| ON DECK FOR TUESDAY, FEBRUARY 6 |

KEY POINTS:

- Global markets stabilize

- Canada’s housing markets is on fire again

- PMIs point to hot US and Canadian services inflation

- BoC won’t cut until September if all goes really, really well, hike risk still alive

- Fed won’t cut until Q3, can’t rule out hikes either

- BoC’s Macklem to deliver a rather awkwardly timed speech

- Eurozone inflation expectations hold firm

- RBA sounded hawkish, markets plugged their ears

- German factory orders totally embarrassed consensus

- The good and the bad and what not to do about Canadian bankruptcies

Small movements are being registered across global bond benchmarks, the USD and equities this morning in the absence of major global developments, or at least not ones that markets are choosing to put a whole lot of emphasis upon. Eurozone inflation expectations held firm, the RBA sounded hawkish but was ignored, German factory orders soared, and Canadian home sales are on fire again ahead of a speech by Governor Macklem.

BoC and Fed Forecasts

The whole Scotia Economics team throughout the Americas put out its latest forecast update this morning that revises several things compared to the prior forecast back in mid-December. The main changes are to the Fed and BoC that better reflect my views on the two central banks as written for some time.

The BoC is forecast to stay on hold until September at which point it cuts by 75bps over the final three meetings of this year. A lot has to go smashingly right to get to cuts and I think hike risk remains. To institutional investors, the advice remains to focus upon continuing to fade any nearer term cut pricing and not get too excited around views beyond the next few meetings at most after which let’s just say the picture gets increasingly cloudy. To borrowers, my advice is to continue to do what you must and/or can on the assumption that no—or minimal—cuts may be delivered this year. If cuts do eventually arise—or especially if hikes resume—then you will be better positioned. I get that this is going to be easier for some than for others.

The Fed is forecast to cut in Q3 with 100bps of cuts this year. I don’t like a cut by May 1st partly on the difficulty around easing on the heels of what is at present shaping up to be another ripping Q1 economy with Q1 GDP due six days before that decision. It’s also difficult to imagine that the Committee would have comfort to explicitly tee up a cut in June at the May meeting. The Fed’s dual mandate is the focus of course, but economic growth is among the influences upon jobs and inflation. The US economy is showing no signs of moving toward building disinflationary slack that would give comfort that 2% inflation can be durably achieved, while wage growth in m/m SAAR terms is trending higher and supply chain risks are material. A massive cooling of the US economy and concomitant implications for jobs and inflation would be required to get to cuts and I just don’t have the faith in such a view at this point partly because the view that the US economy faces imminent slowing has been around for seven quarters now and has been blown out of the water in each and every one of them.

RBA Sounds Hawkish, Markets Didn’t Listen

A hawkish sounding RBA was shaken off by markets. The 2s yield ended the session unchanged compared to just before the statement, pricing for the March decision added about 6bps to price half of a quarter point cut and a quarter point cut remains priced for the August meeting. The A$ is flat compared to right before the communications landed.

RBA Governor Bullock et al did not sound like they were in any rush to cut rates. In fact, she described rates risks as “fairly balanced” with inflation still “too high” and said “a further increase in interest rates cannot be ruled out.” Thank heavens they avoided the BoC’s botched job on the latter issue. The messaging was about how “we are not ruling in anything or out anything” and “need to stay the course.” Revised forecasts expect inflation to come close to the mid-point of the 2–3% inflation target range only by the end of 2026 at 2.6% for headline and trimmed mean. RBA watchers will then have an eye on things like the next wages report that is going to be set against an accelerating trend.

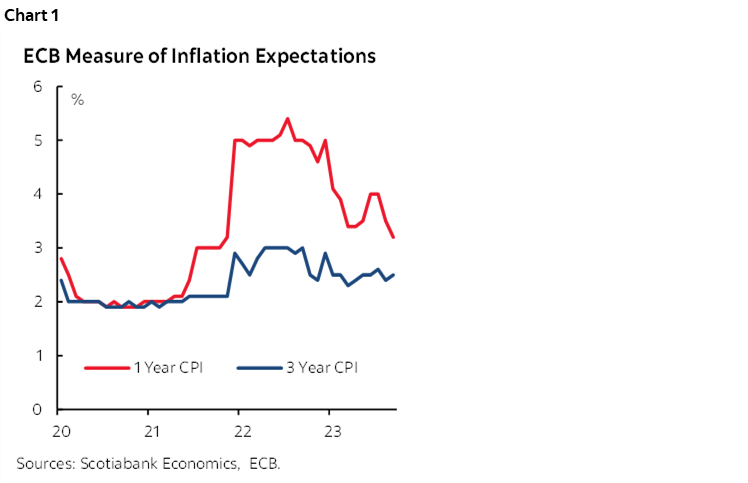

Eurozone Inflation Expectations

Eurozone inflation expectations held firm in December according to the ECB’s measures (chart 1). Upward revisions were key. 1-year CPI expectations stood at 3.2% y/y but the prior month was revised up to 3.5% from 3.2%. 3-year CPI expectations moved up a tick to 2.5% from an upwardly revised prior reading of 2.4% (from 2.2%). How can they revise a survey, you ask?? Because they added some countries including Austria, Portugal, Ireland, Finland and Greece. I never knew these countries were not previously included as it was understood to be a Eurozone-wide survey. Who knew??!!

