ON DECK FOR WEDNESDAY, JANUARY 3

KEY POINTS:

- Why are bonds off to a poor start to 2024?

- One way that the FOMC minutes could be key

- US JOLTS to tease ahead of nonfarm as job markets continue to rebalance

- US ISM-mfrg might get a helping hand from the UAW

- US vehicle sales probably held steady

After yesterday’s fixed income sell-off and sharp gain in the USD we now enter a period of elevated calendar-based risk over the rest of the week. So far this morning the USD continues to march higher, although at a slower pace, while sovereign bonds are putting in a more mixed performance. US Ts, gilts and Italian yields are moving a little higher while bunds and French yields are stable.

Among the initial catalyst for yesterday’s market moves might have been higher oil prices on tensions in the Persian Gulf and effects on inflation break-evens, but oil ended lower and is largely treading water this morning. Heavy corporate issuance rippled through markets as an added influence. Calendar effects might be contributing as the rally in US Ts over December that extended November’s moves might have driven a swing in positioning around month-end into a new calendar year. Markets might also be rethinking how aggressively they have priced rate cuts. There wasn’t any significant data, but some of the sell-off could be positioning ahead of the rest of the week’s developments. The sell-off caught fund managers off guard as they return from holidays and reassess positioning.

Overnight developments should be light, barring off-calendar surprises. The US will then update a couple of significant releases tomorrow ahead of the publication of minutes to the December 12th – 13th FOMC meeting.

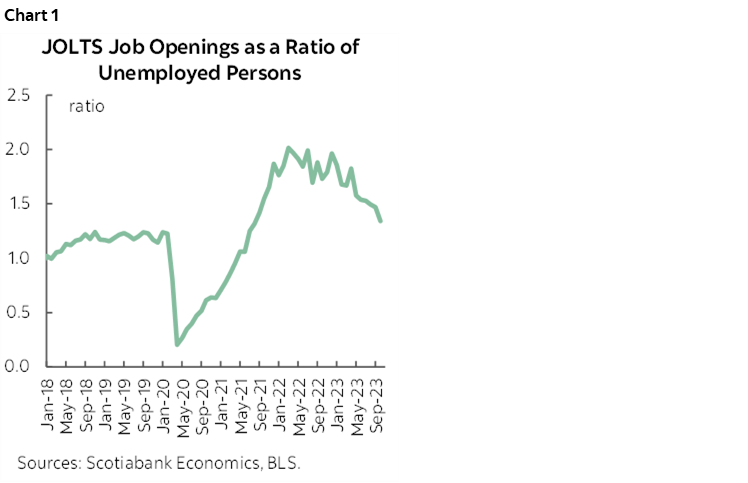

US JOLTS Job Openings

JOLTS job openings have been declining for the past two months but November’s data could face greater than usual positive seasonal hiring effects (10amET). It’s lagging data and what movements in vacancies say about hiring is somewhat ambiguous, but the release can impact markets as we wait for Friday’s payrolls. One measure that is widely followed including by the Fed is the ratio of job openings scaled to unemployed folks. That measure has been steadily declining and is only modestly above pre-pandemic levels (chart 1). This is one of the measures signalling the rebalancing of the labour market.

US ISM-manufacturing

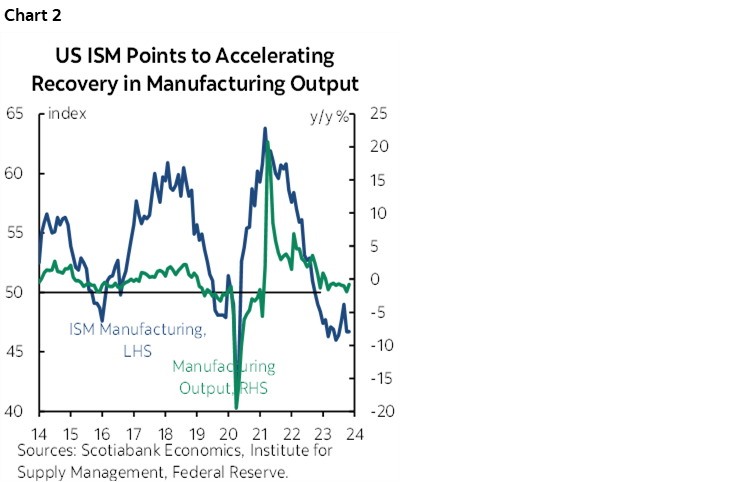

ISM-manufacturing for December (10amET) is forecast to rise a touch, but if consensus is correct, then it could be mostly fed by the transportation sector as the end of the UAW strike continues to restore order. Offsetting this in terms of breadth is the fact that most regional manufacturing surveys deteriorated during December. ISM lands at the same time as JOLTS and so this could make it difficult to separate the effects. The ISM gauge’s volatility exaggerates the changes in actual manufacturing output over time (chart 2).

