ON DECK FOR WEDNESDAY, JULY 31

KEY POINTS:

- Oil and shipping costs tag-team to provide caution on inflation risk

- Oil prices surge after Israel kills Hamas leader on foreign soil in Iran

- Yen appreciates to strongest since March, JGBs bear flatten…

- …after BoJ surprises with 15bps hike and slashing bond purchases

- Eurozone core inflation was relatively warm again, lending caution to ECB easing

- Softer—not soft—Aussie core inflation wipes out RBA hike pricing

- Chinese PMIs weakened again

- US ADP payrolls on tap as a meaningless nonfarm market teaser

- US employment costs expected to keep rapidly rising

- Canada’s economy may have ended Q2 on a softer note

- FOMC to signal greater confidence, but remain cautious

- BanRep expected to cut when the FOMC statement lands

- BCB expected to stay on hold

A brewing oil shock on Middle East tensions risks combined with rising shipping costs and stubborn data risks thwarting easing plans by several global central banks. The BoJ may be an exception after it tightened monetary policy overnight as such catalysts could drive further imported inflation. Especially vulnerable are the easing plans of central banks in oil- and trade-dependent economies that could face more intense inflation pass-through. You and I can probably think of a few; gimme a ‘C’, ‘A’, ‘N’…. Canada 5s are dear imo.

Rising Risk of Middle East War Drives Higher Oil Prices

Oil prices are up by about $2 because of escalating tensions in the Middle East. Israel killed the Hamas political leader in an air strike in Iran overnight. This follows hours after Israel’s strike on Beirut that killed a senior Hamas leader. Iran has pledged vengeance. The original instigation to the latest escalation was the cruel rocket attack by Hamas on a soccer field in Israel that killed a dozen children.

