| ON DECK FOR THURSDAY, FEBRUARY 15 |

KEY POINTS:

- Recessions? Meh. Why markets are walking it off

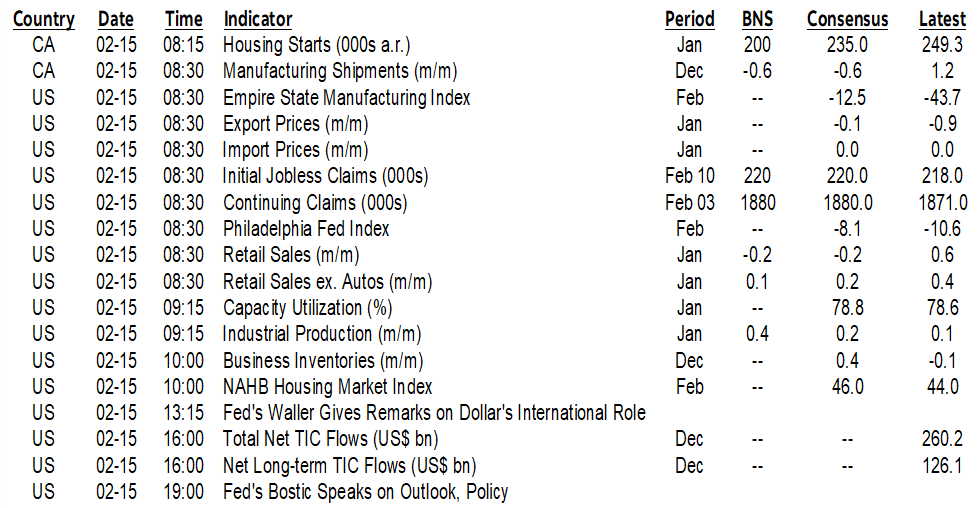

- Japan’s economy barely slipped into technical recession

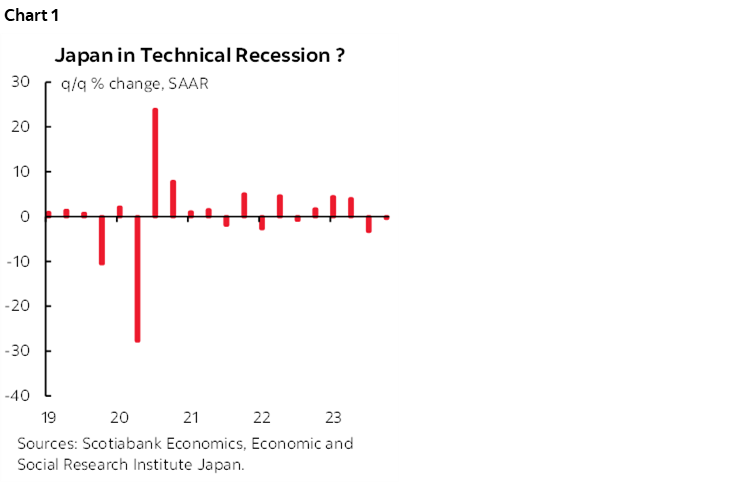

- The UK economy joined it

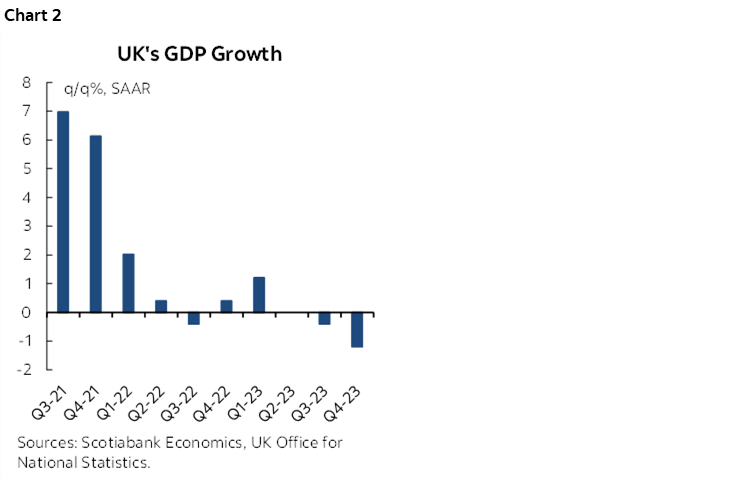

- Australian jobs were flat, failed to rebound

- Core US retail sales will inform Q1 momentum

- Canadian manufacturing sales expected to dip on price effects, starts on multiples

