| ON DECK FOR WEDNESDAY, FEBRUARY 14 |

KEY POINTS:

- Bonds take a breather

- Gilts unwind post-jobs sell-off…

- …as core UK CPI was unusually soft

- EGBs get a lift from a solid German auction

- Let’s see just how hot Canada’s housing market was in January

- US PPI revisions to update SA factors, weights

- Indonesia’s election results are tentatively pro-business

- Immigration, rates, and homebuilding in Canada

Cupid saved an arrow for bonds this morning. Sovereign bonds are taking a bit of a breather after yesterday’s sell off. The US 2-year yield is about 5bps lower this morning but is still about 16bps higher than before US CPI. Stocks are gently higher. The USD is retaining its post-CPI appreciation and is relatively unchanged this morning. Overnight developments were light and only included UK CPI, a strong German bond auction that helped EGBs and Indonesia’s election. There is little on tap into the N.A. session this morning with just Canadian home sales and US PPI revisions due out.

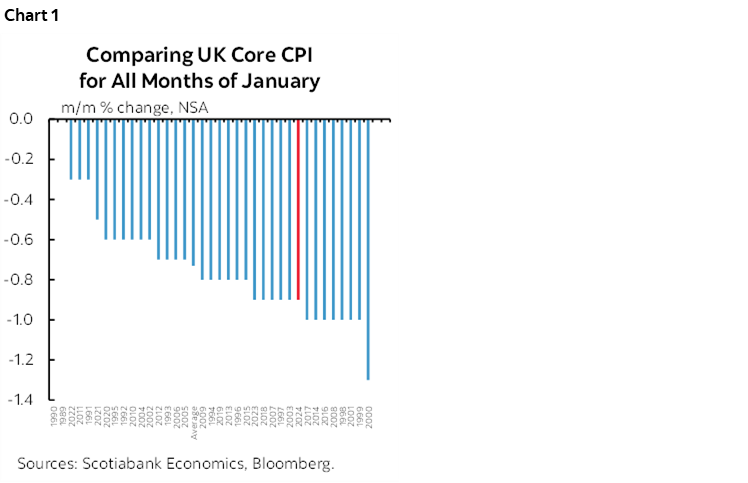

UK core CPI put in a weaker than normal performance in January. Core was down -0.9% m/m NSA versus the historical average for months of January that is more like -0.7%. -0.9 is among the weaker readings on record (chart 1). Headline CPI was down -0.6% m/m NSA, doubling the decline that was expected by consensus and weaker than all but one of the 21 forecasts.

The result drove gilts to be dearer across the curve including an 8bps decline in the 2-year yield that unwound most of the rise that began after UK jobs and wages and then US CPI. It also drove sterling to be among the weaker performers to the USD this morning.

Canadian Home Sales Were Probably Strong in January

Canadian existing home sales will probably post a second consecutive powerful gain after December’s rise of over 8% m/m SA (9amET). Major cities from Toronto to Vancouver, Montreal to Calgary and QC have registered strong gains. A market reaction is unlikely, but it will help to inform housing momentum and hence BoC policy risks. Also watch listings, the sales-to-new-listings ratio, months’ supply and the house price index that controls for compositional changes.

US PPI Revisions on Tap

US producer price revisions are due out this morning (8:30amET). Like CPI, they will reflect updated seasonal adjustment factors for the last five years and revised weights. It doesn’t carry the same pizazz as CPI revisions, but the result could still be impactful to Treasuries.

Indonesia’s Election is Tentatively Pro-Market

It seems likely that Indonesia’s election has been won by the candidate who had been leading in the polls all along. Defense Minister Prabowo Subianto is leading in early counts with official results not expected to arrive for some time. Subianto is relatively business- and market-friendly and viewed as somewhat of a continuity candidate given his role in former President Joko Widodo who hit his two-term limit. Still, Subianto is tagged for having committed human rights abuses in the past and viewed as a risk to democratic institutions. That has geopolitical analysts relatively cautious toward what to expect from his regime.

Also on tap will be minor releases including Colombia’s industrial production during December (10amET) and Russia’s CPI for January (11amET).

Canadian Immigration, Homebuilding and Rates

Canada's Housing Minister, Sean Fraser, suggested that Bank of Canada interest rate cuts would help builders build more homes and help to alleviate pressures on housing affordability. Here’s his direct quote:

"Don't ignore the impact that interest rates have on restricting supply. My expectation is if we see a dip in interest rates over the course of this year, a lot of the developers that I’ve spoken to will start those projects that are marginal today."

This comment feeds off of rising sentiment among builders and governments that housing shortages are the BoC’s fault which of course is music to the ears of governments that most would agree are to blame for decades of mismanagement of housing policies. I don’t agree with the Minister’s take.

First is that BoC Governor Macklem was correct when he recently said this:

“It’s very clear in the data that the effects of interest rates on demand are much bigger than those on supply.”

Ergo, housing imbalances would probably have worsened absent rate hikes in the past few years and would probably worsen further if the BoC were to slash rates going forward because the lift to demand would be dominant.

Second is to challenge the assertion that builders fund their longer-tailed housing developments at very short-term rates. Some, yes, in the overall capital structure mix. But with strong equity markets and the steep decline in corporate bond yields since last Fall’s peak, they’ve already seen substantial relief in their funding costs.

