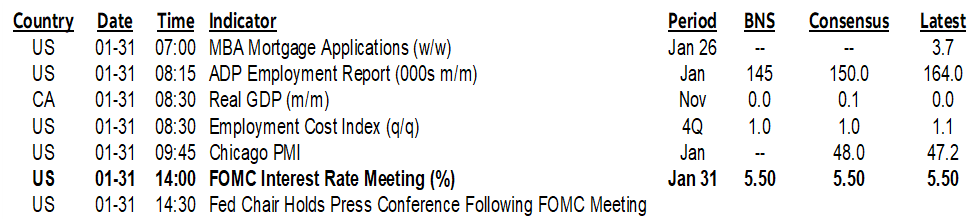

ON DECK FOR WEDNESDAY, JANUARY 31

KEY POINTS:

- Markets await the Fed

- Key FOMC expectations

- US ECI probably remains hot

- US ADP to tease markets pre-nonfarm

- Did Canada’s economy end the year on a brighter note?

- CPI adds to RBA rate cut pricing

- Mixed Eurozone inflation readings

- China’s state PMIs post miniscule improvements

- BanRep: -25 or -50?

- BCCh likely to deliver 100bps cut

- Brazil’s central bank to cut 50bps, guide another one coming

Markets got out the noise rattlers after several overnight developments that are highlighted below, but the real focus will be upon the Fed this afternoon. Canadian markets will track GDP before being potentially buffeted by the Fed a few hours later. So far, US Ts, gilts and EGBs are benefitting from a gentle bid, the USD and slightly firmer, and equities are generally flat to a touch lower. US earnings from Microsoft, Alphabet and AMD were solid but didn’t meet what was priced as bigger tech names await in tomorrow’s after-market.

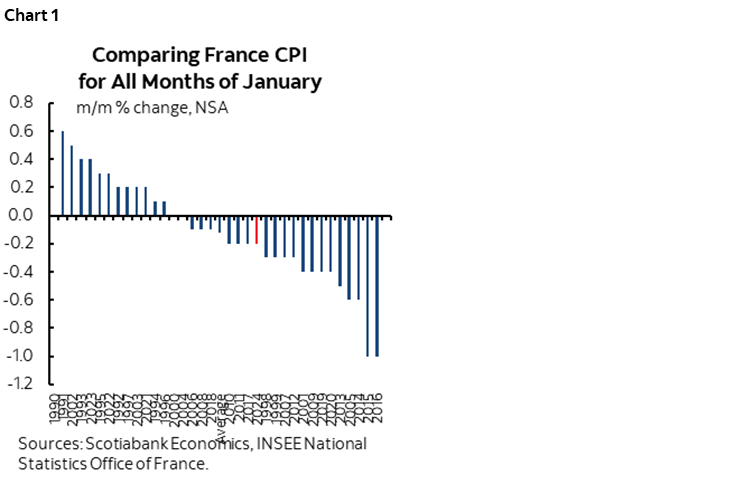

Eurozone CPI tracking was further informed by softer than expected French figures but firmer than expected German readings in the wake of Spain’s hotter than expected core CPI print yesterday. French CPI fell -0.2% m/m (0% consensus) in January which was a little softer than a typical January (chart 1). Individual German states posted readings between 0% m/m and +0.4% which suggests some upside risk to the national estimate that arrives at 8amET. EGBs rallied after the French numbers that followed weaker than expected German retail sales volumes in December (-1.6% m/m SA, +0.6% consensus) but reversed that following the figures from German states.

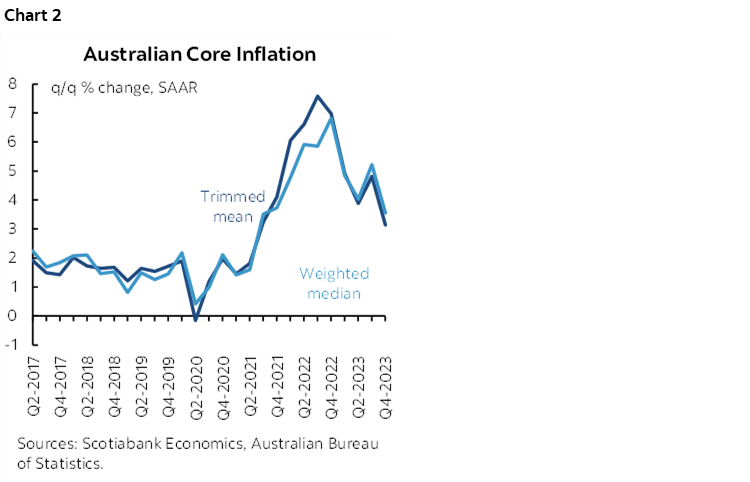

The A$ depreciated and the Aussie rates curve rallied by double digits after Q4 inflation came in weaker than expected. CPI was up 0.6% q/q SA nonannualized (0.8% consensus) which was half of the prior quarter’s rise. Trimmed mean (0.8% q/q SA, 0.9% consensus) and weighted median (0.9% on consensus) were also softer than the prior pattern (chart 2). The RBA meets next week as markets added about 7bps to May cut pricing that stands at about 18bps now, and added about 5bps to June cut pricing that is almost at a full quarter point.

