ON DECK FOR TUESDAY, MARCH 19

KEY POINTS:

- BoJ and RBA actions ripple through global markets as the FOMC meeting begins

- BoJ’s Ueda basically ended most of Kuroda’s policies…

- …with a cautious forward tone that drove yen depreciation

- RBA shifts toward more open-ended rate guidance

- Was January’s soft Canadian CPI an anomaly?

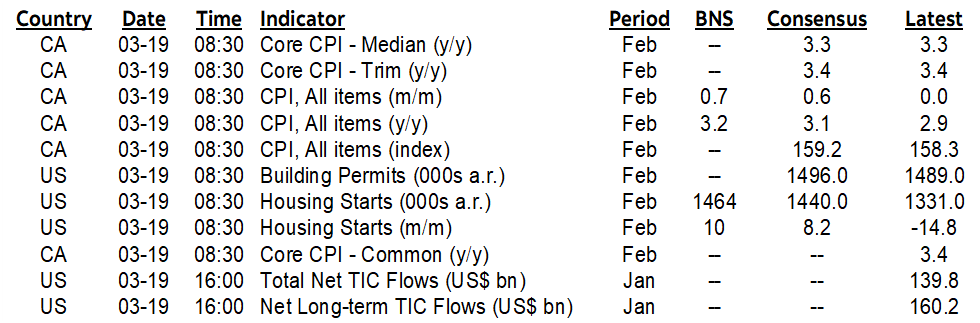

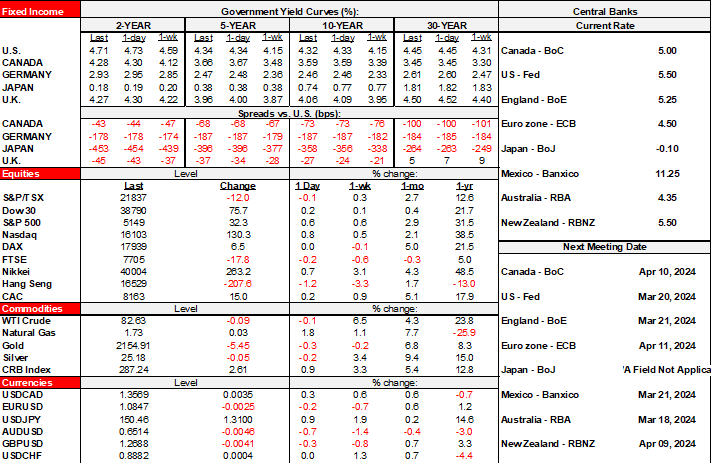

Buy the rumour, sell the fact? That seems to be the reaction to the BoJ’s actions overnight as the yen depreciated from about 149.3 to the USD into the statement to 150.50 now (chart 1). Mind you, some of that is due to a broadly based appreciation in the USD. The Nikkei rallied again and the JGBs curve slightly bull flattened with the 10-year yield down by about 3bps. The BoJ’s moves combined with modest changes to the RBA’s guidance are contributing to a mild rally across global sovereign curves. Effects on global equities are mixed as N.A. futures decline, London is flat, and the rest of Europe is up a bit. Canadian CPI could put a twist on the local narrative this morning. Also in the background which may be driving USD strength is speculation that the FOMC will reduce projected rate cuts in tomorrow’s dot plot as it commences its two-day meeting today.

WHAT THE BANK OF JAPAN DID

The BoJ raised its target rate from -0.1% to a 0% to +0.1% range and now uses the unsecured overnight call rate as its policy rate. Governor Ueda’s press conference delivered a dovish tone by emphasizing a need for ongoing accommodation that provided no hints of future hikes. It ended its formal yield curve control program including the 10-year yield target with Ueda saying markets will drive yields, but retained more flexible JGB buying while saying they will lean against any sharp increases in yields. It ended purchases of ETFs and REITS and guided that purchases of commercial paper and corporate bonds will be gradually reduced. No guidance was provided on plans for its existing US$475B stock of ETFs as speculation over what to do with it remains rampant.

