ON DECK FOR THURSDAY, JANUARY 25

KEY POINTS:

- Risk-off sentiment into the ECB, key US data

- Lagarde already set the table for the ECB’s communications

- US GDP and core PCE could be more impactful to markets

- Other US macro: claims, durables, new home sales

- Canadian markets to be driven by US data after the BoC’s hawkish hold

- SARB expected to hold with inflation toward upper bound

- Norges Bank holds, higher oil prices mattered more

- German business confidence continues to slip

- Turkey’s central bank delivered a final hike

If the ECB walks and talks like Lagarde did at Davos, then the prime focus today should be upon US macro data and especially GDP and core PCE.

Overnight developments were relatively light with a couple of regional central banks and minor data. There is no follow through on yesterday’s sell off in US rates that was triggered by higher PMIs. US Ts are slightly bull flattening while European curves are slightly cheaper across countries and maturities. Oil is up a buck and supporting CAD and NOK. Equities have a slightly risk-off odour.

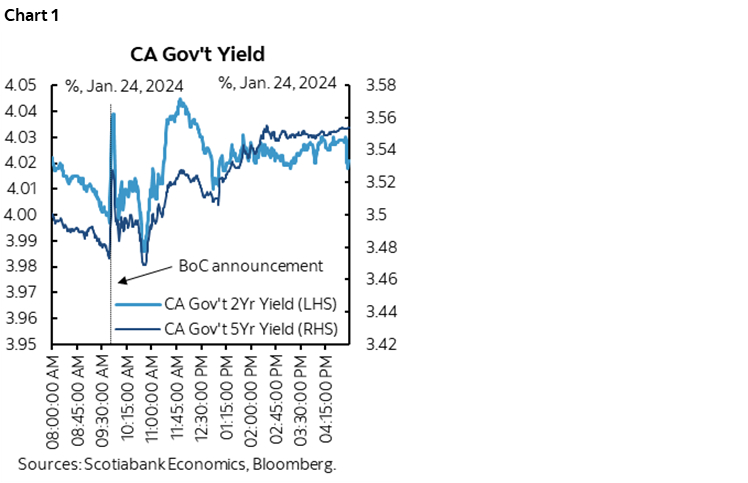

The BoC’s hawkish hold (recap here)—at best neutral, certainly not ‘dovish’—was also probably overwhelmed by Canadian rates being dragged higher along with the US yesterday (chart 1). Why I keep hearing commentary to the effect that Canada rallied post-BoC; umm....check the chart. So why did some describe it as a dovish stance? Maybe because the whole street’s economists are under enormous pressure to forecast lower rates soon. It’s not dovish when you hang out at 5%, say you plan on doing so for a while yet as everything is monitored, you say you’re not seeing the progress on core inflation that you need to see and statement codify such reference, and retain hike risk. Striking out reference to possibly hiking in the statement was meaningless as they just moved it into the Governor’s opening remarks and he spoke to ongoing hike risk in the presser. Besides, they said in December they thought they were restrictive enough in their base case assessment and so yesterday just basically repeated that while saying if inflation continues to surprise higher then hikes can’t be ruled out. A protracted hold is in their base case guidance as they leaned against nearer term cuts with all of their guidance. Dovish to hang out at 5% for a while with hike risk as they evaluate data, fiscal plans through upcoming budgets, spring housing markets, supply chain and transportation cost shocks they only indirectly acknowledged while being overly dismissive toward strong US GDP growth? Yeah right. I just don’t see it that way.

The dominant move across N.A. yields yesterday was the US curve reaction to their PMIs and in the end that’s likely what dragged Canada’s curve alongside the spillover implications for Canada. US 2s and 10s cheapened about 9bps post-data. In the end, the Canadian curve sold-off post-BoC. The BoC changed nothing in my opinion, yet 2s slightly cheapened post-communications and so did 5s that went in at 3.47% and ended at 3.55%. The BoC took reference to hikes out of the statement, and put them in the opening remarks and throughout the press conference. That’s the same unchanged net guidance they had in December when they said they thought they were restrictive enough, as long as the data goes their way. So now we watch the data.

We’ll see what today brings. Macklem’s interview with the WSJ is available now (here) but offered nothing materially different. He’ll also have an interview with Canadian Press at some point. Ignore the day’s ancient payrolls data (8:30amET).

Forget about there being any mystery surrounding the ECB’s policy communications this morning (8:15amET statement, 8:45amET presser). Lagarde’s multiple remarks at Davos last week made it clear there is no appetite for nearer term easing when she said “It is not helping our fight against inflation if the anticipation is such that they are way too high compared with what’s likely to happen.” There is disagreement among ECB officials on when they may commence easing with some preferring nearer term, some by summer, and Austria’s Holzmann saying they might not cut at all this year.

