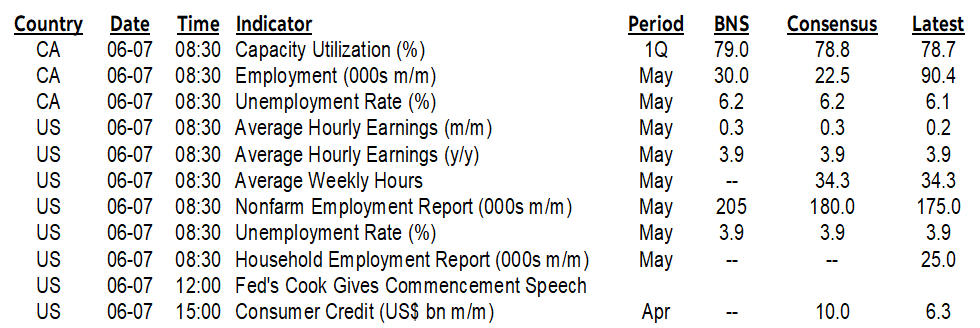

ON DECK FOR FRIDAY, JUNE 7

KEY POINTS:

- Markets await US, Canadian jobs

- A truly bizarre week for global central banks

- Advance readings point to solid US payrolls

- Can Canada follow up April’s strong job gain with another?

- US, Canadian wage growth could be key after prior cooling

- RBI, Russian central bank both held as widely expected

From wonky sounding central banks we can now turn our attention back to the good ol’ fundamentals this morning. Markets are treading carefully as usual before a US payrolls report as both bonds and equities have a mild cheapening bias. Brace for a lot of volatility into the end of the week with potentially significant effects on Fed and BoC pricing. Most of the focus will be upon US and Canadian jobs reports that arrive at 8:30amET. Regional markets may be impacted by a pair of LatAm inflation prints (Mexico & Chile at 8amET). The RBI held as expected overnight and so did Russia’s central bank this morning against some speculation that another hike could be in the works. Brief jobs previews follow.

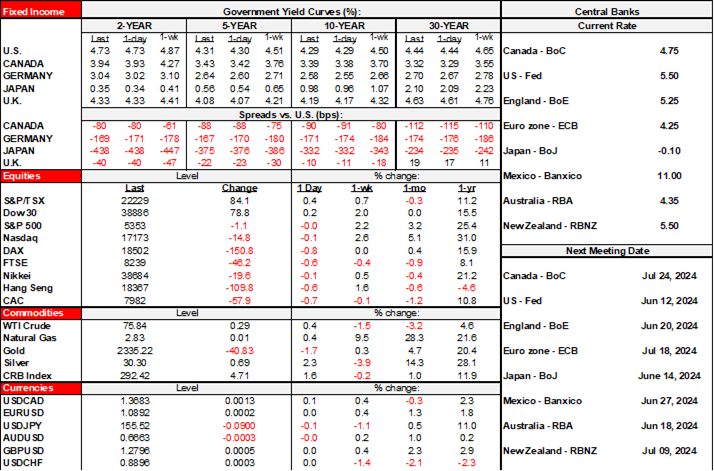

But first, what a bizarre couple of days in the annals of global central bank decisions. I swear that the prime reason both the ECB and the BoC cut was simply to be able to say they did it before the Fed in a symbolic sense. I can't recall weaker justifications or wonkier guidance at the potential start of easing cycles.

- The ECB stuck to forward guidance and cut when it arguably shouldn't have given the evidence to date and then trips over itself to basically apologize with low conviction and no commitment throughout the whole press conference. It was like “we’re cutting, sorry.” They cut after months of saying they wanted to see wage data and that wage data ripped, yet they still cut, and with core inflation still running hot. Then the rebels come out immediately after the press conference in anonymous reports and douse Lagarde's zero forward commitment with a commitment to do nothing over most or all of the rest of the summer. Clearly they did not agree with Lagarde’s “I’m in charge” necklace that she wore during her presser.

