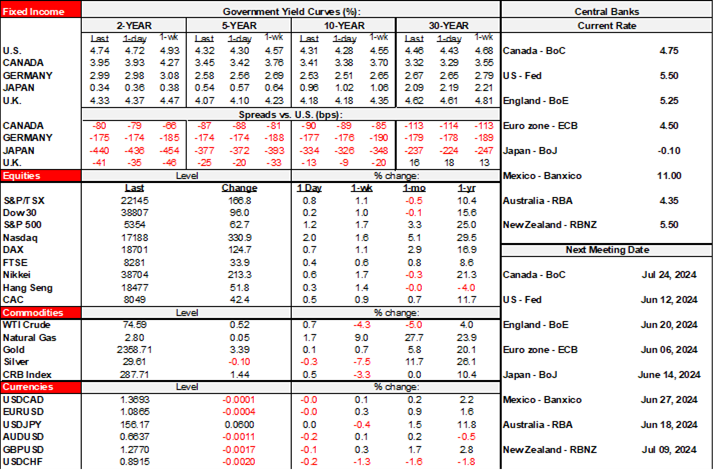

| ON DECK FOR THURSDAY, JUNE 6 |

KEY POINTS:

- Equities rallying ahead of the ECB

- The ECB is fully expected to cut today when it arguably shouldn’t…

- ...which should make it reticent to provide explicit forward guidance

- Gilts rally as a BoE survey showed slightly lower inflation and wage expectations

- BoC forecast update

- Minor N.A. data on tap

NA equity futures are flat as European stocks rally ahead of the ECB. EGBs and Treasuries are slightly cheaper as gilts outperform after a BoE survey was released showing that CFOs expect cooler wage growth and very slightly cooler price increases over the next year of 3.9% compared to 4% in the prior survey.

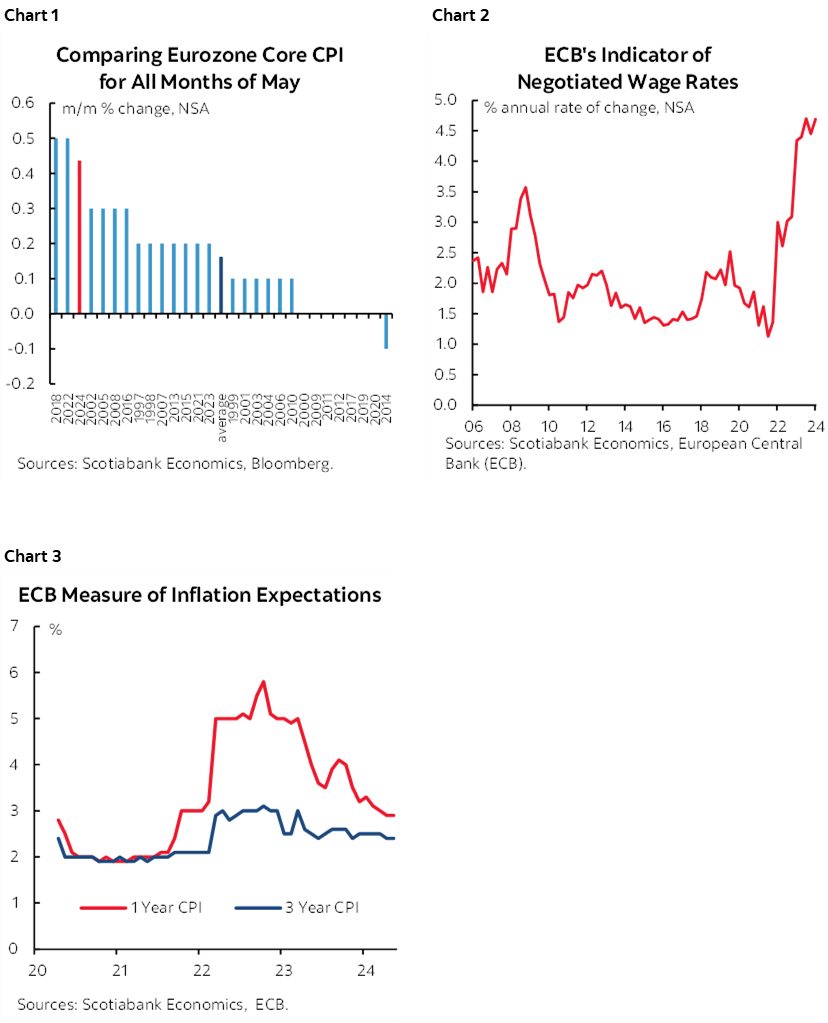

ECB—Why Exactly Are You Cutting?

And now it’s the ECB’s turn. A cut to a new deposit rate of 3.75% is widely expected, fully priced, and publicly supported by key ECB officials. Key, however, will be the forecasts and Lagarde’s verbiage insofar as they may inform the path forward. July is basically priced for a hold and September is mostly priced for another cut. Statement 8:15amET, press conference 8:45amET.

