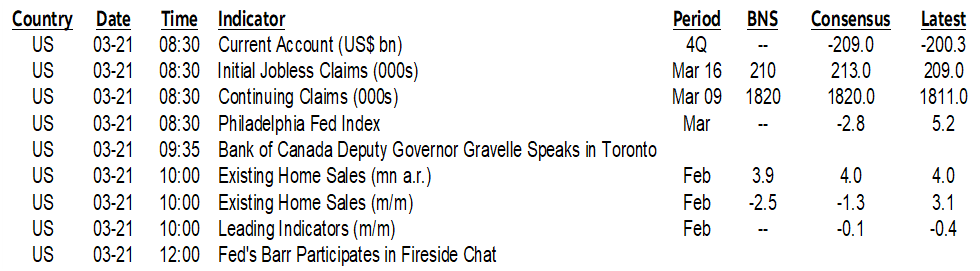

ON DECK FOR THURSDAY, MARCH 21

KEY POINTS:

- Central banks and data are spicing up markets

- SNB delivers a (mostly) surprise cut

- CBCT delivers a (mostly) surprise hike

- Turkey delivers a (mostly) surprise 500bps hike

- Australia posts huge gain in jobs, bonds sell off

- NZ slips into technical recession, prompting bets on RBNZ easing in 2024

- Global PMIs post improvements led by Japan

- BoC speech: Possible CPI reaction may matter more than balance sheet guidance…

- ...as an unexpected suite of BoC policy tools lessened the need to adjust QT

- Banxico likely to cut this afternoon

- Light US data on tap

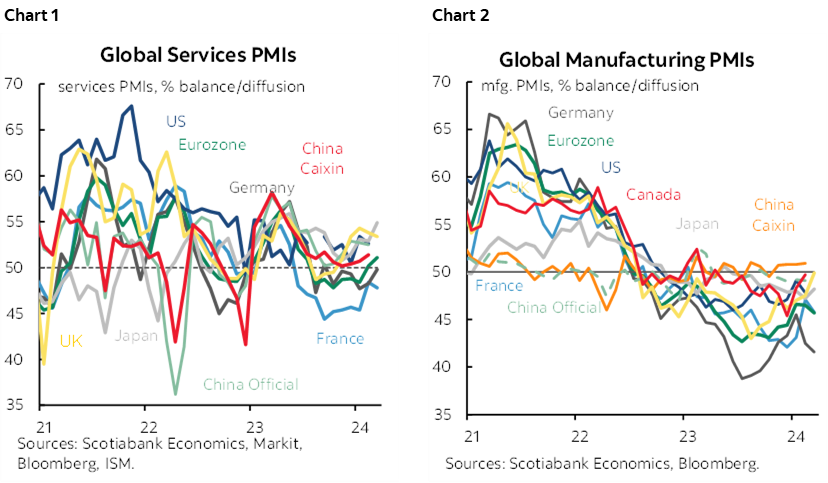

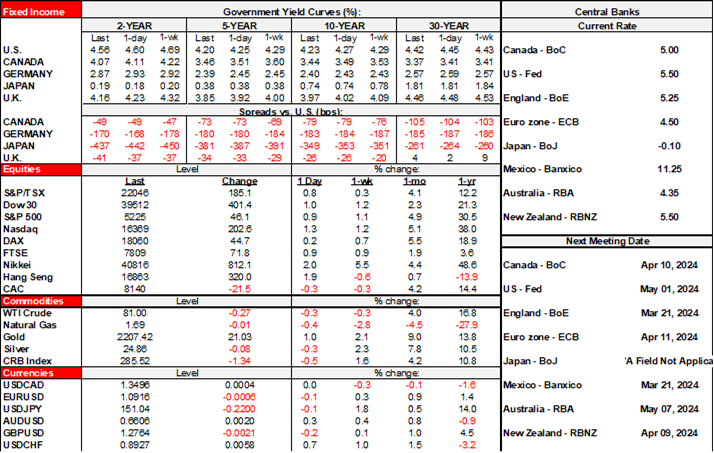

Central banks and data are spicing it up a little this morning and with more decisions and data ahead today. We’re getting a mixture of surprise hikes and a surprise cut as central banks diverge from one another to a degree. Data is informing some further relative central bank divergences with a particular eye on the Antipodean economies, while global PMIs generally improved (charts 1, 2). There is further mild follow-through on the FOMC’s communications (recap here) as the US and Canadian rates curves are rallying by another 4–5bps across both countries and all maturities.

A SWISS SURPRISE

The Swiss National Bank is the first among the fully developed economies to cut. It surprised with a 25bps reduction this morning. The move was only partly priced, and a small minority of economists called it. Inflation is already within range and the SNB lowered its inflation forecast even with a likely implied easing path. The franc depreciated on the back of the announcement and has been depreciating all year after a bout of temporary strength into the end of last year. Clearly, they have confidence that the ECB and Fed are moving toward cuts. Otherwise, the franc is even more vulnerable. The greater sense of urgency also has to be placed in the context of the reverberating effects of challenges in the banking system and the economy.

