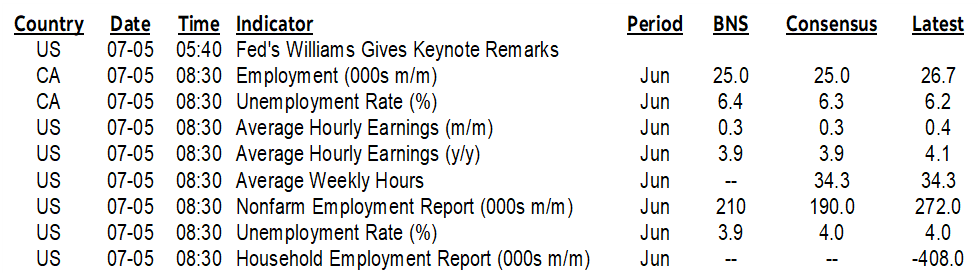

ON DECK FOR FRIDAY, JULY 5

KEY POINTS:

- Global markets await nonfarm payrolls

- Sterling, gilts, FTSE yawn at a priced UK election outcome…

- …that delivered a massive majority to Labour, Sunak resigns

- Most readings point to resilient US payrolls…

- ...that have exceeded consensus 5 out of six times this year!

- Canada’s boring jobs consensus

- Global Week Ahead

As a reminder, please see my Global Week Ahead—Human Error that was sent yesterday (here). Key topics:

- US core CPI may reaccelerate

- French election could impact risk appetite to start the week…

- …as French parties circle the wagons on Le Pen

- US bank earnings season commences

- Powell testimony will be stale on arrival

- CPI: China, India, Mexico, Chile, Colombia, Brazil

- RBNZ expected to remain hawkish

- BoK may sound more open to nearer term easing

- Bank Negara likely to remain on hold

- BCRP has a solid case to extend its pause

There were no materially surprising overnight macro developments which now shifts the emphasis to labour market readings out of North America to potentially influence risk appetite. These are the last jobs reports before the June FOMC and BoC decisions, but the inflation readings before those meetings are likely to matter more than anything we are likely to learn today.

The UK Election Outcome Was Priced Long Ago

The UK election came and went with little market fanfare. Folks over there are probably just glad it’s finally over. The results were broadly in line with the polls translated into seats. A strong majority was granted to Labour’s Keir Starmer as his party won 412 out of 650 seats in parliament. PM Sunak won his seat but then resigned as party leader after a series of truly awful British PMs who in my opinion weakened the country and its economy. Sterling barely wiggled, ditto for gilts and the FTSE100 is riding in tandem with the global tone. Suffice it to say that markets yawned at an outcome that was priced long ago.

Now it’s onto dual Canadian and US jobs reports.

Canadian Jobs Preview

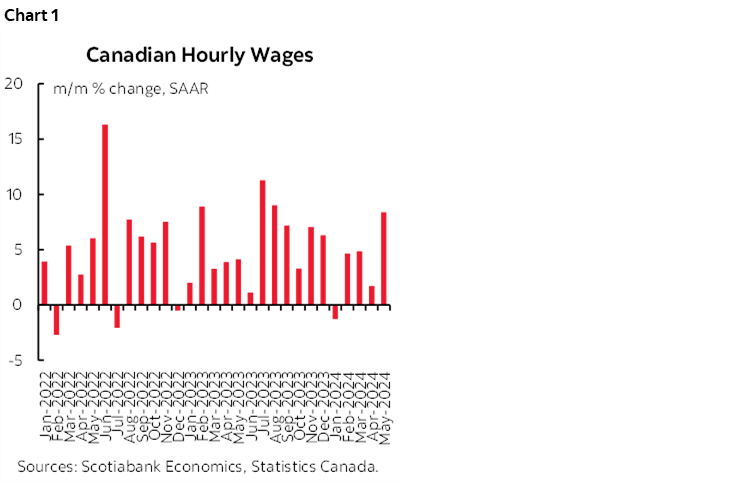

Canada updates job market readings for June at 8:30amET. Canadian population growth is expected to keep filling job vacancies that remain above pre-pandemic levels. The youth category drove much of the prior month’s employment gain and could require the 25+ population to step up this time. Wage growth may slip after hitting +8.4% m/m SAAR in May (chart 1). I expect the unemployment rate to keep rising as the labour force continues to grow more rapidly than employment thanks to strong population growth fed by higher immigration. Also watch hours worked for the full quarter as a Q2 GDP guide.

