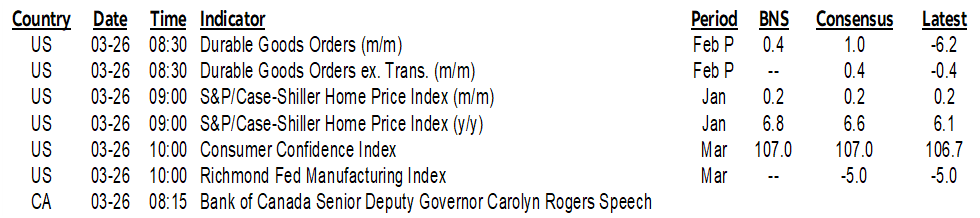

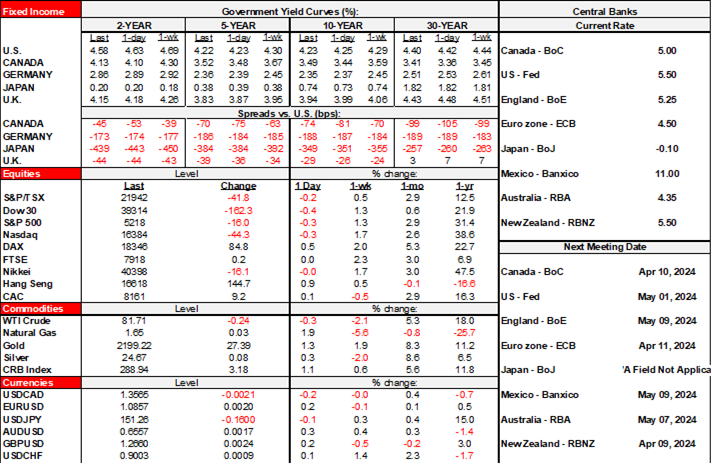

| ON DECK FOR TUESDAY, MARCH 26 |

KEY POINTS:

- Three things to monitor after a dull overnight market session

- The BoC to speak on productivity today

- Ontario to add to fiscal easing that negates monetary easing

- Consumer confidence to headline light US data

After a dull overnight session there will be three things to monitor today.

THE BoC ON PRODUCTIVITY

Senior Deputy Governor Carolyn Rogers will deliver a speech on “the urgent need to improve productivity” this morning (8amET). There will be audience Q&A but no press conference which seems to be a recent pattern.

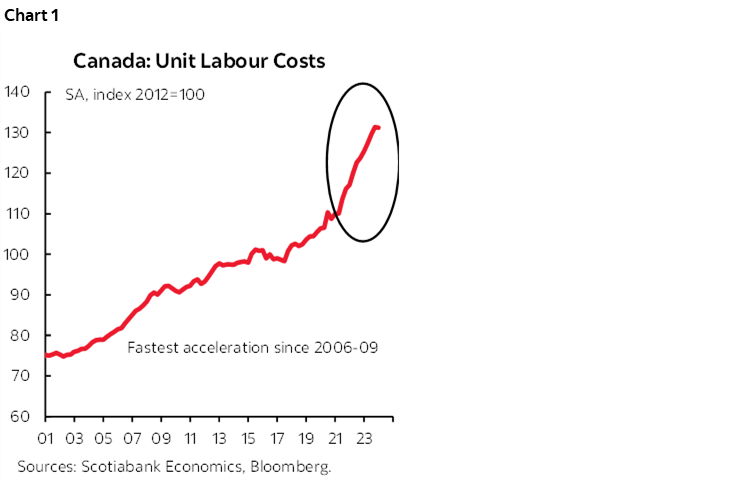

Productivity has been tumbling for an extended period now and it has underperformed the US for many years. Unit labour costs (ie: productivity-adjusted labour costs) started to accelerated after 2017 but really took off from 2021 onward (chart 1). Workers getting paid more than productivity justifies adds to inflation risk. See the Global Week Ahead for more charts and arguments on this.

Hopefully the BoC doesn’t bash immigrants, given the longstanding challenges and what I’ve long said to be the politicization of the narrative around the effects of immigration. I still maintain that it’s premature to judge the decline in real GDP per capita because a population shock unfolds in two or more stages and we’ve only seen part of the first stage so far. The second stage is about integrating new arrivals which may reveal a different picture for living standards. I would expect the speech to address the multiple drivers and also emphasize the implications for inflation if not addressed in an expeditious manner.

In any event, the BoC has misjudged productivity as illustrated by Governor Macklem’s past remarks that advanced the view that productivity would improve on the eve of what instead turned out to be an accelerated deterioration. In theory, tumbling productivity drags down potential GDP and limits the supply side’s ability to contain inflationary pressures at the margin.

LIGHT US DATA

Several US reports are on tap within about a 90 minute window this morning.

- The consumer confidence reading for March (10amET) may be the most relevant to markets. Confidence has been largely moving sideways for an extended period with the reading fluctuating within a band from 100–110 since early 2022. That’s off the peak in 2019 but still relatively elevated.

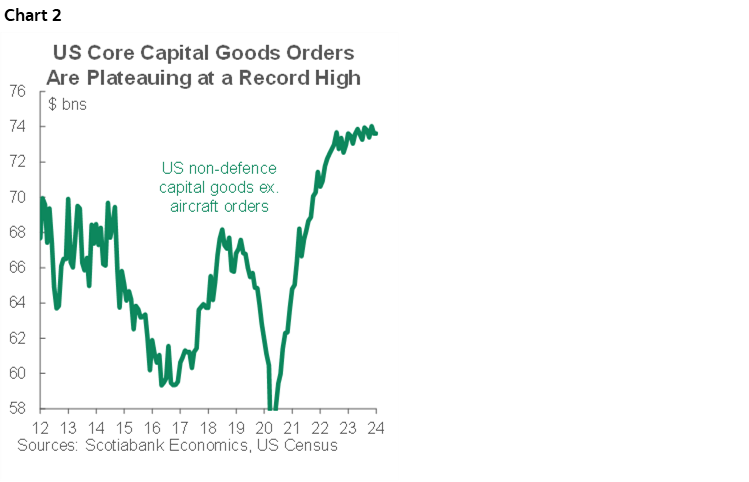

- US durable good orders for February (8:30amET) are expected to post a mild rebound after the 6.2% m/m drop in January. Still, the prior momentum in core capital goods orders (ex-defence and air) has been lost as appetite to invest has softened (chart 2).

- US repeat sale house prices for January are due at 9amET. House prices have been rising for 11 consecutive months.

- The US Richmond Fed manufacturing index for March (10amET) will help to further inform momentum in overall US manufacturing activity. Recent signals have been conflicting. The Empire gauge fell sharply, and both the Dallas Fed’s measure and the Philly Fed’s gauge slipped a bit.

ONTARIO’S BUDGET

Expect more spending on housing and infrastructure plus measures to address cost of living pressures. The latter will include an extension of the cut to the gasoline tax but also watch for more transfers. This added spending on the heels of similarly expansionist budgets by Quebec, BC and Alberta will reduce the ability of the Bank of Canada to eventually ease monetary policy. Expansionist fiscal easing negates or lessens potential monetary easing which means that Ontarians will pay more to borrow money for longer than would otherwise be the case. Finance Minister Peter Bethlenfalvy will deliver the budget just after 4pmET when markets shut.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.