SOME OTHER POLICY SURPRISES

Turkey’s central bank surprised by delivering another mammoth 500bps hike to its one-week repo rate that is now at an even 50%. Yes 50%. Only one out of 21 forecasters got it right with almost all expecting a hold. In fairness, the new Governor had warned the last time they held that they were still of a hawkish mindset. Apparently so!

Taiwan's central bank hiked to 2% from 1.875% against widespread expectations for a hold. The hike was aimed at curbing high inflation, risk to inflation expectations, and pass through effects of a major hike in electricity prices.

Brazil's central bank cut 50bps as expected last evening and guided another 50bps cut the next time.

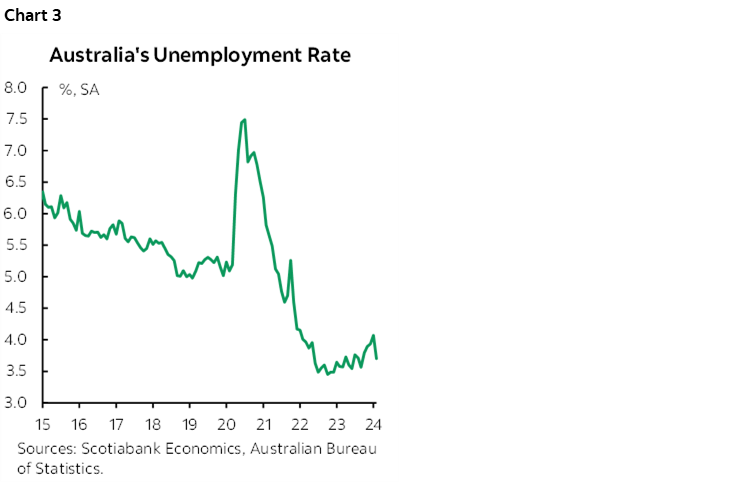

AUSTRALIA’S JOB MARKET IS ON FIRE...

Australia's job market roared to life with the creation of 116.5k jobs last month (consensus 40k). Most were full-time (78k). The unemployment rate fell back to 3.7% from 4.1% (chart 3).

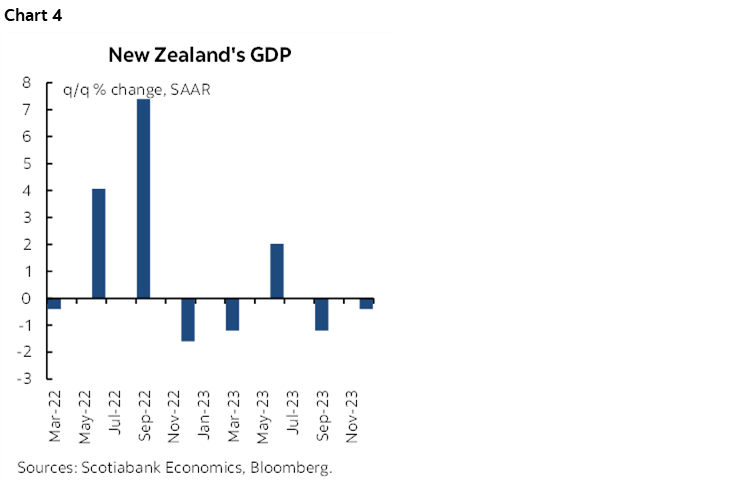

...BUT ITS NEIGHBOUR SLIPPED INTO RECESSION

New Zealand’s economy barely slipped into one definition of recession with back-to-back declines in quarterly GDP. Q4 GDP slipped by –0.1% q/q SA non-annualized after a prior drop of –0.3% (chart 4). That drove a bull steepener with the 2s yield down about 4bps overnight. More importantly, the NZ-AU relative spread widened by 9bps on the combination of weak NZ data and strong AU data which raises the prospects of incremental divergence in relative central bank pricing.