The range of consensus estimates is the tightest I’ve seen in a long time which is surprising. Everyone is in a 20–30k m/m range. Surprising because the 95% confidence interval on the change in employment is +/-57k which offers plenty of room for dispersion within the noise bands for this modest sample household survey.

Nonfarm Payrolls Preview

Could all the gloomy headlines about the US job market’s impending slow down finally get it right? I mean, seriously, I’m reading yet again this morning about how the pace of job growth is surely going to slow down this morning. Maybe it will, but consider the fact that out of the six payroll reports we’ve gotten since early January (hence including December’s), the pace of increase in US payrolls has exceeded consensus in five of them. It’s like endless warnings about GDP growth that is for sure going to crater….any moment now….and yet consensus has been stuck in a serial pattern of revising upward.

Advance labour market readings on balance point to resilient US payroll growth during June (8:30amET). The median call is for a gain of 190k. All estimates are within the noise bands around this estimate given the 90% confidence interval of +/-130k around changes in payrolls. Most of the estimates are within about 150k to 225k. Scotia’s estimate is 210k. The whisper number is 185k and hence any of you who submit estimates are within the noise bands as well.

Like Canada, but to a much weaker degree and for a shorter period of time, a pick-up in US population growth is helping to fill job vacancies that edged up a bit the prior month. Here is a rundown of those readings:

- Consumer confidence jobs plentiful increased in June.

- NFIB small business hiring plans were stable.

- NFIB jobs hard to fill fell

- ADP private payrolls were up by 150k, similar to the prior month

- JOLTS job openings increased in May, either signalling more hiring appetite or less success filling openings

- Challenger job cuts fell to 49k, the lowest since December

- initial weekly jobless claims were up only a touch between nonfarm reference periods

- ISM-services-employment fell

- ISM-manufacturing-employment fell

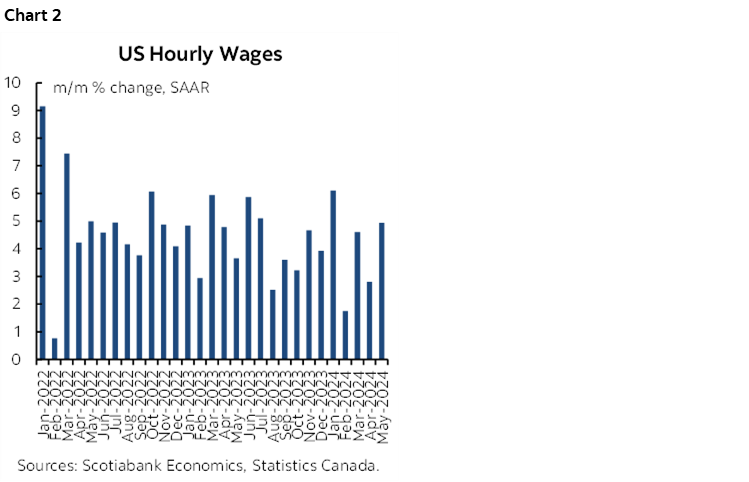

Also watch wage growth that has been on an oscillating pattern of highs and lows over the first five months of this year (chart 2). We’re due for a low if that pattern continues. Scotia’s estimate for the unemployment rate—derived from the household survey—is for it to tick down to 3.9% on the expectation that the 408k drop in the household survey’s measure of employment will rebound by more than the labour force’s 250k drop during May. Also watch hours worked as a Q2 GDP guide.

See this past week’s Global Week Ahead for more about expectations for US and Canadian job markets (here).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.