ON DECK FOR THURSDAY, JANUARY 4

KEY POINTS:

- Markets ignore soft Eurozone inflation, focus on hawkish FOMC minutes

- French, German inflation readings land weaker than expected

- FOMC Minutes indirectly leaned against nearer-term easing...

- ...and no, nothing material was said about QT

- BoC repo intervention is a temporary fix to a problem they are causing

- US job market readings tease markets ahead of payrolls...

- ...and continue to indicate a very resilient US job market

- Americans bought the most vehicles in 2023 since 2019…

- …as the need to replaced clunkers offsets financing pressures

- Canadian auto sales are ripping, Toronto home sales up...

- ...as Canadians continue to make big purchases

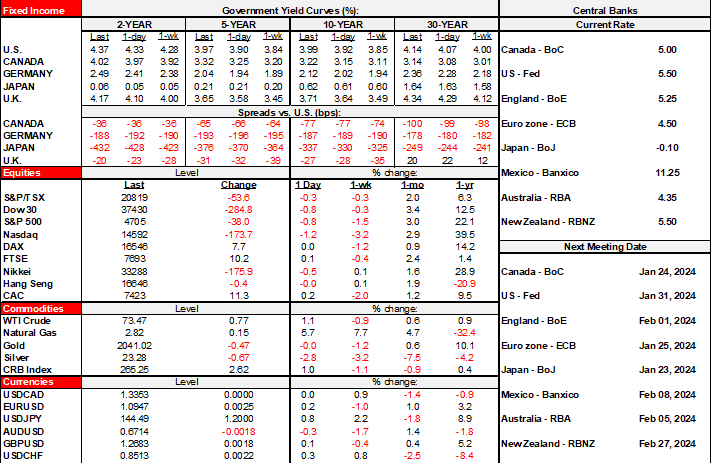

Soft Eurozone inflation readings are being shaken off across the global rates complex that continues to push yields mildly higher this morning. Bonds may be reacting more to yesterday’s FOMC minutes that were hawkish relative to market pricing for the commencement of rate cuts by offering no such hints that the Committee’s collective head is aligned with markets which matters since markets have gotten the Fed wrong on a pretty routine basis throughout the pandemic. Markets are trimming pricing for the March and May 1st fed funds futures contracts. A fuller recap of the minutes is offered below along with comments on the BoC’s repo market intervention and what it says about its QT plans. Other data risk today will be lightly focused upon US job market readings.

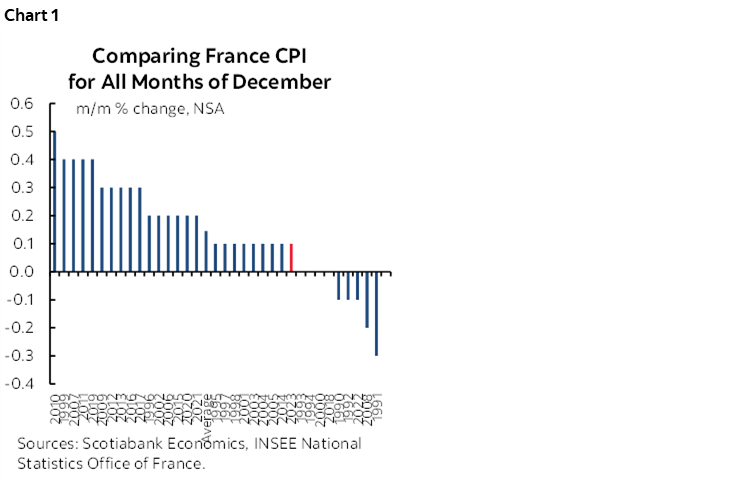

French CPI landed weaker than expected and as such followed in Spain’s footsteps. French CPI was up by just 0.1% m/m NSA in December (0.3% consensus) and it was only due to base effects that the year-over-year rate edged up to 4.1% from 3.9%. Given it is seasonally unadjusted data, we need to compare this December to like months in history to show that it was a relatively light month for price pressures (chart 1).