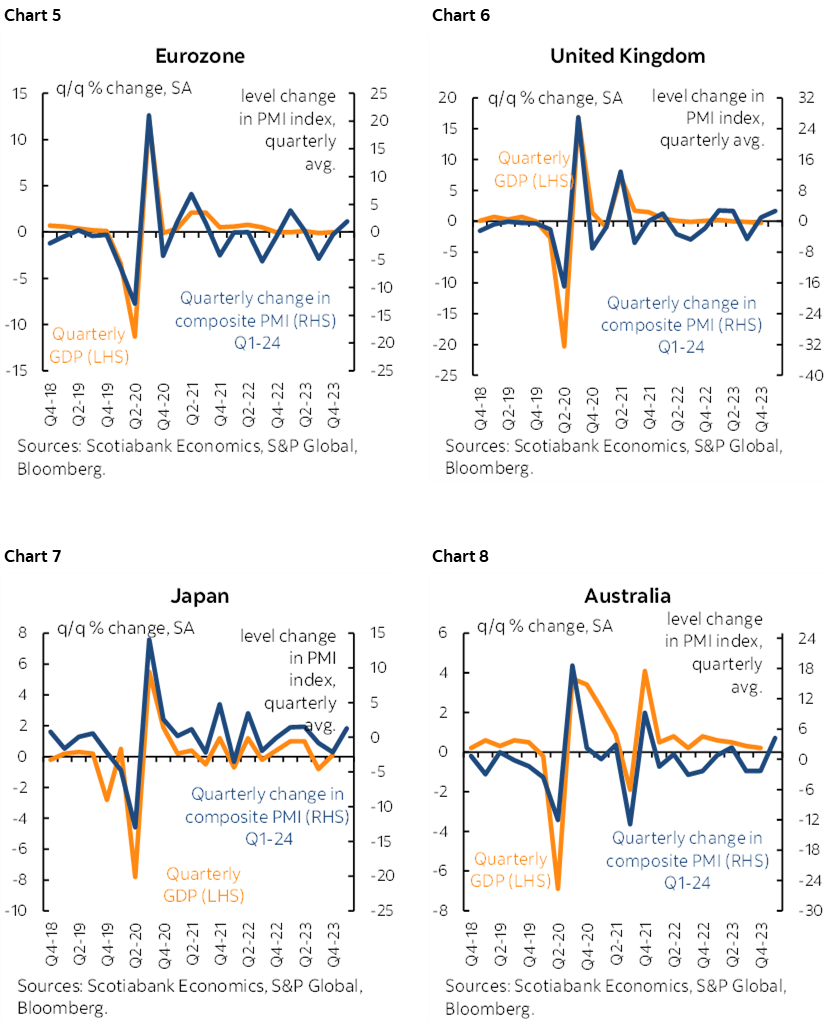

A POSITIVE ROUND OF GLOBAL PMIS

A round of global purchasing managers' indices can be summarized as follows and with charts 5–8 thrown in to show rough correlations to GDP growth over time.

- Eurozone: The composite gauge improved a little to 49.9, up 0.7, and thus signalling that the economy is roughly on the dividing line between expansion and contraction. All of that gain was in services as manufacturing slipped. It appears to have been driven by Germany and perhaps others, but not France.

- UK: The UK composite PMI was little changed as a mild improvement to manufacturing was offset by a mild deterioration in services.

- Australia: the composite PMI edged up by three-tenths to 52.4. That signals modest growth in the economy and the slight gain was all due to services as manufacturing slipped a little further into contraction.

- Japan: the composite PMI was up by 1.7 points to 52.3, signalling improved growth. Most of that was due to faster growth in services but the pace of manufacturing decline ebbed a little.

- India's composite PMI also improved to 61.3 for a seven-tenths gain. That indicates strong growth and the gain was spread across services and manufacturing.

On tap are several additional developments.

BANK OF ENGLAND — STILL PATIENT?

The Bank of England is expected to hold but watch for the possibility of more dovish guidance given recent data (8amET). I suspect they'll acknowledge it but say they require more evidence.

BOC’S GRAVELLE — CPI REACTION MAY MATTER MORE THAN BALANCE SHEET GUIDANCE

How did the BoC view this week's inflation report? That might be the most important part of Deputy Governor Gravelle's speech today (9:35amET) with audience Q&A but no presser. I expect him to say that a pair of soft core prints is encouraging but that they need a lot more data and that they remain concerned about inflation risk. Whippy markets are behaving absurdly in response to a lousy pair of soft readings with big question marks around them.

Gravelle's comments on the balance sheet are unlikely to be that meaningful after Macklem previously said that no QT changes were afoot. Why? Because they've thrown repo injections, receiver general auctions and likely cash management bills at the distorting QT consequences alongside the effects of indigenous payments moving into settlement balances and the signalling effects that they'll do more such things if necessary to contain CORRA-o/n spreads.

If not for these actions and the more important signalling that the Fed is moving toward tapering QT that carries spillover effects across North American funding markets, then the BoC would have very likely had to adjust QT itself. Those who said that the BoC would not have to adjust QT generally did not expect any of these developments, some of which have compounded distortions in funding markets. That’s a bit absurd in my opinion. Perhaps also absurd was SDG Rogers’ claim that the earlier CORRA-o/n spread widening wasn’t due to QT distortions and was just due to funding demand around rate cut expectations. CORRA-o/n was widening since late last summer when no one was talking rate cuts so I don’t know how that argument stands the test of time.

Regardless, the BoC is determined to continue its QT plans through to fruition unless we get another surprise from them today. Their prior guidance was to continue with 100% roll-off until the end of this year or early next.

It might have been nice to have a presser for this one, but maybe they axed the idea after Governor Macklem’s earlier remarks made much of the speech pointless.

LIGHT US REPORTS

There will be light macro reports out of the US including weekly claims (8:30amET), the Philly Fed measure as input into ISM-manufacturing expectations (8:30amET), the S&P PMIs for March (9:45amET), and existing home sales during February that are expected to slip after the prior month’s gain (10amET).

MEXICO’S CENTRAL BANK TO CUT

Banxico might be next up to cut 25bps this afternoon and therefore join most of its LatAm peers (3pmET). Twenty-six out of 29 forecasters expect a cut plus our economist colleagues in Mexico who are not in the Bloomberg survey, making for 27 out of 30 in total.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.