ON DECK FOR THURSDAY, FEBRUARY 22

KEY POINTS:

- Risk-on sentiment driven by earnings and data

- PMIs improve across most major markets...

- ...including a signalled end to the UK’s technical recession

- Canadian retail sales: watch December details and revisions, January guidance

- Where does it say that the BoC’s mandate applies to just 75% of the basket??

- B.C. to kick off Canada’s budget season with more spending, bigger deficit

- US: Fed-speak, light data

- Mexico’s economy ended 2023 better than feared

- BoK, Central Bank of Turkey both held

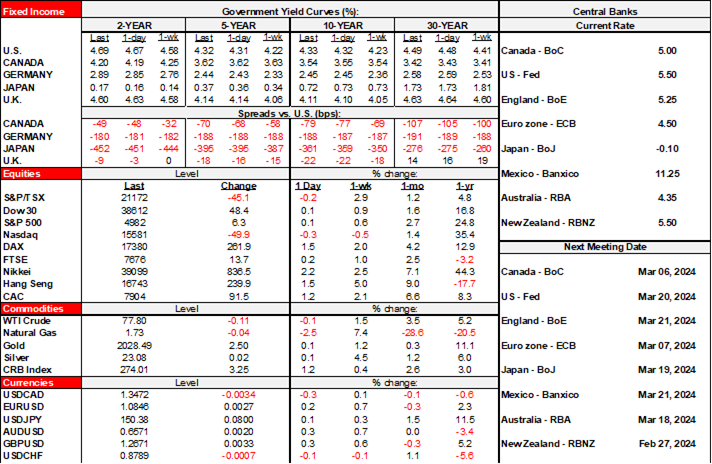

Data and Nvidia earnings are driving positive risk sentiment. After initial volatility, markets decided Nvidia’s earnings and guidance were enough to drive what is so far a 14% rise to a market cap of about US$1.7 trillion with a weight of over 4% on the S&P. S&P futures are up by 1.2% so far and therefore the rest of the rally is driven by broader sentiment including the effects of improved PMIs across most regions. European stocks are also up by as little as 0.2% in London to as much as 1.3% in Germany. The dollar is broadly softer as higher beta crosses gain. Sovereign bonds yields are mostly a touch cheaper toward the front-ends in the US and across EGBs as Canadas are flat and gilts outperform in a modest bull steepener. Gilts may be benefiting from an FT piece that flagged that Winterflood Securities will allow individual investors to buy gilts in the primary market through retail platforms.

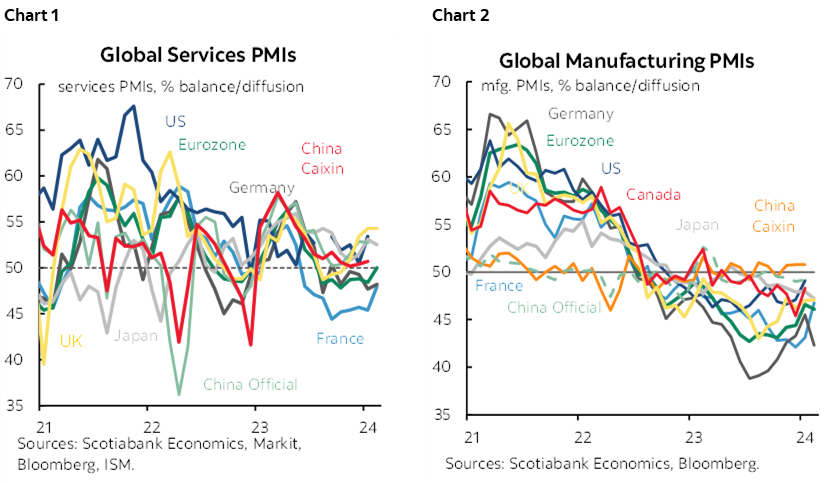

Purchasing managers indices improved across most major markets and are shown in charts 1 and 2.

- Eurozone: The composite PMI increased by a full point to 48.9 which still remains in contraction at a sub-50 reading. The improvement was entirely due to services that climbed 1.6 points to 50 while manufacturing slipped a half point to 46.1.

- UK: The composite PMI edged up a bit to 53.3 from 52.9 and hence signals a return to growth in Q1 after two back-to-back contractions in GDP. The composite PMI has risen from contractionary readings up to October and steadily climbed since then.

- Australia: Here too, the composite PMI edged up 2.8 points to 51.8 and was entirely led by services (52.8 from 49.1) as manufacturing fell back into contraction (47.7, 50.1 prior).

- Japan: Here is the one exception. The composite PMI fell 1.2 points to 50.3 as both services (52.5, 53.1 prior) and manufacturing (50.3, 51.5 prior) retreated.