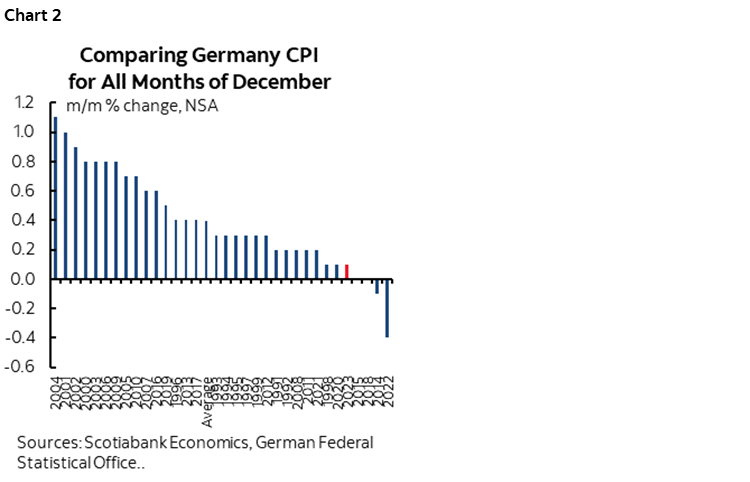

The same can be said about the German figures (chart 2). The national tally (0.1% m/m, consensus 0.2% m/m) and on an EU-harmonized basis 0.2% m/m (0.3% consensus) confirmed what the readings across the individual German states had already indicated when they landed between -0.1% m/m and +0.1%. Germany posted among the very weakest price increases compared to like months of December in history which we do because it’s seasonally unadjusted. The only reason the year-over-year rate moved up from 2.3% to 3.8% was because the index level fell in December of 2022 and offered a weaker base effect for the y/y rate in December 2023.

So why are markets ignoring soft European inflation readings? One possibility is always going to be that perhaps markets just had fundamentally different expectations than the economist consensus and markets were less surprised. Another possibility is that markets had already seen the Spanish numbers last week and were primed for weak French and German tallies, although markets didn’t really respond to last week’s Spanish readings. Another possibility is that it’s not about Eurozone inflation and more about whether the Fed is going to be leading central banks toward easing which positions yesterday’s relatively hawkish sounding FOMC minutes as the most important factor (see below).

The US is updating a round of job market teasers that may spark some market volatility but that are largely just about passing the time before we get payrolls and wages and perhaps revisions to historical unemployment rates tomorrow.

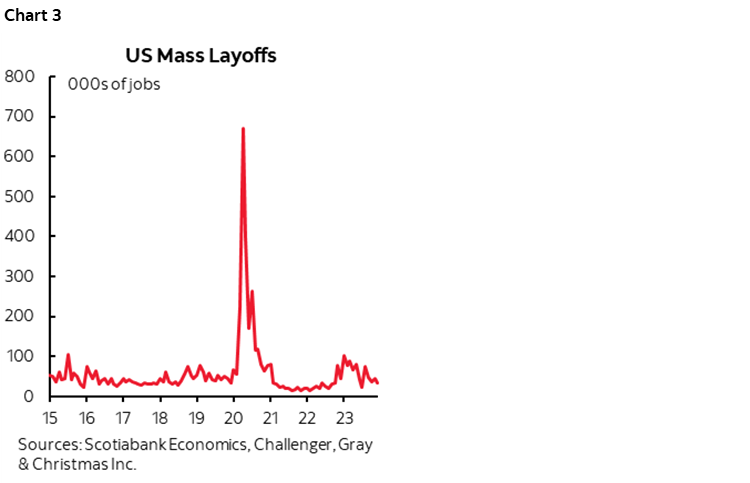

Challenger job layoffs remain low at about 35k in December which is down from 45.5k in November (chart 3). That’s a level of layoffs that is very much indicative of ongoing strength in the US job market.

