| ON DECK FOR TUESDAY, FEBRUARY 20 |

KEY POINTS:

- Markets return from N.A. long weekends on cautious footings

- Canada awaits an inflation report upon which nothing rests

- PBOC sensibly holds

- Chinese banks cut their key property finance rate, buoying banks

- RBA minutes confirm hike bias

- Quiet US calendar

- Global Week Ahead reminder here

Welcome back from long weekends. We didn’t miss much, but Canada will immediately liven it up with CPI on tap as the main event this morning. Chinese stocks—including banks—rallied after a key lending rate was cut. Equities elsewhere are mixed with US futures down, TSX futures steady, and mixed European exchanges. Sovereign bonds are catching a light bid led by gilts outperformance. The dollar is slightly softer on a DXY basis as Antipodean crosses outperform along with the Euro and related crosses.

PBOC Stays on Hold

The weekend only revealed that the PBOC held its policy rate at 2.5% in line with consensus but against another solid minority that speculated upon a cut. Why cut short-term rates?? The Fed’s easing is being pushed out, China’s core CPI in m/m terms is bouncing back a bit, and authorities are relying upon other easing measures like cutting RRRs, easing some regs and offering targeting stimulus.

Because the PBOC held, Chinese banks also left their 1-year Loan Prime Rate unchanged.

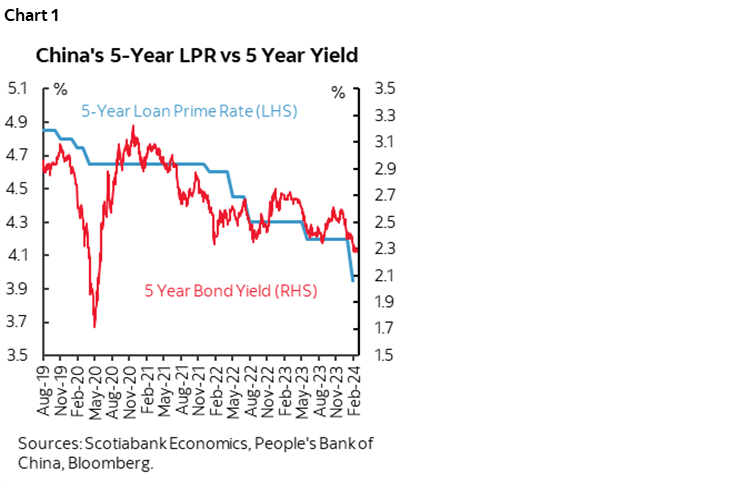

Chinese Banks Cut Property Lending Rate

Chinese banks nevertheless cut the 5-year Loan Prime Rate by 25bps to 3.95%. This measure is key to the property finance sector, as it is in Canada. The 5-year LPR can tend to move lower with a lag to the 5-year Chinese government bond yield that has declined so far this year (chart 1). Despite concerns about margins, the share prices of Chinese diversified banks gained about 1%. That doesn’t mean markets are correct in evaluating the margin effects and future willingness to lend, but for now, they may be assuming that lending volumes and implications for the property sector outweigh the margin implications. Stay tuned.

RBA Minutes Handled the Hike Bias Better than the BoC

Kudos to the RBA. They avoided the BoC’s mishandling of rate hike language that deleted it from the statement but retained reference to hike risk in Governor Macklem’s opening remarks to his press conference and during the press conference. Instead, the minutes to the RBA’s February 5th meeting reinforced its hawkishness at the time by saying that they considered a hike but decided to hold while emphasizing future hike risk should inflation prove to be sticky. That’s not really new information, even though markets reacted to the headlines. When she delivered the decision on the 5th, Governor Bullock said “a further increase in interest rates cannot be ruled out” and “we are not ruling in anything or out anything.”

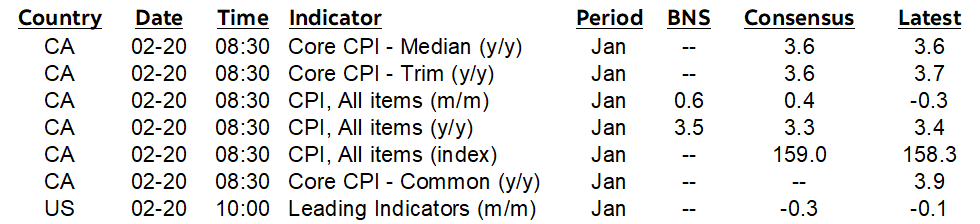

Canadian CPI—Making Something Out of Nothing

As for Canadian CPI, the January estimates arrive at 8:30amET. Please see the preview in the Global Week Ahead. There is one thing I’m pretty certain of going into the numbers: any surprise will be met by overreaction in markets even though this number on its own will determine nothing at the BoC that has made it clear they are on in a longer-lived period of monitoring data and developments.

My estimate is 0.6% m/m NSA and 3.5% y/y (3.4% prior). That would translate into 0.4% m/m SA. Traditional core CPI (ex-food and energy) is estimated to have risen by about ½% m/m NSA and by 0.3% m/m SA.

At 0.6% I’m toward the upper end of consensus with a little company; the median call is 0.4%. Most shops are between 0.3 and 0.6.

Rent should be an upside contributor again. Gasoline won’t be. A rebound in the volatile recreation/education/reading category could occur and carries a 10% weight. Watch for whether core services rebound and whether core goods CPI can build upon prior momentum.

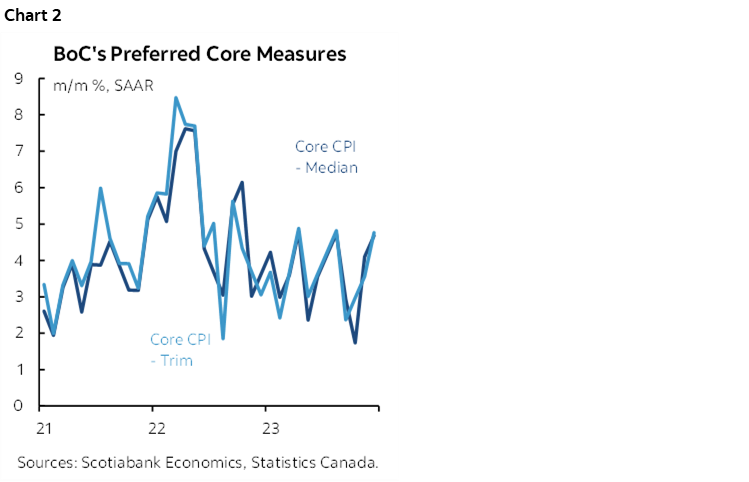

But it’s all about trimmed mean and weighted median CPI—both in m/m SAAR terms—given how clear the BoC is about those being its two preferred measures of underlying inflation and in the context of the pattern of strong readings (chart 2).

There is nothing on the go in the US today, where Trump now fashions himself to be a shoe salesman carrying Putin’s briefcase for him; would you like a shine too sir?

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.