| ON DECK FOR MONDAY, JUNE 3 |

KEY POINTS:

- Stocks, bonds have richening bias to start a fresh week

- Most of the week’s developments unfold in the back half

- Markets are frowning upon Mexico’s election results…

- …but gleefully welcoming India’s polling estimates ahead of official results

- Oil prices largely shaking off OPEC+ surprise

- US to update ISM-manufacturing, vehicle sales, construction spending

- Canada to update manufacturing PMI

- Global Week Ahead reminder

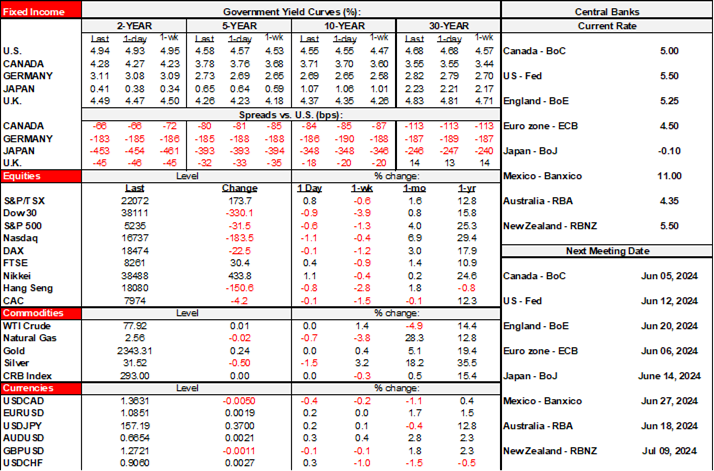

While most of the week’s action will unfold over the back half of the week, there are several noteworthy macro drivers to consider this morning. Elections in Mexico and India are having opposite market effects, oil prices are barely reacting to the OPEC+ meeting and US data lies ahead. Stocks are mostly higher across the major exchanges, sovereign bonds have a small richening bias, and the USD is little changed.

Peso Sinks on Mexican Election Outcome

Well, one of North America’s elections over the next 17 months is over and the electorate decided to grant a leftist administration broader support. The Mexican peso is frowning upon the outcome of the election and is about 2% weaker to the dollar so far this morning. Claudia Sheinbaum won the Presidency by an estimated 30 percentage points, and with her associates appear to have won a super majority in the lower house and senate. Expansionist fiscal policy, sector-specific risks and constitutional changes are at stake.

Indian Stocks Soar as Polling Indicates Strong Modi Victory

Indian markets were much more welcoming toward polls that are indicating Narendra Modi and his Bharatiya Janata Party alliance will win a majority when the official results of the weeks-long vote arrive tomorrow. Indian stocks advanced by over 3% and the rupee appreciated a touch. Stocks like it because Modi is perceived to be relatively friendlier toward markets than others and because of the magnitude of victory that may make it more possible to advance needed reforms. A risk concerns the need to keep Modi’s autocratic tendencies in check.

Oil Prices Shake Off OPEC+ Supply Surprise

Oil prices are taking the weekend OPEC+ virtual meeting in stride so far. WTI and Brent are little changed despite the potential addition of supply. The dysfunctional oligopoly extended production cuts as expected, but what was unexpected was the announcement that the cuts would be gradually phased out starting in October.

US Macro Updates on Tap

The US will update several readings today with the main one being ISM-manufacturing for May (10amET). It is expected to barely remain in contraction territory and also watch the prices paid measure.

US vehicle sales for May land later this afternoon as industry guidance points toward a modest rise toward 16 million SAAR based on sampling skewed toward the first 16 selling days of the month’s total of 26 selling days. That level has not been breached since May 2021. Also watch construction spending for April (10amET).

Canada updates the manufacturing PMI for May this morning (9:30amET) after signalling modest contraction of late.

As a reminder, please see the Global Week Ahead—Can Macklem Keep his Word? It should be in your inboxes or the general public version is here. There is no chart deck version this week.

Key topics:

- Will the BoC cut or hold? The cases for both & expectations

- ECB expected to begin easing—but should it?

- Will Canada’s jobs boom continue?

- Temps are swamping the Canadian summer job market

- US payrolls may be looking a tad Canadian

- Mexico’s election primer

- RBI expected to hold

- OPEC+ meeting probably won’t rock the boat

- Global macro

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.