US ADP payrolls were up by 164k in December (130k consensus). There is nothing statistically unusual about this gain relative to consensus expectations for tomorrow’s private nonfarm payrolls to be up by 130k (total up by 171k) in light of ADP’s weak performance as a guide to nonfarm payrolls. In other words, there is no reason to react to ADP and no reason to alter expectations for nonfarm because of it.

US initial jobless claims fell back to 202k last week which is quite low. I wouldn’t get too excited by this, however, since there will always be question marks around whether the SA factors adequately compensated for the holiday season and because California submitted an estimate instead of hard data which accounted for much of the w/w improvement from 220k prior.

Canadian auto sales are soaring. Desrosiers Automotive Consultants estimated another m/m SAAR gain in auto sales in December (here). 2023 saw the highest sales volumes since 1997 and they were up by 11.8% y/y. The age of vehicles combined with pent-up demand and a resilient macro backdrop characterized by very strong job growth, very strong wage gains, soaring immigration, and overhyped mortgage reset concerns explain this.

In addition, Toronto’s existing home sales soared last month (here including rolling graphics, and here for the detailed data). Sales were up by 21% m/m SA and 11.5% y/y with seasonally adjusted prices up by 2.5% m/m SA. Despite all of the gloom across consensus, Canadians are still making large purchases.

Canada also updates S&P PMIs for December but there is no consensus estimate for them and they don't have a material market following (9:30amET).

Also note that US vehicle sales surprised higher late yesterday. 15.83 million units were sold last month, which is up by half a million from the prior month for the highest level since April. On a weighted contribution basis, this gain would add about ½% m/m to December retail sales on its own which is a good running head start. Despite the pessimism, Americans bought the greatest number of new vehicles in 2023 since 2019. While financing tightened, the average age of vehicles on American roads is over 12 years. Being an average means that a lot of them are considerably older and facing replacement demand plus pent-up demand from earlier in the pandemic.

FOMC MINUTES—NO HINT AT NEARER-TERM EASING, SAID NOTHING MATERIAL ABOUT QT

The Minutes to the December 12th–13th FOMC meeting came and went with little to no fanfare. My take on them is that whether through omission or because of thinly veiled guidance, they leaned against any notion in the markets that the Committee is moving toward easing as soon as markets are pricing. I also thought that headlines on what the minutes said about QT were extraordinarily exaggerated.

The minutes contained no direct discussion on easing parameters and the indirect message is that they are not even broaching the topic of possibly easing as soon as markets are pricing by the March or May 1st decisions. Chair Powell was asked during his December press conference when it may become appropriate to begin easing and responded by saying “That was a discussion point in our meeting today.” Since the minutes are an account of the discussion there was the reasonable expectation that the minutes would expand upon the topic. They did not do so in any meaningful fashion.

“…almost all participants indicate that, reflecting the improvements in their inflation outlooks, their baseline projections implied that a lower target range for the federal funds rate would be appropriate by the end of 2024.” We knew this from every dot plot since the one in June 2022 and so there was nothing new here.

“Participants also noted, however, that their outlooks were associated with an unusually elevated degree of uncertainty and that it was possible that the economy could evolve in a manner that would make further increases in the target range appropriate.”

“Several also observed that circumstances might warrant keeping the target range at its current value for longer than they currently anticipated.”

“Participants generally stressed the importance of maintaining a careful and data-dependent approach to making monetary policy decisions and reaffirmed that it would be appropriate for policy to remain at a restrictive stance for some time until inflation was clearly moving down sustainably toward the Committee’s objective.”

The minutes also reversed the Committee’s prior take on tightening financial conditions in the November 1st statement by now acknowledging that conditions had eased and complicated their plans once again.

"Many participants remarked that an easing in financial conditions beyond what is appropriate could make it more difficult for the Committee to reach its inflation goal. Participants also noted other sources of upside risks to inflation, including possible effects on global energy and food prices of geopolitical developments, a potential rebound in core goods prices following the period of supply chain improvements, or the effects of nearshoring and onshoring activities on labor demand and inflation."