German factory orders embarrassed consensus. They were up by 8.9% m/m SA in December (consensus -0.2%) and revisions don’t explain anything about the beat. The gain was driven by a 10.9% m/m jump in capital goods orders mostly from outside of Germany and an 8.3% increase in intermediate goods mostly from within Germany as orders for consumer goods slipped 1.3% because a surge in domestic demand was offset by a drop in foreign orders.

Canada’s Housing Market is Doing it All Over Again

Canada’s housing market is on fire again. Add Toronto and Quebec to the list of regions reporting strong sales after Vancouver and Calgary surged in last week’s reports. Toronto’s existing home sales (here) were up by 9.6% m/m SA in January as reported by TREB this morning. Montreal’s sales were up by an estimated 5% m/m SA that was derived by taking NSA data from the source and applying the average January seasonal adjustment factor in recent years. Quebec City’s sales were up over 2% m/m SA after a surge of about 12% m/m SA in December. The nationwide total figures for home sales will be released next week and are likely to add another strong gain to the prior month’s 8.7% m/m SA surge; a high single digit gain seems assured. From what I’m gathering from various sources, more strength very much remains in the pipeline ahead of the Spring market.

This is happening even earlier than I had thought it would. I’ve always thought that the only folks who buy homes in January do so either because they absolutely must (job change, lifestyle change etc) or because they are masochists in this kind of climate. To be getting hot numbers like these already is a stern warning sign. That the market would be strong into Spring should shock no one, however, as I’ve been warning about massive immigration, little to no supply, a ripping job market that created 430k jobs last year, soaring wage gains, affordable mortgage rates, and evidence that first time homebuyers have been amassing bigger downpayments. The next question is whether the BoC should respond.

BoC Governor Macklem Cannot Ignore Housing Like Poloz Did

BoC Governor Macklem delivers a speech on ‘The Effectiveness and the Limitations of Monetary Policy” and hosts a press conference afterward. The speech text will be available at 12:45pmET and the press conference will be held at about 2:10pmET, give or take.

There may be a sense of helplessness in this speech. The overall tone might be an extension of some of his arguments to date. Namely, that monetary policy is working, where it is working, and how it cannot address other issues like housing. As written numerous times, I think he has been overstating where monetary policy has been working by ignoring all of the serial shocks to hit the Canadian economy. I think he is wrong to dismiss his powers over housing which is the most rate sensitive sector going.

More fundamentally, I think he slopes off responsibility for housing excesses too readily to others by saying it’s everyone else’s fault in terms of supply management. Yes there are supply issues. But the BoC has serially overstimulated housing in one cycle after another and the real cost of mortgage debt is doing it again. Former Governor Poloz could get away with what he did to impair housing affordability because he could point to reasonably low inflation.

Macklem cannot do the same. This time the stakes are higher. With inflation expectations already unmoored amid evidence that behaviour has been changing as a result (eg. wages and productivity), each new serial shock to inflation risk results in people losing additional faith in ever durably hitting 2% and so they go on changing their behaviour in the same unhelpful ways. The tendency across some other economists and the BoC throughout too much of the pandemic has been to have serial excuses for inflation and to counsel ignoring it. That’s how we got into this mess and imagine had the BoC looked through them all and held; CAD would be the northern Turkish lira and inflation would be totally off the charts.

Furthermore, there are other drivers of inflation risk beyond housing including ones that I’ll cite below on the services side, plus others like wages, productivity, immigration, fiscal excess, an undervalued CAD etc etc.

So, if I see the Governor shrug his shoulders and say he can’t do anything about immigration, housing, etc, and the ties to inflation, then it’s added cause to think that inflation risk will persist without the BoC doing much about it. Go ahead, don’t listen, push wage demands even higher. The BoC cannot forecast inflation and has a poor track record at doing so anyway.

On that note, maybe Canadian wage settlements will come out today after all. I was told by the source that they were supposed to be out yesterday and are about five weeks behind the normal schedule as it is.

Hot US, Canadian Services Inflation

It’s not just housing that is a challenge to inflation in Canada. Another warning on Canadian inflation came in yesterday’s composite PMI from S&P for January:

"Service providers also noted that typical wage costs had risen at the start of 2024, and this was a key factor behind the latest acceleration in overall input cost inflation. According to the latest data, input prices rose to the greatest degree for three months and remained historically elevated. Firms were also willing to pass on these costs to clients in the form of increased output charges. January’s survey signalled that average tariffs rose to the greatest degree since last July."