- Colombia’s weak economy is poised for an update

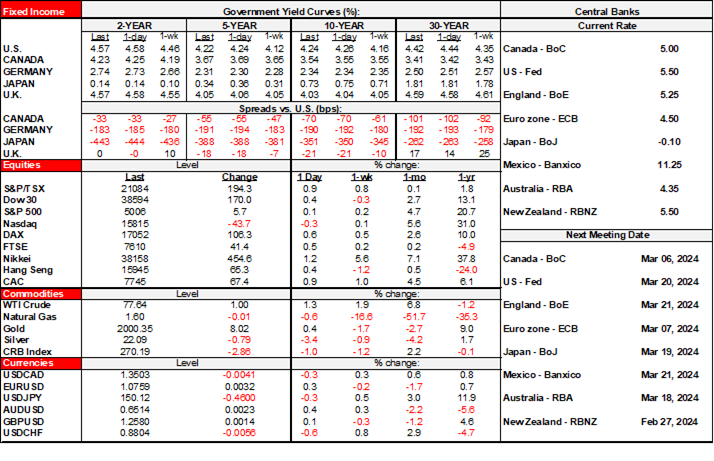

Markets are not really fussing over an onslaught of macro data and sensational headlines this morning. Bonds are catching a slight bid across US Ts and EGBs and with very small moves in gilts. The USD is very slightly softer as sterling underperforms. Equities are mostly up a touch across NA futures and most European benchmarks excluding London that’s flat.

In other words, markets are taking in stride the splashy headlines that are full of recession talk. Maybe that’s because it’s backward-looking data. Or maybe it’s because they were primed to expect readings that aren’t great but basically lean toward soft landings so far. Or perhaps it’s because real recessions need more than just a couple of small negatives, while alternative definitions of recession that also consider job markets are not really saying the same thing. Heck, for that matter, it could all be because markets are more focused upon central bank mandates that are driven by watching prices and wages.

Whatever the reason(s), the UK and Japan barely met one definition of recession overnight. More of the focus is likely to be upon the US consumer a little later this morning.

Japan’s economy barely slipped into technical recession with GDP down by -0.4% q/q SAAR in Q4 after a downwardly revised print of -3.3% in Q3 (from -2.9% previously). Weakness was genuine as consumer spending fell by -0.2% q/q SA nonannualized after a -0.3% prior contraction. Business spending also fell -0.1% q/q SA after a -0.6% drop. Inventories were a neutral contribution. So were exports that only added 0.2 ppts to GDP growth in weighted terms.

The UK economy also slipped into technical recession with GDP down by -0.3% q/q SA following a prior -0.1% contraction. Here too the weakness was genuine as consumer spending slipped by -0.1% q/q SA following a larger -0.9% q/q prior drop. Exports slid by -2.9% q/q—marking the fourth consecutive decline in a picture that has been challenged since the 2016 Brexit vote.

The UK economy also ended Q4 on a weak note that suggests Q1 is set up for a repeat. December GDP was down -0.1% m/m as services shrank -0.1% along with construction at -0.5%, while industrial output was up 0.6%.

Australian jobs were flat in January (+0.5k m/m) following a decline of 63k the prior month. The details were a little better as full-time employment was up by 11k following a prior loss of 109k. That was offset by a drop of about 11k part-time jobs.

The main focus into the N.A. session will be upon US retail sales for January (8:30amET) that are expected to be on the soft side following December’s gain. Key will be core sales ex-autos and gas that are more difficult to observe relative to the expected drag effect from lower auto sales following December’s surge. Other US releases will include the Empire (8:30amET) and Philly (8:30amET) manufacturing gauges plus weekly jobless claims (8:30amET) and industrial output (9:15amET).

Canadian manufacturing sales during December are expected to dip on price effects but watch volumes (8:30amET). Housing starts will probably dip (8:15amET) as permits for new dwellings fell sharply and volatile multiples starts pull back from December’s surge.

Colombia’s economy is expected to contract again after barely staying on the plus side in Q3 and contracting by 1% q/q SA in Q2 (11amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.