- India’s composite PMI was little changed but still signals quite solid growth. The composite landed at 61.5 (61.2 prior) as both services and manufacturing edged a little higher.

The US will update its S&P PMIs later this morning (9:45amET). They are not the Fed’s preferred gauges because they track global operations as opposed to the ISM measures that track domestic operations in keeping with the Fed’s primary focus upon the domestic economy.

The Bank of Korea held its base rate at 3.5% as universally expected. One board member advocated nearer term easing and that was seized upon by markets that drove a slightly richer front-end. Governor Rhee Chang-yong nevertheless argued against nearer-term easing over 2024H1.

The Central Bank of Turkey left its one-week repo rate unchanged at 45% as widely expected under yet another new Governor. The bias points to a protracted hold with ongoing hike risk that is data dependent upon inflation.

Mexico’s December reading for the economic activity index was better than feared at –0.05% m/m (-0.4% consensus). Bi-weekly core CPI was a touch softer than expected at 0.2% w/w (0.3% consensus). Q4 GDP was left unchanged at the original estiamte of 0.1% q/q 0.1% q/q SA nonannualized.

There will be three things to watch into the N.A. session:

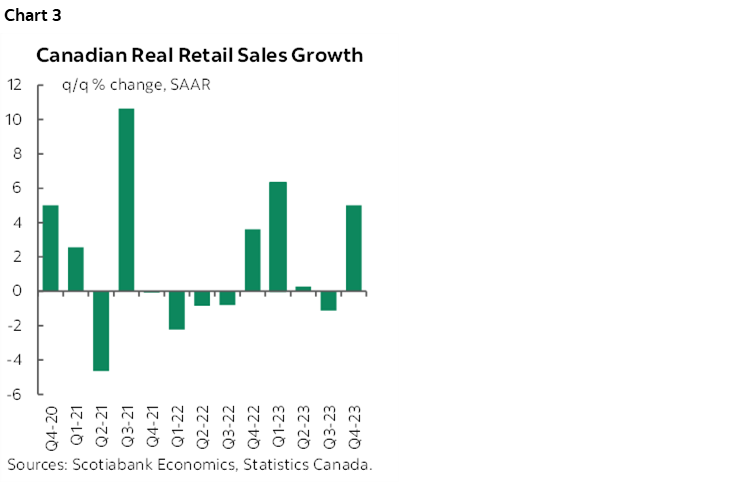

1. Canadian retail sales (8:30amET): A strong December flash estimate of +0.8% m/m for nominal sales is subject to revision, but the fresh info will be the January flash. We know auto sales were sharply higher in January, but will that be enough to carry the January headline? Recall that consumers powered a sharp gain of 5% q/q SAAR in Canadian retail sales volumes during Q4 (chart 3).

2. BC Budget: The veil will lift at 4:10pmET as BC fires the opening shot on Canada’s government budget season. Finance Minister Katrine Conroy has already guided that there will be more spending and a bigger budget deficit to help with the cost of living. That’s been what I have expected as a general theme for Budget season in Canada as more government spending continues to fight the Bank of Canada’s efforts to control inflation. Spending is expected to focus upon housing assistance and support for small businesses as CEBA loans expire.

3. Five Fed speakers will fight over the microphone today. There will also be light US data beyond the PMIs including existing home sales during January (10amET) and weekly initial jobless claims (8:30amET). Fed speakers will include Jefferson (10amET), Harker (2pmET), Cook (5pmET), Kashkari (5pmET) and Waller (7:35pmET).

THE BANK OF CANADA CAN’T EXCLUDE SHELTER FROM ITS MANDATE

A persistent point of debate in Canada is whether the Bank of Canada should be pivoting toward cutting by reprofiling the CPI basket to exclude shelter costs because ex-shelter, current inflation is otherwise relatively tame. Here are reasons I see that as profoundly bad advice.

- First, ignoring shelter is another manifestation of the exclusion principle that led to bad advice to the Bank of Canada throughout the pandemic. That approach started with a prior about what the central bank should be doing (hiking less, or in the current context, cutting soon) and then defined the CPI basket in a selective way in order to achieve such an outcome. Talk about data manipulation to suit the narrative! That’s how the central bank got caught flat-footed by reacting too late because it misread too many of the inflation warning signs and then we got saddled with high inflation and bigger hikes than we would have otherwise needed. The camp that says remove shelter from the basket now to merit cuts risks doing the exact same mistake.