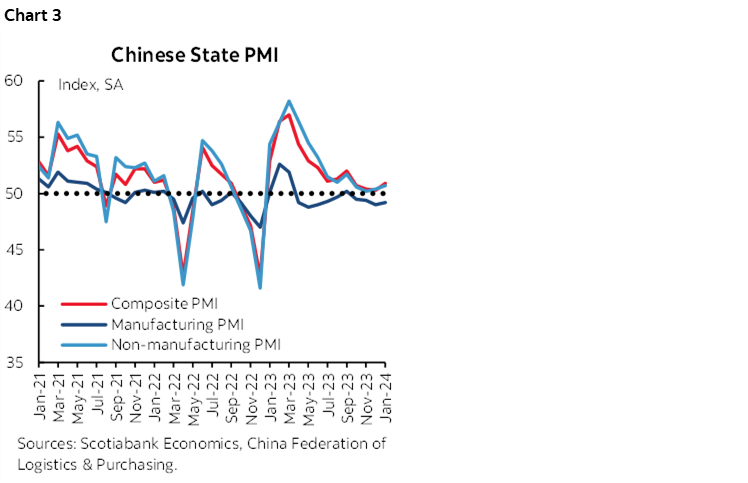

China’s state PMIs posted a very slight improvement but remained soft (chart 3). The composite PMI rose 0.6 points to 50.9 in January as tiny improvements were registered in non-manufacturing and manufacturing PMIs.

Japanese macro readings further suggested that the BoJ should tread carefully on ending negative rates anytime soon. Retail sales fell by 2.9% m/m in December (consensus +0.2%) and industrial output disappointed expectations (+1.8% m/m, 2.5% consensus, -0.9% prior).

On tap into the N.A. session will be the following developments.

Canadian GDP for November with details and the preliminary estimate for December sans details are likely to show little to no growth in November but perhaps stronger growth in December based on limited activity readings (8:30amET). Statcan had guided November was up 0.1% m/m before fresher data arrived. Consensus estimates are between 0% (mine and others) and +0.2%. I’m a bit surprised no one went with a dip. Preliminary guidance for December could be positive based upon readings available to date. See the Global Week Ahead for more about Canada’s economy.

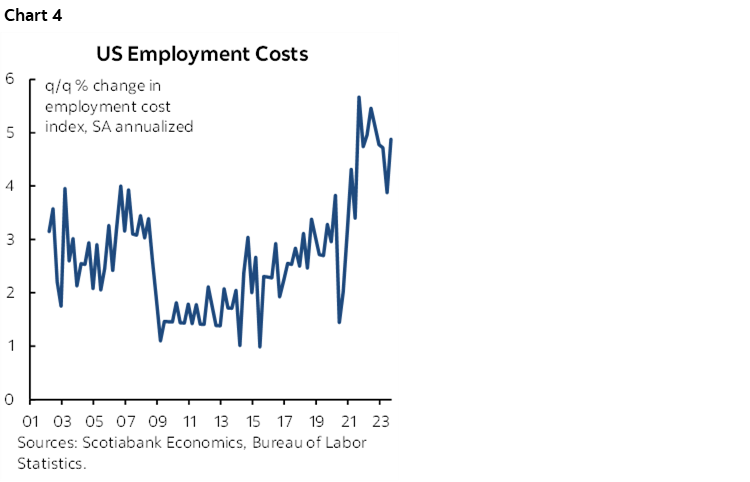

US labour market readings will include ADP private payrolls (8:15amET) that aren’t worth much by way of providing insights into expectations for Friday’s nonfarm payrolls, plus the key Employment Cost Index that is expected to be another hot one at 1%+ q/q SA nonannualized (8:30amET). Chart 4 shows the accelerating trend that began before the pandemic. That will help to further inform expectations for Q4 unit labour costs when we get that and productivity on Thursday.

BanRep is expected to cut 50bps (1pmET).

Then it's the Fed's turn. The statement arrives at 2pmET sans SEP and Chair Powell’s press conference is at 2:30pmET. Here is a summary of key FOMC expectations and please see the Global Week Ahead for more:

- The FOMC is expected to hold at a Fed funds upper limit of 5.5%.