- The BoC cut starkly against the Governor’s forward guidance and threw all caution to the wind in a package of views that are low on the believability scale across multiple points as previously covered.

CANADIAN JOBS PREVIEW

90k jobs created in April—the largest number since January of last year—may present a high bar to post a repeat gain in May’s numbers. The only one in consensus to go negative did it just for optics as -5k doesn’t matter especially given a large +/-57k 95% confidence band around the survey estimates. All others went with a gain from +10k to 96k but with most in the 20–30k range.

An upside risk is ongoing strength in population growth through immigration that is filling job vacancies while perhaps also spurring the creation of new businesses albeit there is no clear evidence of this as yet. New business openings have been flat over the past year, but may have been lower if not for high immigration.

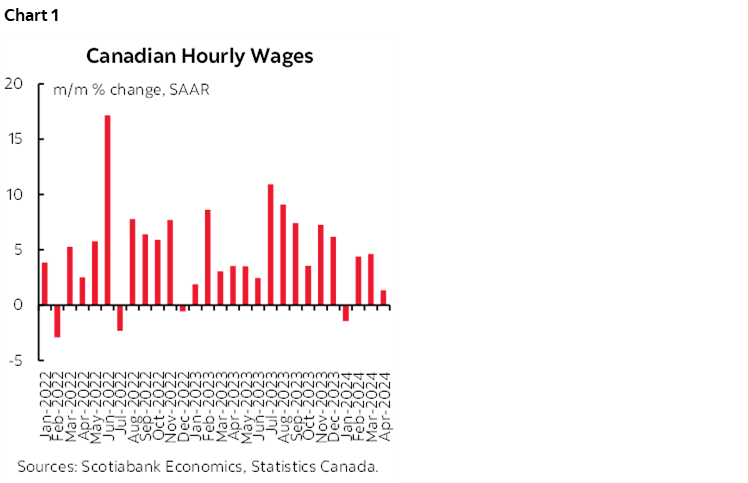

Key is also whether wage growth reaccelerated after hitting a soft patch in April shown in chart 1 (+0.1% m/m SA). Also watch hours worked since they are tracking a powerful gain so far in Q2 and that points to strength in the economy. The large gain in hours during April could be tough to follow.

A weak report either on headline and/or details and Macklem says told you so. A strong report tamps down July cut pricing.

US NONFARM PAYROLLS PREVIEW

The US labour market is looking a little more like Canada these days, although definitely not in terms of the trend in labour productivity. The US resembles Canada in a lighter version of the impact of population growth on filling vacancies.

Estimates for today’s payrolls report for May (8:30amET) mostly fall within a rise of 150k to about 200k with a median call for 180k. The whisper number is no different at 167k. I went toward the high end of estimates partly on the population effect that may prove to be transitory as Biden tries to get ahead of Trump on border control and re-electing Trump risks crushing labour force growth once again.

The 90% confidence white noise band on changes in nonfarm payrolls is about +/-130k and so no one is outside of that realm.

Most within consensus expect a little firmer wage growth after only 0.2% m/m SA in April (chart 2). That could matter at least as much as the jobs print.

Most of the advance drivers of potential US job growth in May that go beyond population growth are constructive:

- Consumer confidence ‘jobs plentiful’ fell in May

- NFIB small business hiring plans increased

- NFIB small business hard to fill positions also increased

- ISM-services employment slightly improved

- ISM-manufacturing employment significantly improved

- JOLTS job openings fell (latest April), either signalling a pick up in filled spots or cooler openings

- ADP payrolls landed at 152k

- initial jobless claims moved roughly 10k higher between nonfarm reference periods in April to May

- Challenger job cut announcements were stable at around 64k/mth in each of April and May, down from 82–90k per month in Q1. This supports the thesis that seasonal layoffs on initial pandemic hiring is being driven by companies into the start of new fiscal years.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.