What the minutes said about QT plans was ridiculously overhyped by some commentators. No, the minutes did not say they were approaching the end of QT. The minutes merely stated the blindingly obvious point that it would be prudent to be discussing technical factors that would guide QT tapering well before reaching a decision on when to taper. Here is the passage:

“Several participants remarked that the Committee’s balance sheet plans indicated that it would slow and then stop the decline in the size of the balance sheet when reserve balances are somewhat above the level judged consistent with ample reserves. These participants suggested that it would be appropriate for the Committee to begin to discuss the technical factors that would guide a decision to slow the pace of runoff well before such a decision was reached in order to provide appropriate advance notice to the public.”

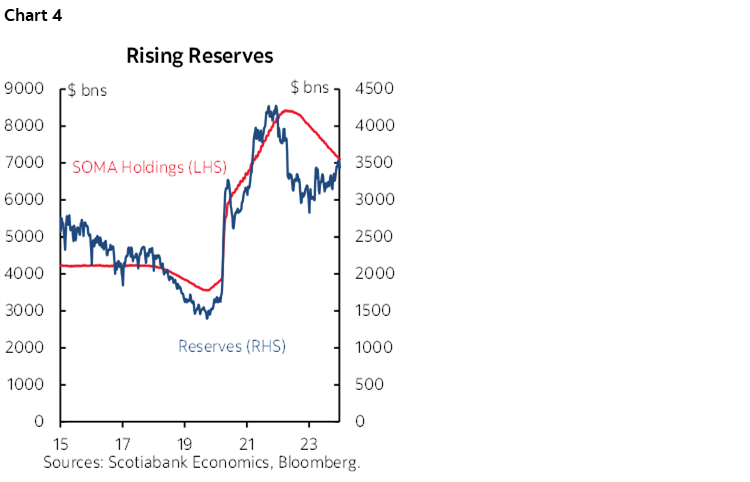

At US$3.45 trillion, US bank reserves have been rising for some time now of late and remain well above most estimates of the Fed’s target for ample reserves that it wants to remain above in order to avoid funding market problems (chart 4). That increase is despite continued QT as other funding market developments and Fed tools have been offsetting. This stands in direct contrast to what’s happening in Canada which is the next focus.

BANK OF CANADA FUNDING PRESSURES AND QT

Funding market pressures are catching the eyes of central banks in both the US and Canada. While there are some common drivers in both countries, the Canadian context involves longer-lived and more idiosyncratic drivers of funding pressures.

The BoC expressly stated upon announcing yesterday morning’s repo market operation that the intervention had “the purpose of alleviating funding pressures” which would be the customary motivation for such action.

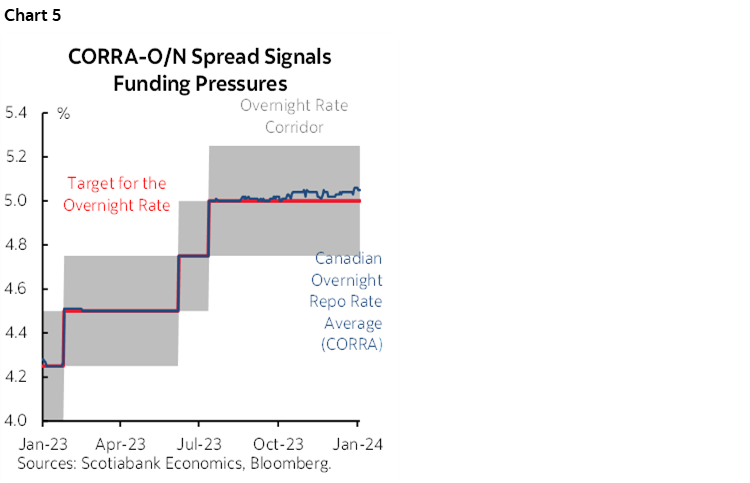

I think their approach to rely upon short-term open market operations is at best an imperfect and temporary solution given the long-lived root causes. For many months now, the market has been sending the BoC a signal about reserve scarcity in the context of their aggressive QT plans. The Canadian Overnight Repo Rate Average (CORRA) has been trading above the overnight rate for over four months now (chart 5). There may have been added year-end transition pressures, but this is not a new phenomenon.

