’s competition” and went on to claim that “many sectors….face limited levels of competition” and this “can also help to explain Canada’s weak record in business investment.” That comment leveraged a Statcan research piece in February, but I didn’t like the tone that left the reader thinking the BoC condescendingly believes that businesses are just a lazy bunch and costing the whole economy. All stakeholders play a role in explaining weak productivity and in coming up with solutions; vilifying one of them is unhelpful. There are also other considerations that help to understand weak investment in Canada that are correlated with the concentration and competition trends over time, some of which are endemic to the nature of the Canadian economy.

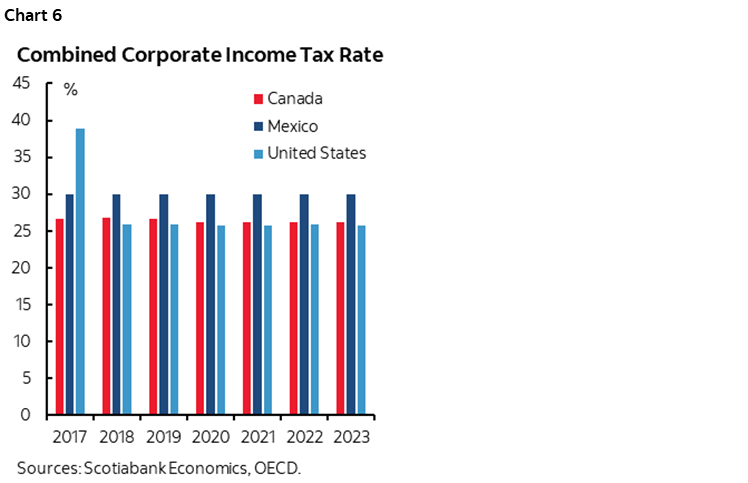

Absent from the speech was any attempt at explaining why businesses underinvest in a more fulfilling sense. Could it be because Canada once had a relative advantage on corporate tax rates that disappeared starting in 2018 as the Trudeau government and provinces chose a different path to the US (chart 6)? Could it be because most Canadian economic activity is driven by short-term spending on consumption, housing investment and government spending with 86% of GDP now allocated toward such activities which is floating around the highs observed in the late 1980s and early 1990s? Canada has been running current account deficits for about 15 years and mostly to fund consumption as public policy has been obsessed with short-termism. Could it be that serial CAD weakness makes it expensive to invest given that most capital goods are imported into Canada and particularly from the US? That one’s a chicken-and-egg argument since a weak CAD raises the cost of investment but perhaps also the reward if it’s to export and a weak CAD partly reflects poor productivity. Maybe BoC policy has contributed to all of this over time by always running to the rescue of any wobble in short-term spending and housing market activity which, until the past couple of years, reduced the rate pressures on businesses to invest more.

The speech was devoid of any policy suggestions which is also not unexpected given that the BoC tends to stay in its lane. How about leaning on the provinces to address interprovincial trade and mobility barriers that impair business competitiveness? How about effective immigration policy that brings in the right skills to complement expansionary investment? How about addressing uncompetitive tax policies that go well beyond just statutory rates? How about revisiting the government’s pro-labour and anti-productivity policies like overly generous supports for too long that prevented more efficient redirection of workers from underperforming sectors to ones that faced brighter prospects? I’ve long argued that labour policies over 2020–23 contributed to a lot more zombie jobs in this country relative to the US which came at the expense of productivity relative to, say, the US that ditched lower supports earlier than Canada. Canadian public policy always emphasizes bodies over productivity at times of uncertainty. Or how about revisiting actions that strengthened the hand of unions? How about had Canadian governments not driven record hiring of public sector workers for years, starving businesses of labour that would be complementary to investment? How about spending less on short-term stuff? How about revisiting pro-labour policies that have jacked up minimum wages and banned company flexibility to deal with strikes? How about resetting Ottawa’s finger-wagging tone that makes it look to international investors as if the country has an anti-business government? And if you want to open up Canada to more competition, then yesterday’s announcement restricting foreign investment in Canada was a curiously inconsistent step on the same day that the BoC was lamenting poor productivity and a lack of competition and investment.

In short, yes, Canadian businesses have long invested less as a share of GDP than US businesses while having lower technology adoption rates and less spending on R&D, none of which helps productivity. Some are stars, but we need more. Yet just blaming them without addressing what about the system may be causing this is intellectually dissatisfying, counter-productive and divisive. Ottawa could use some business-minded folks these days.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.