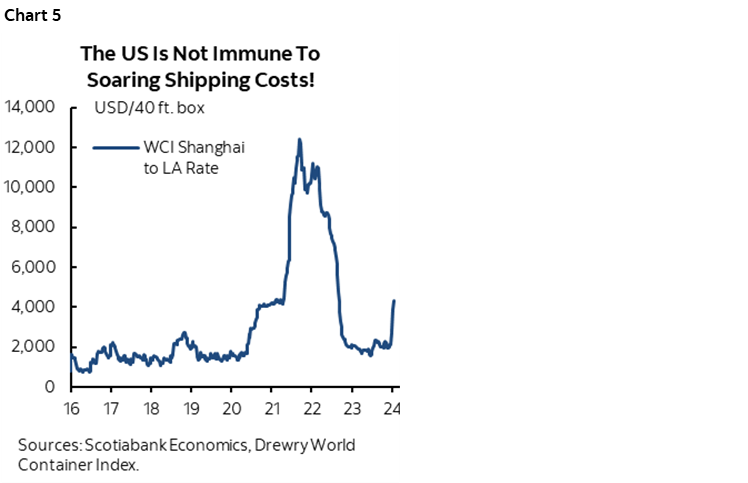

- Watch for whether they eliminate or tweak the statement reference to “any” further rate hike(s). If they blow it off, then this could ignite March cut pricing at least until Powell's presser expands upon the decision. I doubt they will, given developments since the last statement that have included stronger than expected growth, strong payrolls and wages, rising shipping costs including from China to the US (chart 5), and the mostly positive tone of other data. Core PCE has cooled on a trend basis, but upside risks remain material and probably higher than in December. In December's presser, Powell said that Committee participants thought they were probably at a peak but did not want remove the option from the table. If they didn't want to then, Powell would have to have a very good explanation for why they would suddenly wish to do so now.

- as for setting up a March cut in the statement or presser, I highly doubt it. Upon removing the ‘any’ reference to additional policy firming they would have to replace it with something more open, but in that scenario, I would expect Powell to indicate caution against moving too soon during the presser. The last dot plot showed 75bps of cuts this year and so starting now would mean two more 25bps cuts over the other six meetings which would be a pace that wouldn’t signal much conviction they should be easing. Several voting FOMC members have cautioned against easing prematurely.

- They might strengthen the opening sentence’s reference to strong US growth; technically they could still say the economy is slowing from the Q3 pace, but 3½% isn’t slow and so they might want to revamp the sentence.

- Forward rate guidance is likely to continue to refer to the December dot plot with the next one due in March.

- No QT changes are expected.

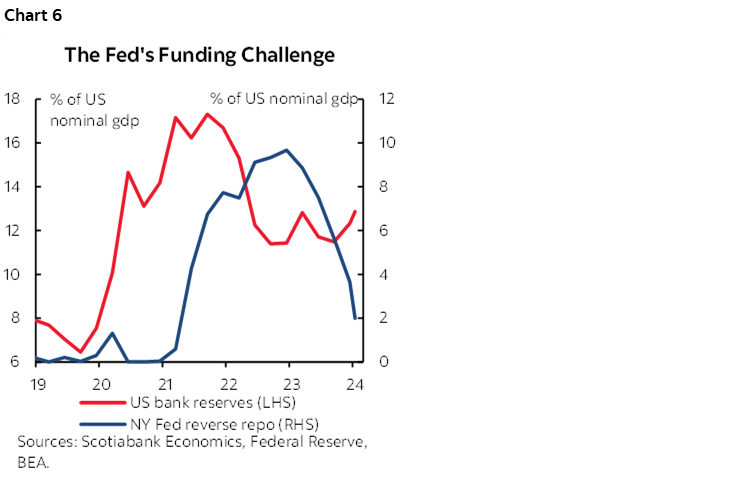

- watch the presser for any potential QT set-up. Reserves and repo facility balances are expected to further tighten funding market pressures into Spring, likely requiring the Fed to reduce QT run-off of maturing bonds (chart 6). I think Powell’s safest route for now is to tease. He'll likely say they discussed it further, watch the minutes in 3 weeks time, say no decisions were made at this meeting and that they plan on discussing it further in March at which point most folks expect an announcement to be made and implemented shortly thereafter. The QT taper timeline is uncertain but they will probably opt for a meeting by meeting approach that lowers the roll-off amounts to zero over multiple meetings into 2025.

Another pair of LatAm central banks will then follow the Fed. Chile’s central bank is expected to deliver a -100bps whopper (4pmET) while Brazil’s central bank sticks to its well telegraphed plan to cut another 50bps and set up another cut of the same size in March (4:30pm).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.