| ON DECK FOR THURSDAY, FEBRUARY 8 |

KEY POINTS:

- Sovereign yields remain under upward pressure

- China’s core CPI inflation accelerated; forget alarmist headlines

- Banxico to hold, faces weakened case to pivot than in prior minutes

- Peru’s central bank expected to continue easing

- Mexican, Colombian CPI matched expectations

- Chilean CPI a little firmer than expected

- US jobless claims held steady

- RBI held, retained hawkish bias

- Canada only holds a 2 year-auction today, no data

- Canada’s terms of trade remain very favourable to the economy

- Canadian net trade will contribute to Q4 GDP growth

- Canadian wage settlements soared by the most since 1982…

- …and collective bargaining pressures are only just beginning

- Why shelter can’t be excluded from Canadian CPI

- SCOTUS addresses Trump’s eligibility today

A sprinkling of CPI reports and a trio of central bank decisions should translate into mostly regional market implications as opposed to being influences upon global markets. There is a slight cheapening bias across sovereign bonds as the USD gains. US and Canadian equity futures are slightly in the red along with mixed European equities. Because of light developments I’ve worked some additional content on Canada into the early morning draft of this note.

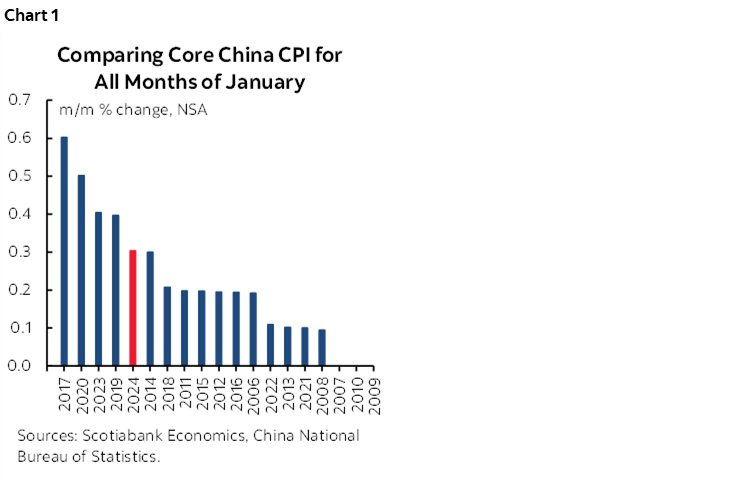

Chinese Core Inflation Accelerated

China’s core CPI inflation registered the warmest reading since July. It clocked in at 2.0% m/m SAAR in January and is the second monthly acceleration (chart 1). Year-over-year rates of inflation ebbed because of year-ago base effects that tilted higher, but that’s not the way to look at it. For instance, headline CPI slipped from -0.3% y/y in December 2023 to -0.8% in January because it was based off of a blip higher a year ago relative to the prior month of a year ago. Ergo, fade the alarmist headlines about the fastest fall in prices since coming out of the GFC as that misses the point on core inflation at the margin.

The RBI Still Sounds Hawkish

The RBI kept its repo rate unchanged at 6.5% as widely expected, but dashed some expectations it may have adopted a more neutral stance. The statement repeated reference to how the RBI “decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth” which was unchanged from the prior statement in December. The RBI Governor followed that up in the press conference by saying “The job is not yet finished, and we need to be vigilant about new supply shocks that may undo the progress made so far.” The rupee outperformed other crosses to the dollar and the 2-year climbed by about 3bps post-statement.

A Trio of LatAm Inflation Reports

A trio of LatAm inflation reports started arriving overnight with another on tap shortly. Chile’s readings were a little firmer than expected with headline CPI at 3.8% y/y (3.9% prior, 3.5% consensus) and 0.7% m/m NSA which is a little warmer than seasonally normal for a month of January. Colombia’s CPI matched expectations at 8.4% y/y (9.3% prior) and 0.9% m/m NSA in January with core at 9.7% y/y (10.3% prior) and 1.0% m/m NSA that also matched expectations.

Mexican CPI landed on the screws. It was 4.9% y/y (4.7% prior) and 0.9% m/m with core at 0.4% m/m and 4.8% y/y (5.1% prior). There were no big surprises in part because they release bi-weekly which gives a big advantage to estimating the monthly figures.

