ON DECK FOR THURSDAY, JULY 4

KEY POINTS:

- UK markets await election outcome

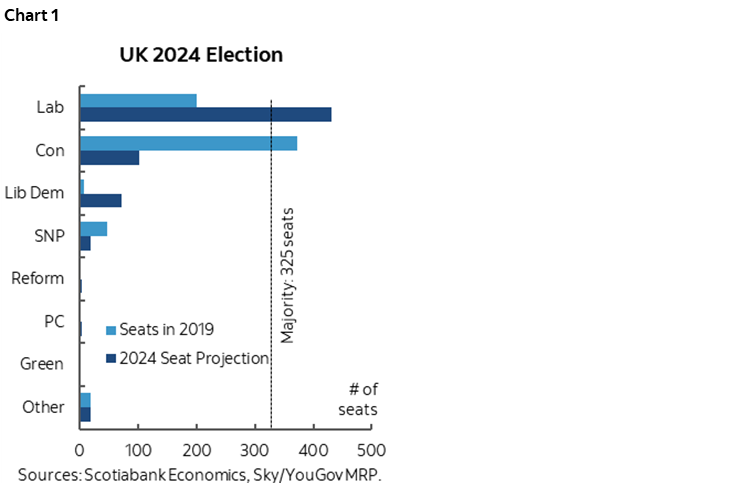

- Fresh poll points to Labour securing biggest majority since 1832…

- ...with the Tories getting crushed after years of mismanagement

- What Labour stands for in this election

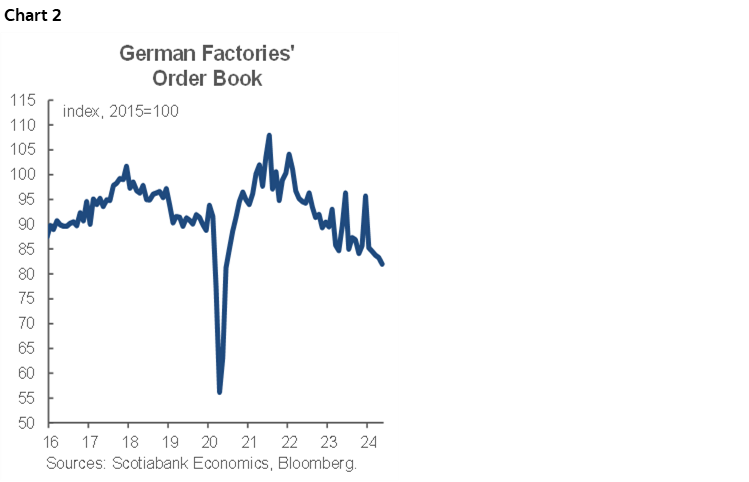

- German factory orders continue to fall below pre-pandemic levels

- US markets shut for Independence Day

The UK general election will be the main focal point as American markets are shut for Independence Day. Light data is on tap but probably won’t be consequential to markets. There is nothing consequential on tap in N.A.

UK voting ends tonight at 10pm British Summer Time (5pmET). A few early results will start trickling in by 11pmBST/6pmET. We may have an idea of the overall results by late tonight (eastern time) and hence into the early morning hours in London.

It would be a wild shocker if Labour didn’t win a large majority, let alone didn't win at all given their polling advantage. The key issues are whether Labour secures as large of a majority as the polls indicate and what shape the opposition may take.

The latest poll from YouGov (here) is indicating that Labour could win the largest majority of any government since 1832 (chart 1). PM Sunak may even lose his own seat. The projections point to a landslide outcome with Labour getting 431 seats, or 106 more than required to have a majority. The Conservatives may be crushed by getting just 102 seats, down massively from the last election. The Liberal Democrats would go from total obscurity to 72 seats. A stunning development would be if the Conservatives didn’t even secure status as the official opposition party.

The UK is bucking the pattern elsewhere as the center-left Labour party looks set to oust the Conservatives by a wide margin but in the context of extreme instability within the Conservatives and their poor performance over the years since the Brexit vote in 2016.

This piece in today’s Telegraph summarizes Labour’s platform.

German Factories Are Struggling

German factory orders disappointed again. They fell 1.6% m/m in May and the prior month was revised lower (-0.6% m/m instead of -0.2%). Orders have been trending lower since 2021 and are materially lower than pre-pandemic levels. With the exception of the pandemic’s initial effects, orders are at their lowest since 2012 (chart 2).

Not Much Else

Markets shook off a small miss on Swiss CPI. It was flat in June (+0.1% consensus). Pricing for the next SNB decision on September 26th was little changed.

Minutes to the ECB’s June meeting arrive at 7:30amET but are unlikely to offer materially different guidance relative to the views expressed by President Lagarde et al.

Canada updates the little watched S&P Global purchasing managers index this morning (9:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.