The last time we saw CORRA depart from the o/n rate was in the opposite direction from late 2020 through 2021 and it was among the reasons the BoC shut down their QE program earlier than other CBs. The market was sending them a signal that they were doing too much bond buying and reserve injection.

Today is offering the reverse logic. They may be withdrawing liquidity and funding support at an overly rapid pace. While it’s by no means a crisis, it risks becoming a more acute challenge should the central bank continue to foist bonds back into the market through 100% roll-off plans for as long as they have previously stated a desire to continue doing so. I think they'll be increasingly pressured to reduce QT flows earlier than planned.

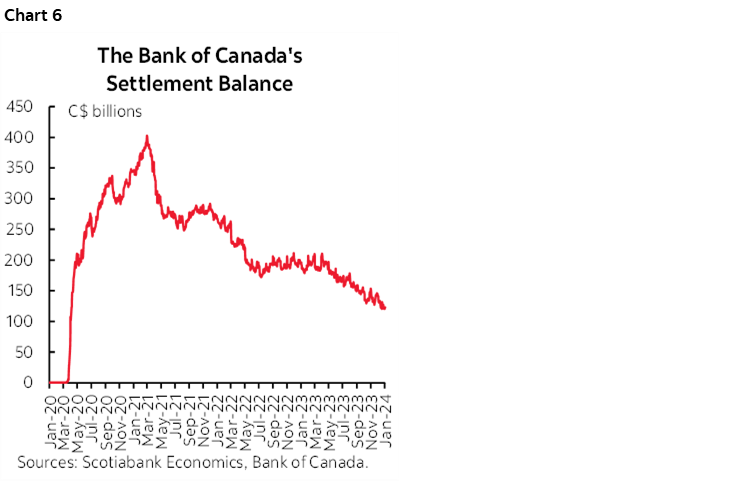

Reserves have now fallen to about C$123B from a peak of about $400B (chart 6). That’s a massive unwind of the extent to which the BoC had driven reserves higher in the pandemic when it bought up bonds by the bucketful.

The BoC's announced target was to get reserves down to between $20–60 billion or 1–2% of NGDP. That compares to the Feds' ballpark targets of reserves to GDP at 10–12%. The BoC is targeting a much leaner reserves framework than the Fed and leaving little margin for error in funding markets.

They said they thought they would achieve such targets for reserves toward the end of 2024 or early 2025. Ergo, they would be shutting down QT by around that time and probably guiding markets in advance.

When the BoC announced those targets last March, however, they said it was a rough estimate that would be informed by market developments. That would include evidence on funding pressures.

I wrote at the time—and again in December—that I thought the BoC may have been too aggressive with such targets by going on auto-pilot with 100% roll-off of maturing bonds. You could argue that Canada's banking system can get away with leaner reserves than the perennially accident-prone US banking system. By contrast, you could also argue that Canada should have higher reserves because when market risk appetite turns and volatility escalates, Canada tends to get hurt more which may require higher levels of liquidity in the banking system. If the economy rolls over this year and market frailties are exposed, then it would be an inopportune moment during which to be continuing to pressure funding markets and risk courting an accident.

Against various hypothetical arguments is the fall-back argument of letting markets decide. I think markets are saying to the BoC that they are trying to push reserve scarcity to being too tight and by corollary the liquidity withdrawals through roll-off plans are too aggressive.

So, what I'm still saying on balance is that the longer funding pressures persist, the greater my preference for the BoC to announce a longer-lived and more certain solution by backing off QT and reserve plans earlier than previously guided as their best guess at that time. I don't like the alternative of keeping markets guessing toward serial applications of open market funding tools. It would probably be preferable for the BoC to begin signalling that it is open to gradually tapering QT flows. They could invoke the same approach—in reverse—that they used upon shutting down QE by tapering the flows at each MPR meeting and taking one year to extricate themselves from the bond buying business.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.