FOMC Minutes

FOMC minutes (2pmET) will offer further colour around the dialogue on rate cuts that occurred during this meeting (recap here). Why? Because during his December press conference, Chair Powell responded to a question about when it may become appropriate to begin easing by saying “That was a discussion point in our meeting today.” Since the minutes are a recap of the discussion there should logically be some further colour on offer. If not, and Powell just misled all of us such that there will be no discussion on cuts, then that could indicate that the Committee’s head isn’t anywhere close to courting a deeper dialogue on when to ease than what they loosely conveyed in the dots.

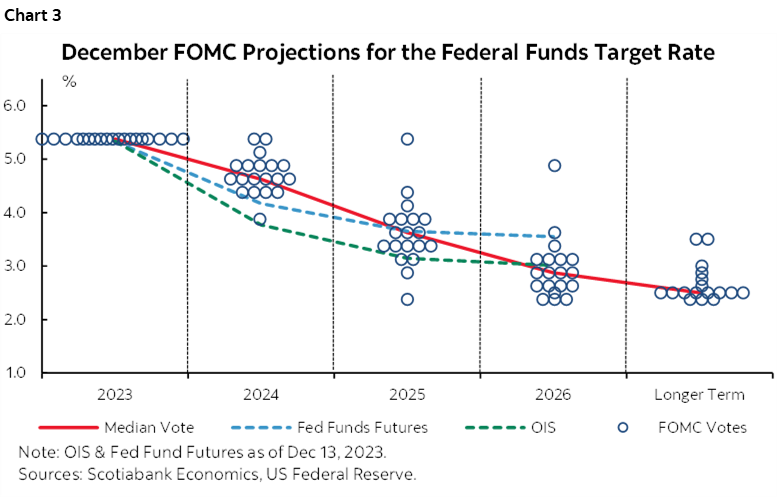

Assuming there will be a meaningful dialogue, I expect the outcome to reflect the same diversity of opinions that we saw in the dot plot from December’s meeting (chart 3). Recall that the median FOMC participants’ ‘forecast’ was for 75bps of easing this year. That was also the mode. That said, the fat tail risk was toward less, rather than more. Of the 19 participants, only 5 anticipated more than 75bps of easing versus 8 that expected less. There were two holds, one -25bps call, 5 at -50bps, 6 at -75bps, 4 calling for -100bps and 1 at -150bps. So what did markets do? They went with the one outlier call and are pricing over 150bps of easing this year. As argued at the time and once again in the holiday edition of the Global Week Ahead (here), I thought markets got carried away.

Using the Fed’s frequency of citations language, I would expect the minutes to indicate that a majority think that a modest amount of easing may be required this year. We may see language like how a majority, or most, expect modest cuts. They might say that while all recognize progress, many/most are aware of history’s cautions against prematurely declaring victory.

So will the minutes matter to markets? They might, but it’s hard to have much conviction given that a) markets are already pricing more than double the median FOMC participants’ forecast amount of easing this year, and b) markets are not really listening to the Fed in any event!

If there were to be a direct remark about how several/many/most participants don’t expect to begin easing until later in the year or something like that, then that could be impactful to current pricing for about -25bps in March and -50bps by the May Day decision. It’s unclear that the Fed wants ot get into a bun fight over meeting-by-meeting pricing at this point, but if they feel as strongly about teeing up easing moves as they did about teeing up hikes, then at some point they’ll have to either embrace pricing for March/May or lean more strongly against it.

Also note that Richmond Fed President Tom Barkin (voting 2024) delivers his economic outlook this morning (8:30amET).

US Vehicle Sales

US vehicle sales were probably little changed in December but we’ll find out toward the end of the day. Industry guidance points to about 15.4 million units sold (SAAR) compared to 15.3 million the prior month. That would mean that autos would offer little to no contribution to December retail sales except for about a 1.9% m/m SA rise in new vehicle prices.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.