Banxico’s Weakened Case to Pivot

Banxico delivers its latest decision later this afternoon (2pmET) with a hold at 11.25% widely expected. Minutes to the prior meeting indicated that the central bank may be open to a cut toward the end of Q1 or Q2. That may be stale now after Fed Chair Powell explicitly ruled out a cut in March and sounded in no rush to ease. Our Mexican economics team notes that ongoing upside risks to inflation, procyclical fiscal policy, economic activity that has gained momentum and persistent core inflation pressures combine to add reasons to remain on hold.

Peru’s Central Bank to Stay on Track

Peru’s central bank is expected to continue cutting at a 25bps clip this evening (6pmET).

US Jobless Claims

US initial claims held steady at 218k (227k prior) as continuing claims pulled back a little to 1.871 million from 1.898. No states were estimated so it’s hard data. The figures are between nonfarm reference periods and of little significance.

SCOTUS hears Trump’s Jan 6th case today with no clarity on when it may rule on his eligibility to be on the ballot; obviously there will be no direct market implications for now, but there are pretty clear implications for the US election and economic policy thereafter.

Canada only faces a 2-year auction today and no data.

CANADIAN WAGE SETTLEMENTS HIGHEST SINCE 1982

Canada finally updated wage settlements yesterday. The average contract period of 57 months was marked by a first-year wage increase of 9.1% (chart 2) which is the hottest since 1982. Yes, 1982. The average annual wage gain over the contract period is 3.9%, or double the BoC's inflation target. It's not just the public sector where these gains are being booked, although their settlements were up by 10.6% in the first year and 3.5% on average over the contract period. C-suites are pretty happy to give away shareholder money too. Private sector deals saw a first-year wage settlement of 7.5% and an average annual wage increase of 4.3% over the contract period.

Individual numbers of employees affected by these agreements are modest in any given month but Canada is going through a multi-year repricing of labour. This is a good opportunity to reinforce points that were made in the Global Week Ahead about the state of Canadian job markets and ahead of tomorrow’s figures:

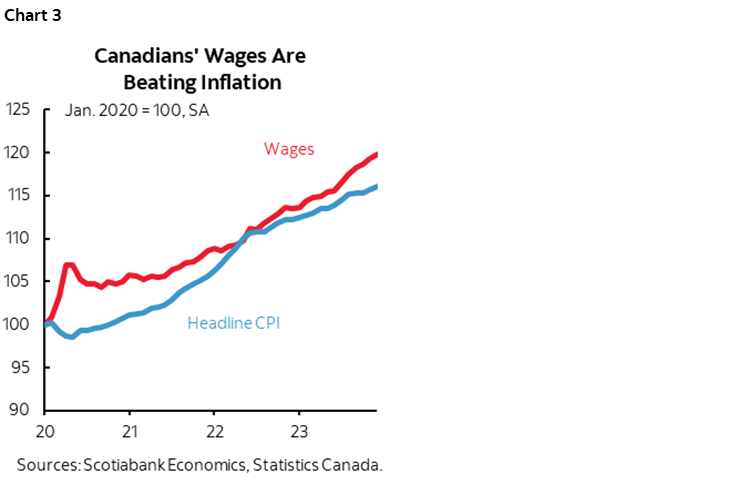

- these are not just make-up wage gains. Canadian average hourly earnings have been outpacing inflation throughout the entire pandemic era (chart 3).

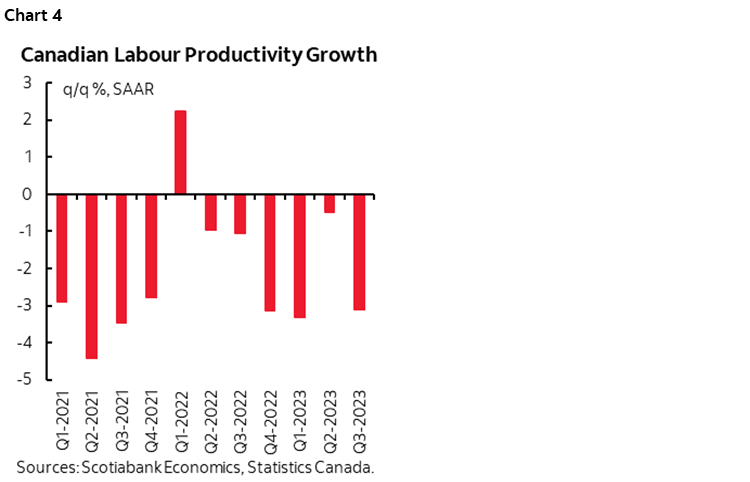

- These real wage gains are being granted despite tumbling labour productivity (chart 4). Most economists would argue that real wages should ride in sync with labour productivity over time. When that’s not the case, it’s a warning sign to inflation watchers and to the international competitiveness of Canadian labour over time.