That services inflation is very much alive and kicking in N.A. was further evidenced by the US ISM-services report yesterday. Here’s what they had to say about prices:

"Fifteen services industries reported an increase in prices paid during the month of January, in the following order: Real Estate, Rental & Leasing; Arts, Entertainment & Recreation; Construction; Other Services; Educational Services; Health Care & Social Assistance; Wholesale Trade; Public Administration; Professional, Scientific & Technical Services; Retail Trade; Finance & Insurance; Management of Companies & Support Services; Utilities; Information; and Transportation & Warehousing. The only industry reporting a decrease in prices for January is Agriculture, Forestry, Fishing & Hunting."

US Only Faces Fed-Speak

Fed-speak will come from Cleveland’s Mester (12pmET), Minneapolis President Kashkari (1pmET), Boston’s Collins (2pmET) and Philly’s Harker (7pmET). There are no US releases on tap today.

The Good and Bad and What Not to Do About Canadian Bankruptcies

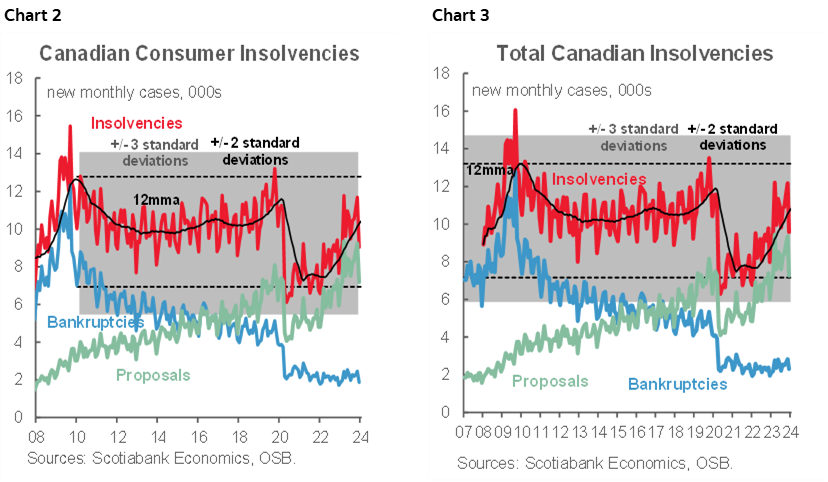

Canada released bankruptcy figures for households and businesses yesterday. Some balanced context is needed relative to how the numbers are being portrayed elsewhere.

First, consumers continue to do what it takes to adjust as bankruptcies remain toward record lows (chart 2). Insolvencies are rising due to proposals which continues a longstanding trend, but they are not showing up in bankruptcies. This reflects public policy supports and a very different banking model in Canada. The consumer side is weighing down total consumer and business bankruptcies in Canada (chart 3). This may also have a side narrative; there can be a fuzzy line between consumer and small business finances.

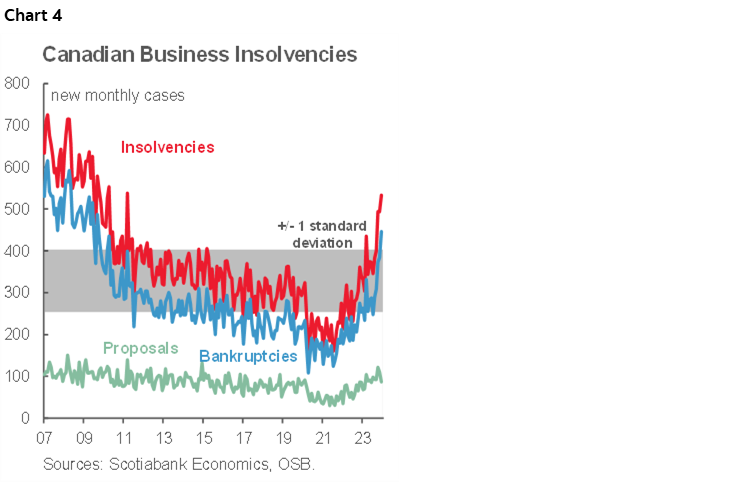

Canadian business bankruptcies, however, are soaring (chart 4). That’s unfortunate, but sound public policy has to take this in stride. If you want Canada to improve its moribund productivity, then let's not have governments stand in the way of this. Business bankruptcies had been plummeting when Canada was granting handouts galore that covered rent, wages, etc and offered preferential loans. That was sound policy at the very start when public policy did what it should in response to an awful shock no one deserved but these supports were maintained for far, far too long and were too generous. I believe that's one reason why Canada’s labour productivity has stunk for years while US productivity growth is surging. The country went too far in making businesses whole. This prevented any hope of the market clearing and reallocating resources from firms and industries that were undergoing structural and cyclical changes that were dampening prospects to firms/industries that faced better prospects. The result was an inability to fill vacancies in sectors that needed the workers and hence there was a permanently lost of output, impaired productivity, excess inflation, and upward effects on the cost of capital. Now the market is working it out. There are multiple costs, but they are delayed costs that should have been allowed to unfold more gradually and earlier.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.