Cutting is not what the ECB should be doing today in my view. Core inflation in m/m NSA terms compared to like months in history has been putting in hotter and stickier than usual readings every month this year (chart 1 shows May, for example) and so if they are truly data dependent rather then being on a year-long preset course to ease then they wouldn’t be doing so now. You might say they need to cut in anticipation of achieving their inflation target, but their inflation forecasts perform poorly, and model-based forecasts always anticipate perfect equilibrium and achievement of the target within the forecast horizon. Negotiated wage gains are very high (chart 2). GDP growth is on the mend. Inflation expectations have come down but are still above target (chart 3). Therefore, if they’re forcing a cut today for impure reasons—maybe bragging rights ahead of the Fed or messy European politics—then why commit to the next move today?

Minor Other Data

German factory orders fell by -0.2% m/m (+0.6% consensus) in April with negative revisions (-0.8% m/m from -0.4%).

Minor data is on tap into the N.A. session. Canadian trade during April may further inform Q2 GDP tracking (8:30amET). We already know most of the US trade figures through the advance goods component that showed a wider US trade deficit (8:30amET). US weekly jobless claims offer low risk ahead of tomorrow’s more important nonfarm payrolls.

What’s the Real Reason Macklem Cut Against His Own Forward Guidance?

Canada may also monitor any spillover effects from yesterday’s BoC cut (recap here). Markets have 15bps of a cut priced for the July BoC which is about right for now as we go into several rounds of data before the decision. There are 3+ 25bps cuts priced in for this year. Our forecast is for 100bps this year with cuts in July, September and October and we’ve penciled in a December pause due to US election uncertainty for now and because we think the BoC will want to deliver a meaningful amount of easing before then deciding whether to continue or pause and assess.

The frustrating thing is that Scotia Economics had a June cut call ever since last June as we led consensus, but punted to a first cut in Q3 this past February. We got the mid-year cut call right ahead of others but missed on the exact meeting. I can live with that because we listened to Macklem’s guidance ahead of the meeting but certainly won’t do so again.

Knowing Macklem’s past behaviour, the prime motive for cutting may have been so he could say that he was first among majors and semi-majors to cut while stealing the ECB’s thunder, even though it meant violating his own forward guidance. They are quite proud of the fact they were first to begin tapering QE and then shifting to QT, even though they totally messed up on the policy rate during the pandemic. That’s a puerile motive if so.

And yet I’m still stunned about the attitudes Macklem portrayed in the presser.

- Saying they are ‘not close’ to the limit of Fed policy divergence was curious. Try going 150–250 points below the Fed and let’s see what happens.

- You can’t say just one month before the decision that you want several more months of data before deciding when to ease and then turn around and cut and not be held accountable for your terribly unreliable forward guidance. One media report misquoted me as saying Macklem had said this months ago when in fact what I pointed out was that he said it just one month before the meeting! Something happened in the intervening period and I don’t believe that one round of data did it when he was clear in advance that we wanted more than just one round.

- Ambivalence toward the currency went too far; we know full well there is a limit to the extent to which the BoC would tolerate a currency in free fall and it’s about more than just inflation pass through. Excessive currency volatility in an open economy that trades a lot can dampen business confidence and investment plans. A weaker currency is a disincentive to invest because it lowers the pressure on exporters and raises the cost of importing machinery and equipment given so much of it comes from the US. Always resorting to debasing the currency can turn a country into one that competes more on price every time a bump in the road arrives rather than on innovation, investment, R&D, adopting new technology and coming up with better products. Maybe the BoC is part of the productivity problem. CAD would be bathroom wallpaper if the BoC dove deeply beneath the Fed and yet I’m pretty sure the BoC would get rather antsy the further into the 1.40s that USDCAD pushes.

- Macklem cherry-picked the evidence on the economy’s performance. He flagged Q1 GDP being weaker than the April MPR forecast while avoiding mention of the fact that final domestic demand grew strongly, GDP was weak mainly because of inventories, and the economy over H1 is significantly stronger than they had anticipated coming into the start of the year. He offered no explanation of why the BoC would cut when the evidence shows that consumption is growing by 3%+ q/q SAAR in each of the most recent two quarters as the mortgage hysteria ignores the fact that consumption is growing strongly.

- I disagree with his view that the economy is super weak in per capita terms for the same reasons I’ve been writing for a while. You can’t include all of the surge in non-permanent residents that are the ones who have driven so much of the population growth because they can’t be expected to contribute to GDP growth in proportionate fashion to those born in Canada and permanent immigrants. The temps are made up of asylum seekers, temporary foreign workers who send their paycheques home and take back with them what’s left over after spending on the means of subsistence in Canada, and international students of varying types from genuine to fakers who are exploiting loopholes to get permanent residency with neither type contributing much to the economy at least not while during school. And GDP, in my opinion, was depressed since 2022Q4 by factors such as inventory shedding, wildfires, rampant strike activity and lost hours worked, and sector-specific retooling and maintenance issues at major auto and resource facilities. Hikes are working, but for the central bank to ignore the other things that have dampened GDP growth is going much too far.

We’ll see how this all turns out. Where the clash of narratives is most acute, however, lies in the fact that the BoC is convinced that Canada has much bigger troubles than the US and lower inflation risk as justification for easing and being open to potentially much bigger undershooting of the Fed. I’m much more uncertain. Wage growth is getting no support from labour productivity that continues to tumble. Fiscal policy is still adding to growth this year and next and the risk is that it adds even more into an election year given how badly the Federal government’s left-wing alliance is polling. If monetary policy continues to ease and vote-grabbing fiscal stimulus ramps up then inflation risk will be resurrected. Mortgage resets remain an over-hyped risk.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.