Third is to further explore which funding point matters most—the very short-end, or further up the curve. On that note, the Canada 5-year yield is probably only marginally higher than where it should be relative to reasonable assumptions about the neutral policy rate and term premium. I wouldn’t expect that much more relief that is already priced in 5s.

Fourth is that this whole argument latches onto a familiar complaint from builders that high interest rates prevented them from building more homes in recent years in order to meet a massive surge in immigration. It has been a challenging market for them, but I’ve previously addressed this as misguided (here).

In economics, you can’t just shock one variable and assume that nothing else about the world would change. In other words, you can’t just say that had interest rates been lower over recent years, more homes could have been built due to cheaper financing costs without having to worry about any other consequences to a lower for longer rate policy.

Why? The alternate state of the world in which rate hikes had not occurred (or the present world should the BoC cut prematurely) probably would have sparked the following consequences:

- even greater upward pressure on broad inflation, including housing input costs faced by builders.

- higher term-funding costs as markets would have ditched the country’s public and private bonds in a total loss of confidence in its ability to ever get inflation under control. The resulting lower prices and higher yields would have been sought to compensate for higher inflation risk.

- With the Fed tightening while the BoC would have been whistling by the graveyard, Canada could have been having a two-for-one sale on CAD to the USD with even more imported price inflation including housing inputs.

- And you think wage pressures and labour scarcity have been bad in recent years? Try a totally overheated economy with massive runaway inflation; wage pressures and labour scarcity would have been even worse.

But surely the demand side would have had more stimulus at lower rates to offset all of this additional pressures on costs, right? Uh, maybe not. Fixed mortgage rates would have presumably been under upward pressure alongside builders’ term funding costs on the market’s lack of faith in the country’s management of inflation risk. Variable rates would have been cheaper, for a time, until either imbalances sparked even tighter monetary policy later or until the whole powder keg blew open, creating a boom bust scenario for housing.

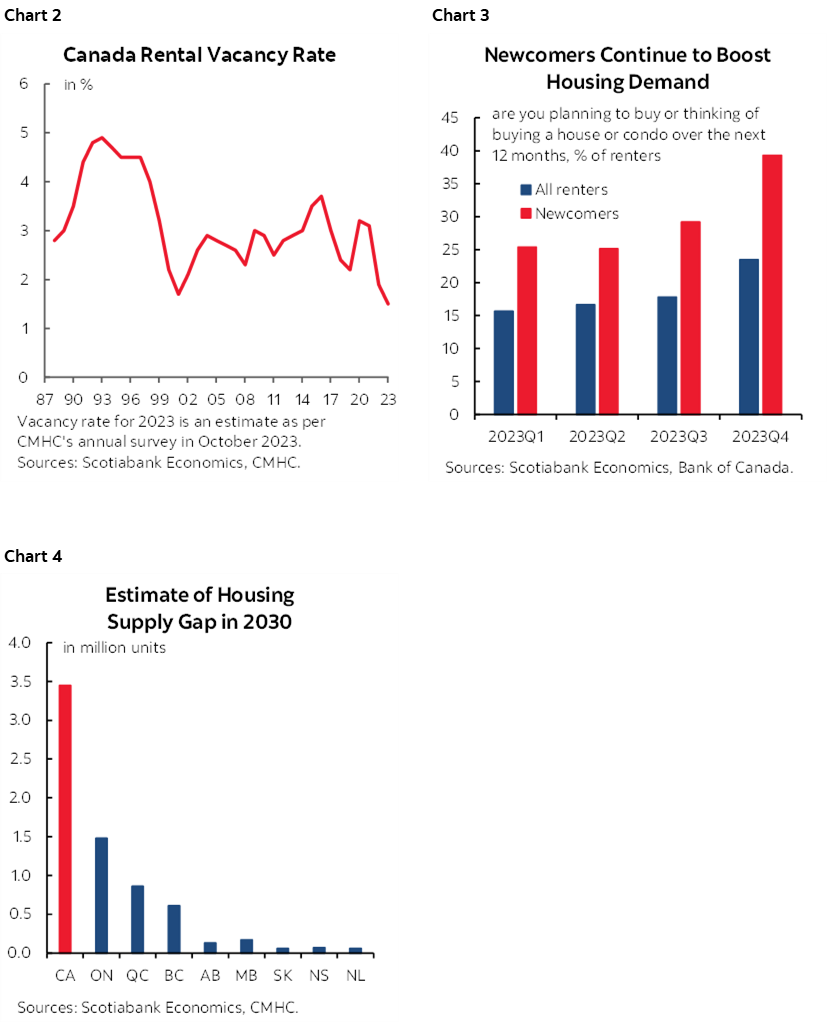

So where does this leave us? I find it disturbing that immigration policy in this country seeks to compound the policy errors. Immigration is excessive relative to the country’s ability to absorb new arrivals particularly in the most pressured cities. Period. The temp residents file was totally mismanaged. The fastest population growth in a peer group of other nations with nowhere to put them and infrastructure bottlenecks has contributed to inflationary imbalances. Rental markets are very tight (chart 2), surveys point toward surging demand for owner-occupied housing (chart 3) and the country needs vastly more homes to be built to alleviate pressures on housing affordability than anything that is likely to be delivered through modest announcements (chart 4). You can’t make up for decades of mismanaged housing supply and the compounding effects of excessive immigration overnight. Politicians need to stop scapegoating the BoC for all the mistakes that governments have made.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.