- Second, the BoC’s mandate is to achieve 2% inflation over medium-term. It is not 2% inflation over the medium-term excluding a quarter of the basket! That quarter of the basket is about what you get when shelter’s 28% weight is reduced by removing mortgage interest cost’s weight of under 4%. To ignore shelter, the BoC would be derelict in its duty to deliver upon its mandate and that would be a disturbing sign to markets. Ignoring a quarter of the basket is metaphorically akin to ignoring the elephant that’s standing on your head.

- Third, I think shelter cost inflation is going to be persistent and ignoring its weight could result in never being able to durably achieve 2% inflation.

- Fourth, I think shelter cost inflation is associated with other types of inflation through activities that are complementary to housing. Anyone who has bought a new or existing home knows this because they’ve had to buy a new roof or windows or backyard deck or landscaping or furnace or that shiny new car to go in the driveway of the new digs. Ignoring shelter in CPI and the risks to its outlook can be tantamount to ignoring too many other components of the basket.

- Fifth, context matters. When former Governor Poloz cut in 2015 and was dovish afterward, he could do so without fussing over the fact that he inflamed housing markets because inflation was low, inflation expectations were on target, and inflation risk was also low. It was a different world. Macklem doesn’t face the same conditions as Poloz did. We’ve had a very recent soft patch in underlying inflation and need a lot more evidence to avoid easing prematurely and lighting it up again. Expectations are still at or above the upper end of the 1–3% inflation target range. Inflation drivers and inflation risk are still much alive.

- Sixth, the view that one can exclude shelter assumes there are no such other drivers of inflation risk that are still out there. Yes there are. The list includes soaring real wages, tumbling productivity, excessive immigration, housing shortfalls, ongoing fiscal pump priming, pressured global supply chains, only slight excess supply conditions, etc etc. It’s not just about backward looking and volatile recent inflation data!

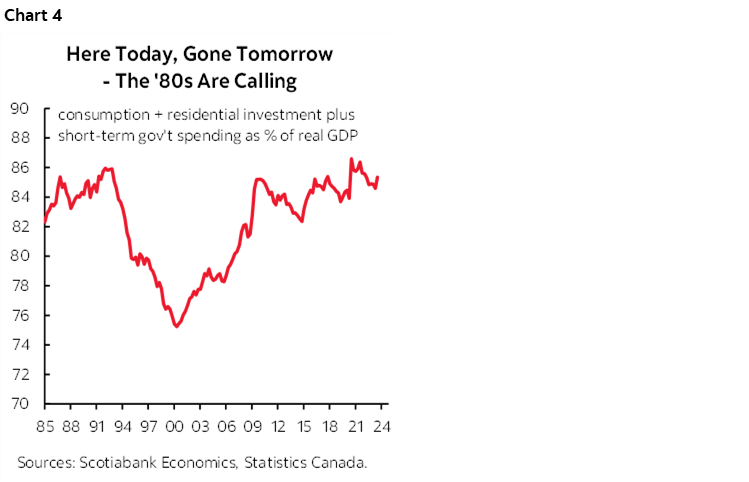

- Seventh, there is an argument to be made that excessively low rates over Poloz’s period raised the weight on current spending as a share of GDP to today’s eye watering levels (chart 4). That made Canada an economy that spends it all on here-today-gone-tomorrow current consumption which magnified longer run inflation risk with proportionately less spent on investment and hence upon improving productivity. A strict focus upon inflation targeting can have its downsides over time. Consumption plus residential investment plus short-term government spending (excluding their capital budgets) equals an astounding 85% of GDP. That’s ten points higher than in 2000 and back to late 1980s levels. Who cares? I’ll quote a former BoC Governor:

“Shorter-run biases in economic policy stack the deck in favour of inflation. So while accommodating and encouraging inflation is all too easy, limited and reducing inflation is not.” —John Crow, Governor of the Bank of Canada, 1987–1994.

- Finally, inflation expectations and changed behaviour as indicated by wage setting exercises are driven by overall inflation. Consumers don’t differentiate between different sources of inflation and instead look at broad cost of living pressures. Ignoring a major driver of those cost of living pressures risks being out of touch with how expectations are formed and how behaviour changes in ways that threaten the BoC’s ability to deliver upon its inflation mandate.

So in all, I find that this proposition that inflation targeting should cross out the shelter component is just the latest iteration of the bias that has resurfaced throughout the pandemic to ignore this, ignore that, can't control this, can't control that—and before you know it we've got runaway inflation and fundamental changes in behaviour (eg. wage settlements, poor productivity).

Last, think about the extension of the policy advice for a minute. Ignoring shelter as the justification to ease in potentially premature fashion could reignite broader inflationary pressures especially if done straight into the peak Spring housing market and through another round of what I’m sure will be expansionary government budgets.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.