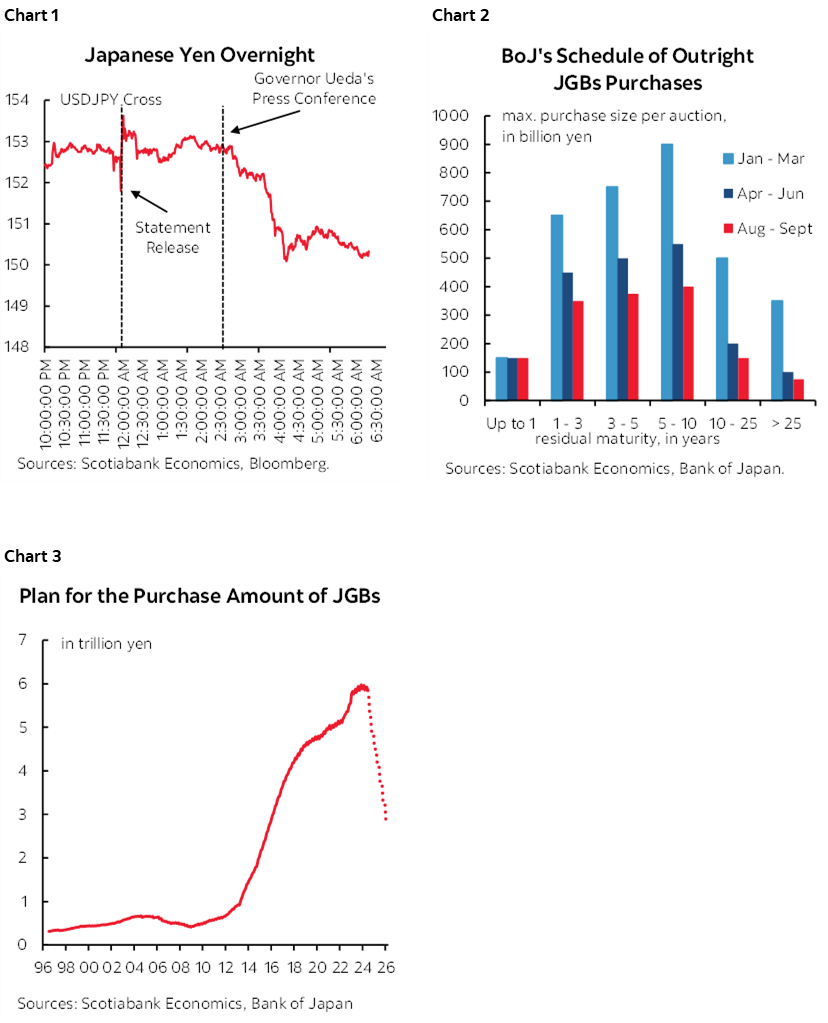

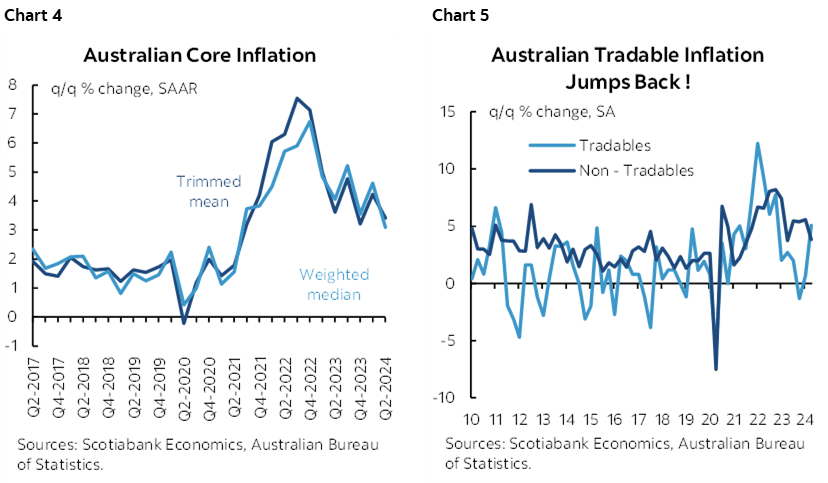

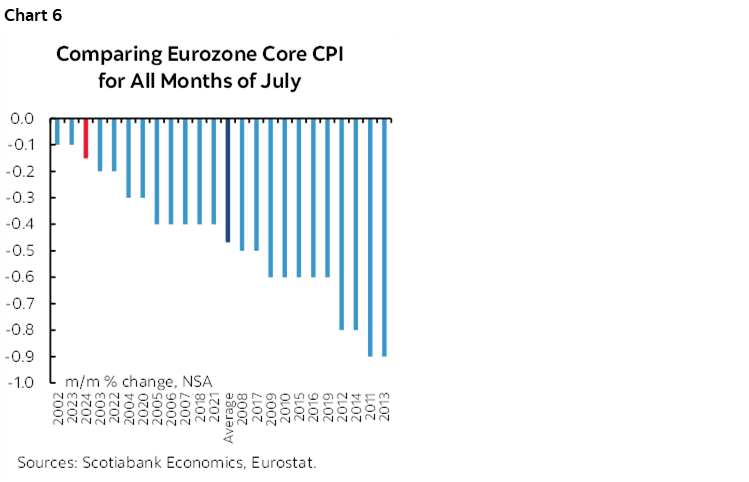

BoJ Hikes, Slashes Bond Purchases

The Bank of Japan hiked its policy rate by 15bps to 0.25% and announced a plan to gradually taper its monthly bond purchases of ¥5.7 trillion by about ¥400 billion per quarter eventually going down to about ¥3 trillion by the Spring of 2026. Forward guidance was hawkish by stating: “…if the outlook for economic activity and prices presented in the July Outlook Report will be realized, the Bank will accordingly continue it raise the policy interest rate and adjust the degree of monetary accommodation.”

Markets responded by pushing the yen to 150 to the dollar (chart 1), making it the class leader this morning. Charts 2 and 3 show the BoJ’s projected plans for QE tapering. The JGBs curve sold off in bear flattener fashion led by about an 8bps rise in the two-year yield to 0.44%. That yield is up by almost half a percentage point this year while the US two-year yield is only about 16bps higher on net so far since January following the rally that build momentum since June. This narrowing differential is helping yen and lessening carry influences out of yen into benchmarks elsewhere if it were not for geopolitical turmoil.