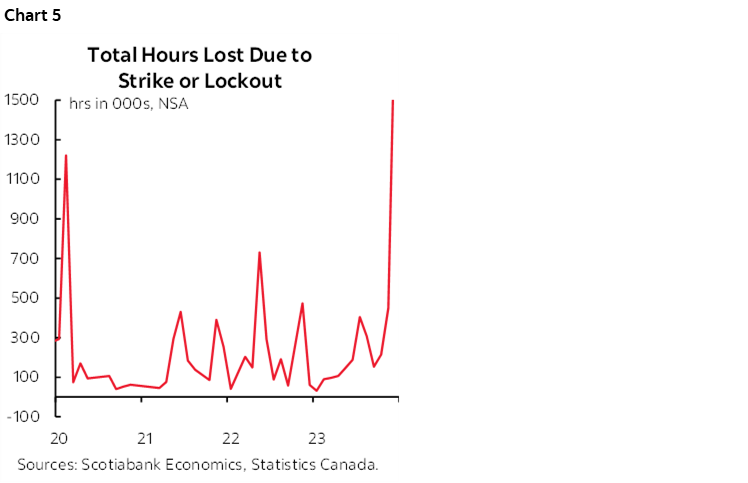

- Canada is losing more hours worked due to strikes than even during the very depths of the pandemic lock downs at the start of it all (chart 5).

- this matters more to Canada than the US where they fuss over the UAW and Hollywood. 10% of US workers are unionized versus triple that in Canada. Collective bargaining is much more important to Canada than the US.

That's a big part of the hawkish BoC narrative and a key distinction by way of relative central bank narratives compared to the Fed. Soooo.....the glass half full perspective is that it's good for the consumer especially when spillover effects into non-unionized roles unfold. That's true as long as competitiveness problems don't become so acute as to lose jobs. If that happens, it will become a matter of balancing the gains received by most against the potential job losses and where that balance resides.

The glass half empty perspective is that inflation persists, then rates stay high, don’t even begin to entertain easing.

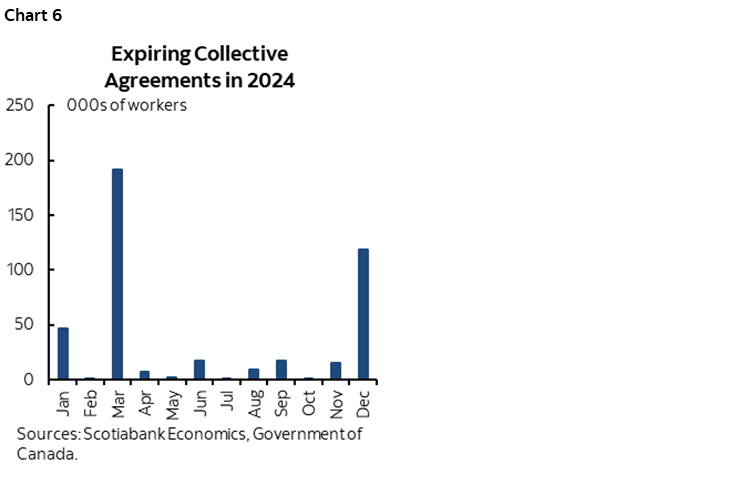

Such pressures are by no means over. In fact, we’re only getting started. Expiring collective bargaining agreements in 2024 will cover about 427k workers. Chart 6 shows the monthly distribution. Here is a list of a few of the bigger examples that are particularly focused upon the public sector with implications for property taxes, services fees, tuition and interruptions to the normal course of business:

- Alberta Health Services 70k

- Alberta government 46k

- Government of Ontario 52k

- Canada Post 42k

- Ontario Colleges 26k

- City of Toronto 11.2k

- TTC 11k

- City of Ottawa 10.8k

- Sask health workers 10k

CANADIAN TRADE TO ADD TO Q4 GDP

Yesterday’s Canadian trade figures should buoy Q4 GDP growth. Export volumes were up by +2.8% q/q SAAR in Q4 while import volumes were down -0.5% q/q SAAR. Both effects will have net trade adding to GDP growth in Q4 through higher exports but also less of an import leakage effect that, in a GDP accounting sense, adds to GDP. I’m getting about a 1% weighted contribution to Q4 GDP growth from net trade.