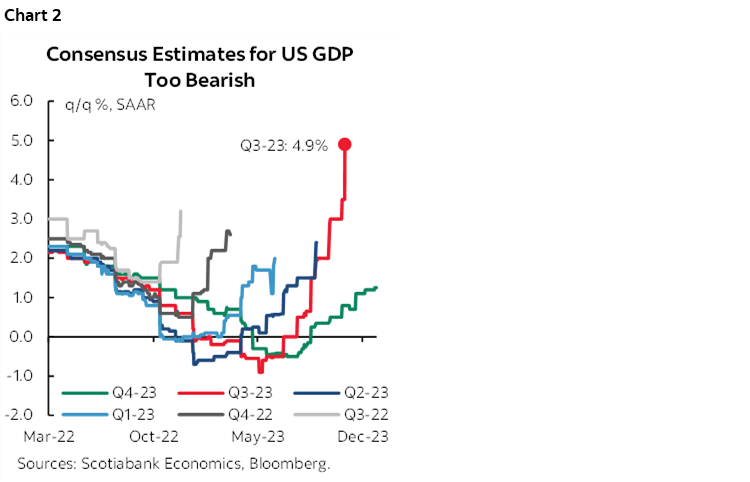

US macro data risk will be significant. Key will be Q4 GDP (8:30amET). Consensus is at 2.0% q/q SAAR. My estimate is 2.2%. Almost all within consensus lie between about 1.5% and 2.5%. This could be the sixth straight quarter in which consensus underestimated US GDP growth going into each quarter (chart 2). It kills me to hear headlines talking about some great slow down. Slower, yes, but that can’t be helped after 4.9% growth in Q3. If anything around 2% is achieved, then that would be a remarkable follow-up. Growth details will also matter, such as inventory swings.

Also keep an eye on core PCE for Q4 (8:30amET) as it may include revisions and will incorporate tomorrow’s December estimate. 2% is a common estimate based upon no revisions to monthly core PCE and tacking on 0.2% m/m as a reasonable estimate for December that would be a touch softer than core CPI.

US weekly initial jobless claims could also be worth a peak (8:30amET). They dipped to 187k the prior week for the lowest reading since September 2022. No states were estimated that week which supported data quality. Claims have been broadly trending lower since June of last year and continue to indicate a strong US labour market.

US durable goods orders should get a transportation/aircraft lift, but watch core (8:30amET). New home sales (10amET) are widely expected to rebound from the prior month’s drop with the assistance of higher model home foot traffic as a leading indicator.

SARB is expected to hold at 8.25% a little later this morning (>8amET). Yesterday’s inflation report for December remained toward the upper end of SARB’s 4.5% +/- 150bps target range with headline dipping to 5.1% y/y and core stable at 4.5% y/y.

The rest of what follows is a recap of overnight developments.

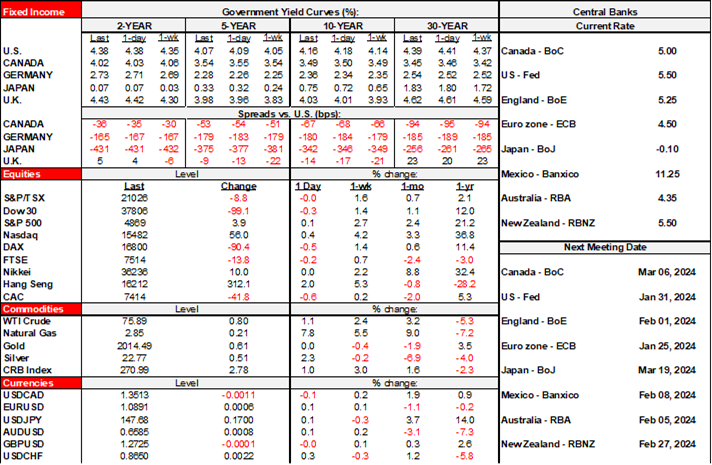

Norges Bank held its policy rate at 4.5% and guided it would stay on hold for “some time.” It dropped reference to how “the policy rate will lie around 4.5% until autumn 2024” which could be meaningful, or it could just be a reflection of the fact it was an interim meeting sans forecasts or any refreshed explicit forward rate guidance. Norway’s yield curve underperformed other cheaper European curves and the krone is outperforming, but that could also be due to higher oil prices this morning.

Turkey’s central bank—your fave—hiked 250bps to 45% as expected. It also signalled the end of rate hikes by stating “that the monetary tightness required to establish the disinflation course is achieved and that this level will be maintained as long as needed.” That was consistent with expectations this would be the final hike after the central bank said at its last decision in December that the goal was to “complete the tightening cycle as soon as possible.”

German IFO business confidence slipped a touch on each of the headline, current assessment, and expectations component. Confidence has been broadly trending lower on a volatile path since mid-2021.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.