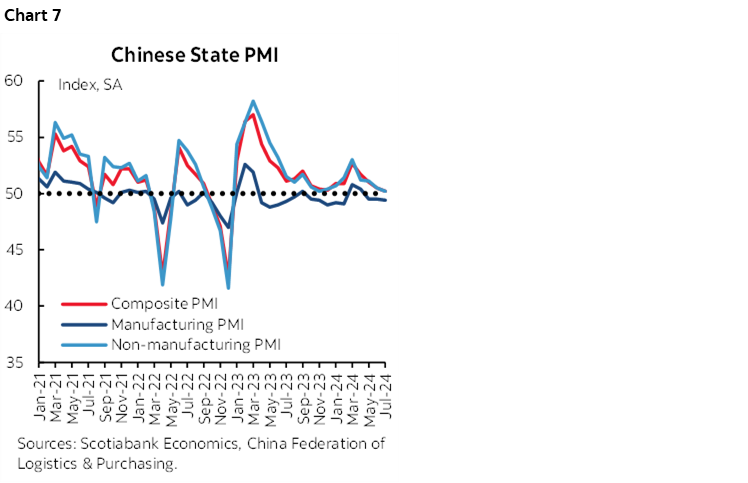

Australian Core CPI Wipes Out RBA Hike Pricing

Australian CPI wiped out the slim market pricing for an RBA hike on August 6th. Both core measures landed softer than expected. Trimmed mean CPI and weighted median CPI were both up by 0.8% q/q nonannualized (1% consensus). Chart 4. Those are still above the upper limit of the RBA’s 2–3% headline inflation target but demonstrate progress that provides time for further assessment by the central bank. Chart 5 shows that non-tradeables inflation—more driven by domestic factors—ebbed a touch while tradeables inflation surged.

Eurozone Core Inflation Was Another Hot One

Eurozone core CPI was down -0.15% m/m seasonally unadjusted. Prices normally fall in July over June and so what matters is that compared to like months of July in history this one was the third strongest on record (chart 6). Core inflation continues to be too warm. The result held the y/y core CPI rate at 2.9% against consensus expectations for a small drift lower. The y/y rate is influenced by base effects whereas the persistent pattern of stronger than usual m/m readings is an ongoing warning sign to the ECB.

China’s Troubled Economy

Chinese PMIs weakened a touch further on the heels of more concerns being expressed about the economy by the Chinese leadership (chart 7). The state’s composite PMI slipped three tenths to 50.2 mostly due to a three-tenths decline in the non-manufacturing PMI.

North American Market Events

Here is what’s on tap into the N.A. session:

US ADP payrolls are almost always useless for forecasting nonfarm payrolls, but markets often think differently at least for a little while in the aftermath (8:15amET).

US employment costs are expected to continue to grow at a rapid pace (8:30amET).

Canada’s economy will be the focus in May and June estimates (8:30amET). May was previously guided to be up 0.1% m/m SA but watch for revisions and details. June will be the initial estimate that rounds out Q2 tracking and sets the hand-off effect in the math for Q3 GDP momentum.

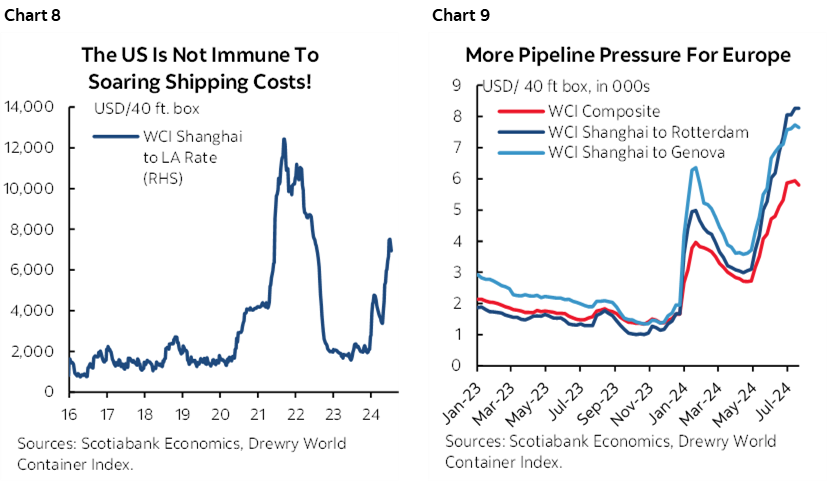

Then it’s over to the FOMC that won’t change any policy but watch whether more confidence is offered toward a cut in September. Statement at 2pmET, press conference at 2:30pmET, no forecasts this time. Tread carefully, Mr. Powell, as inflation risk is brewing through oil prices and shipping costs due to tensions in the Red Sea shipping lanes (chart 8, 9). I still think that inflation is principally driven by domestic factors in the US and that the imbalances are turning toward being more favourable to the inflation outlook which will dominate the presser. And yet the need for further data and global developments may keep Powell sounding noncommittal to September. September is fully priced, so the market risk is that Powell says they don’t have enough confidence and will need to see more of it before deciding.

BanRep is expected to cut by another 50bps at the same time as the FOMC statement lands which might be a tad nervy (2pmET).

Brazil’s central bank is widely expected to hold in tomorrow’s after-market (5:30pmET).

Tech earnings could play a major role once again as Meta Platforms releases Q2 EPS (estimate US$4.75) in today’s after-market.

For more on expectations for the FOMC and Canadian GDP please see my Global Week Ahead here.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.