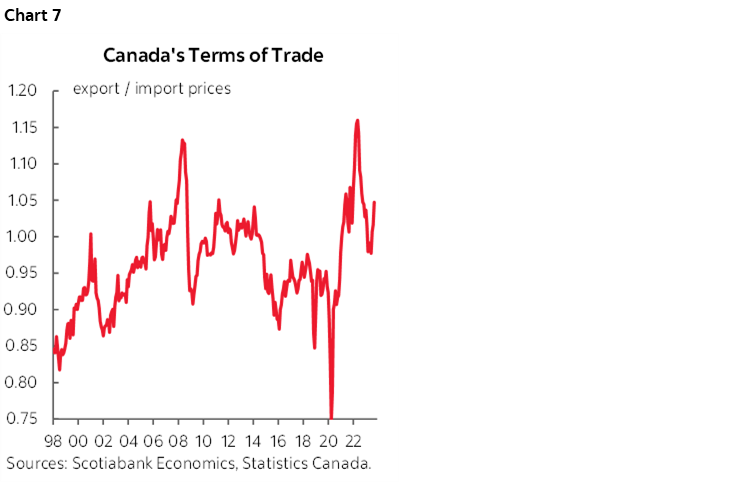

I'm also still loving Canada's terms of trade (chart 7). This matters to an open economy that trades a lot, like Canada, where trade is a much bigger share of the economy than, say, the US. An elevated terms of trade (export to import prices) is like a positive income shock to Canada's economy that trickles down throughout the sectors. It supports broad corporate finance measures as well as government fiscal balances and trickles down into the household sector. In plain language, it shows favourable prices being fetched for exports relative to what the country is paying for imports.

WHY SHELTER COSTS CANNOT BE EXCLUDED FROM CANADIAN CPI IN THE CONDUCT OF MONETARY POLICY

Governor Macklem didn’t say this, but should monetary policy look through shelter cost inflation in Canadian CPI? Macklem’s message got misinterpreted by some a couple of days ago; what I heard him say is that they target total inflation over the medium-term, but can’t ignore shelter given it is a big component, but also can’t fix affordability issues even though I disagree with his downplaying of that point as written yesterday. Here are some reasons why shelter cannot be omitted from CPI when doing so could lead to misleading interpretations about how the BoC is about to ease because the rest of the basket ex-shelter is looking like it’s better behaved.

- Upside risk to shelter costs may well intensify into the Spring housing market.

- Multiplier effects of shelter on other categories could become material. Therefore it’s not clear that shelter crowds out pricing power in the rest of the economy as opposed to buoying more widespread pressures.

- In today’s environment, households don’t differentiate between sources of inflation in forming expectations and changing behaviour. They just think the cost of living is going up and so they demand bigger wage gains which feeds further inflation. Therefore it’s a mistake to dismiss shelter cost as a relative price effect on CPI in the context of today’s realities.

- There are multiple other sources of inflation risk, like very strong wage growth, previously flagged evidence from the S&P PMI for Canada that service sectors plan on passing on higher wages and other costs through prices, moribund labour productivity, excessive immigration, a very slow movement toward excess supply that may be interrupted into 2024H1, excessively stimulative fiscal policy that may become more so (witness the NDP’s repeated warning yesterday) etc etc.

So why the misinterpretations of what the Governor said? He himself put it best in Le Devoir when he said:

"The financial markets think that if we are not raising rates, we must lower them. But it is also possible to maintain them."

In that same interview, Macklem repeated that neutral was likely higher: “When we use the models with historical data, it suggests something between 2% and 3%. When we look at the future, it’s more likely that it will be higher than lower."

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.