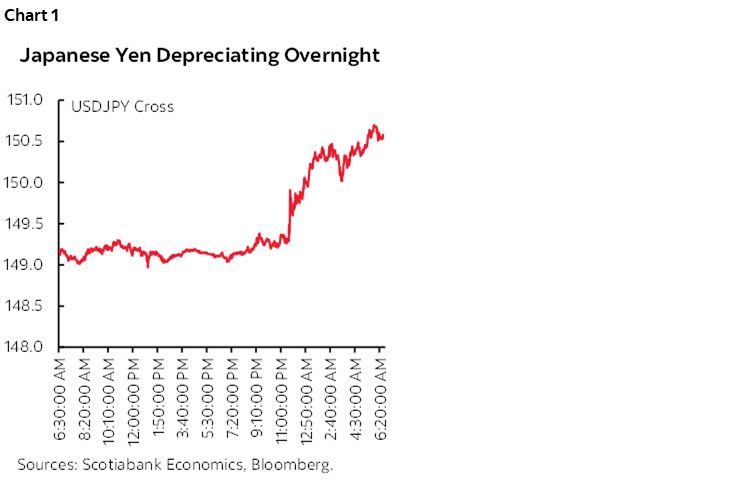

In a sense, the BoJ has merely caught up to the fact that negative yielding global debt has been thoroughly wiped out (chart 2). A market that once pushed toward US$18 trillion of such debt had moved toward basically nothing quite a while ago. There are risks aplenty to what the BoJ has done and this only commences the experiment that basically amounts to Ueda scrapping the central tenets of former Governor Kuroda’s framework. What if wage growth at large companies (chart 3) falls back down given the lack of productivity supports? What if wage growth at large companies still doesn’t trickle through to lift the wages of the vast majority of Japanese workers (chart 4)? What if inflation fails to sustainably achieve the 2% target and the rise was driven by transitory factors? Hence some of the reasons for why the decisions had some dissenters on the Board.

RBA SHIFTED TOWARD MORE OPEN-ENDED FORWARD RATE GUIDANCE

The A$ was the second worst FX performer to the USD overnight and Australia’s rates curve outperformed other global benchmarks with a bull steepener move. The RBA held its cash rate target at 4.35% as universally expected. The statement dropped the reference to how “a further increase in interest rates cannot be ruled out” and replaced it with “the Board is not ruling anything in or out” on the future rate bias which is now more open-ended. The statement suggested that wage growth may be peaking but remains high and is only compatible with achieving the 2–3% inflation target range if productivity accelerates, given that unit labour costs are high.

GERMAN INVESTORS MORE CONFIDENT THAN BUSINESSES

German investor expectations accelerated with the ZEW measure rising from 19.9 to 31.7. That continues the upward trend that has been in place since August, but the markets community is recently more upbeat than businesses given that the IFO expectations measure has been moving sideways.

WAS CANADA’S SOFT INFLATION PRINT IN JANUARY AN ANOMALY?

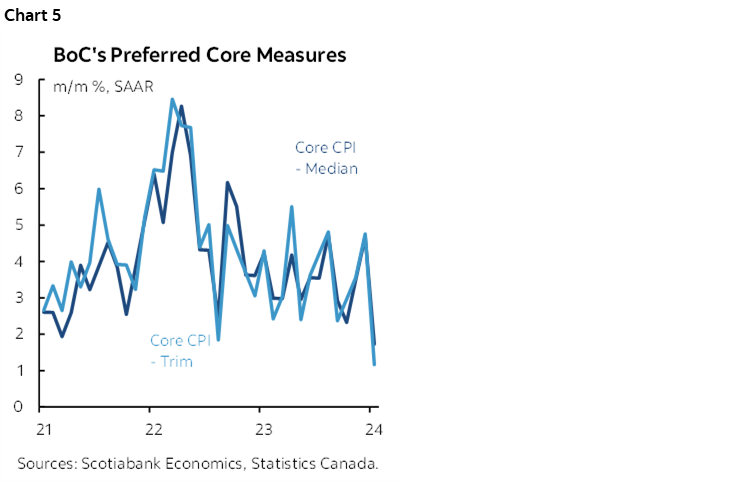

Canada will update CPI inflation for February this morning (8:30amET). I've gone with 0.7% m/m NSA, 0.4% m/m SA and 3.2% y/y from 2.9% prior. February is normally a significant up-month for seasonal price increases. Key will be the trimmed mean and weighted median gauges in m/m SAAR terms. January was a soft patch along a previously hot trend and so whether that was an anomaly or the start of a trend may be influential to markets (chart 5). I think it was more of an anomaly. Some effects, like abnormally mild and dry winter weather due to El Nino, may persist but if this continues into Spring it could whip the affected categories around in the other direction.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.