| ON DECK FOR TUESDAY, JUNE 4 |

KEY POINTS:

- Widespread risk-off sentiment ahead of the week’s main developments

- Oil’s slow response to OPEC+

- Indian stocks hammered as Modi won’t secure as much power as thought

- Swiss inflation adds to June cut pricing

- US retail sales are tracking softly

- US JOLTS to start the week’s focus on the US job market

The usual currency havens—the dollar, CHF, JPY—are outperforming other crosses on this morning’s jolt to risk appetite. MXN is depreciating by another almost 2% to the USD this morning in the ongoing aftermath to the election results. Oil prices are down by under 2%. Stocks are lower by around ½% to ¾% across NA futures and between 0.5% and 1% in Europe. Sovereign bonds are slightly dearer across most major benchmarks. This is happening before the week’s main events that start tomorrow.

Oil’s Slow Response to OPEC+

Energy and materials are driving much of the decline in equities. London’s FTSE 100, for example, is being dragged down by declines of 2.8% and 2.3% for energy and materials subindices respectively with other sectors mixed between mild gainers and losers. It took a while for markets to respond to the OPEC+ plan to ease away from production declines starting in October, as oil prices started to drop only at around 9amET yesterday morning after Asian and European markets shrugged, and oil prices continue to decline this morning. General pessimism toward the health of the global economy may be adding to this sentiment; at this rate, give that another day and another couple of indicators and markets might be jubilant again.

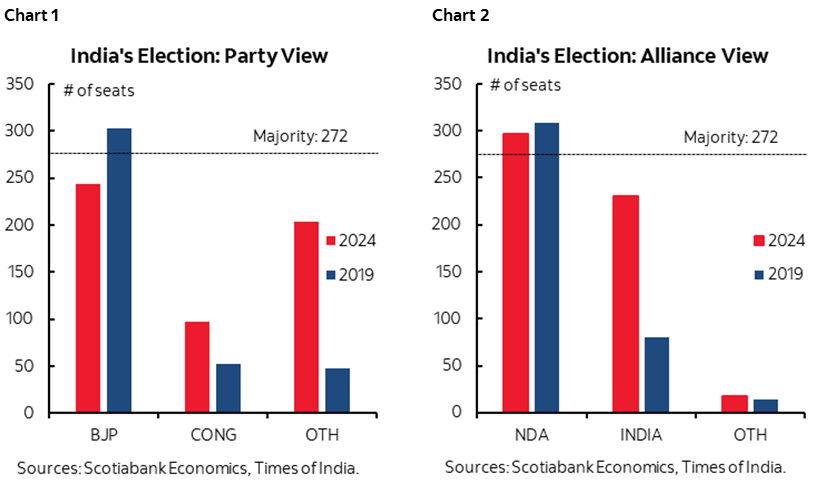

India Delivers a Reminder that Polls Can be Very Wrong

India’s stock market is getting hammered with a decline of about 6% for the biggest single day drop since the early days of the pandemic. The country’s curve is cheaper by 7–9 bps across maturities. The rupee is slightly depreciating to the USD. The culprit? We just got yet another reminder that polls can be wrong. Very wrong. Take that, Trump. Narendra Modi’s Bharatiya Janata Party may not secure a majority on its own after all, based on ongoing vote counting (chart 1). The BJP will have to rely upon the National Democratic Alliance to form a coalition government and the coalition seems to be on track to win far fewer than the targeted 400 seats as it leads in 280 with 272 required for a majority (chart 2). A much narrower victory than exit polls were suggesting and that is dependent upon a coalition partner dampens enthusiasm that Modi will be able to pursue as many reforms that are needed but may serve as a check on his autocratic tendencies. Modi, it seems, isn’t as popular among Indian voters as thought even just a day ago.

SNB Cut Pricing Increases Post-CPI

The strength of the Swiss franc is despite a soft core inflation reading of 1.2% y/y (1.3% consensus). The result for May added about 3bps to June cut pricing with the SNB now a little better than 50–50 odds to cur on June 20th.

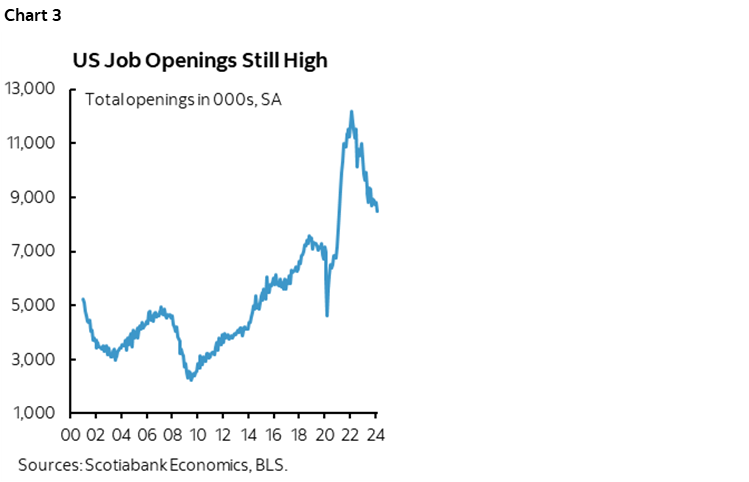

US Job Vacancies on Tap

US JOLTS job vacancies may pose the most calendar-based macro risk this morning (10amET). They’ll merely tease ahead of Friday’s nonfarm payrolls. First, they lag, since they are for April whereas Friday’s payrolls are for May. Second, we often can’t tell if a decline or rise is due to a change in new vacancies or a change in the pace of filling pre-existing ones. Still, markets can react to the JOLTS figures in the warm-up to payrolls. Vacancies have declined, but remain high (chart 3).

US Retail Sales Are Tracking Softly

US retail sales are not tracking very well based upon partial information. Late yesterday’s US vehicle sales climbed to 15.9 million SAAR in May for a 1% m/m SA gain that was close to the industry guidance of 16 million that was based on tracking for part of the month. On its own, that adds about 0.1–0.2% to expectations for May’s retail sales which should be offset by tracking a decline in vehicle prices that should dent next week’s CPI as well. Gas prices also fell by about 3% m/m SA in May. That leaves a gain in retail sales on June 18th dependent upon a renewed pick-up in core sales ex-autos and gas.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.