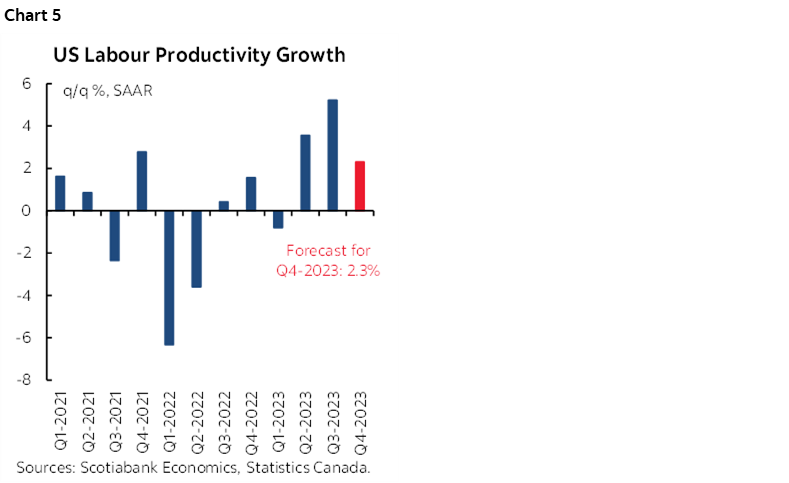

ON DECK FOR THURSDAY, FEBRUARY 1

KEY POINTS:

- Markets continue to reduce Fed, ECB, BoE and BoC cut pricing

- The Fed’s aftermath continues to reverberate through markets

- Eurozone core inflation was warm again, leans against premature easing

- Markets didn’t like what the Bank of England had to say

- BoC testimony: what’s changed since the last decision?

- US layoffs picked up in January

- US data dump: productivity, ULCs, claims, ISM, vehicle sales

- Key US tech names release in the after-market

- Sweden’s Riksbank doesn’t know what to do

- Peru to update inflation ahead of next week’s BCRP decision

Month-end transitions in markets are being swamped by the ongoing aftermath of the Fed’s communications (recap here) coupled with another warm Eurozone inflation report. The BoE disappointed market positioning into this morning’s communications as sterling appreciated and yields on gilts climbed in the aftermath so far. Also ahead are US data releases, big names in US earnings, and Bank of Canada testimony.

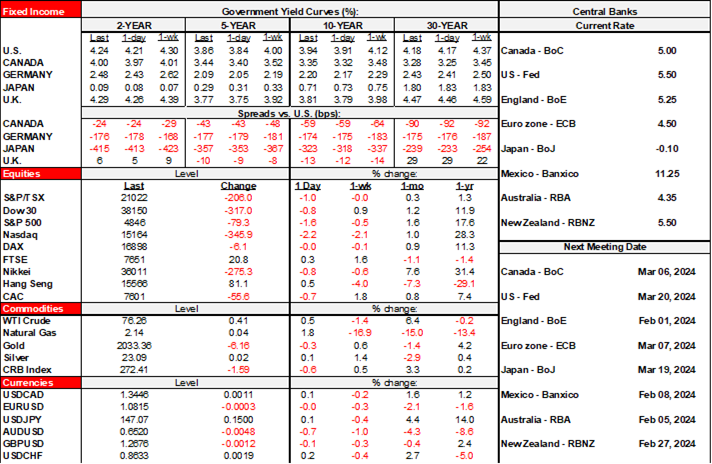

US Treasuries are cheaper by another 3bps or so across maturities with Canadian government bond yields performing similarly. EGBs are underperforming and gilts are reversing their rally into the BoE communications with yields now pushing higher. The dollar is slightly firmer against most crosses as an extension of reduced cut expectations. Stocks are in a mildly positive mood in N.A. but will be sensitive to data and key earnings, and stocks are mixed in Europe.

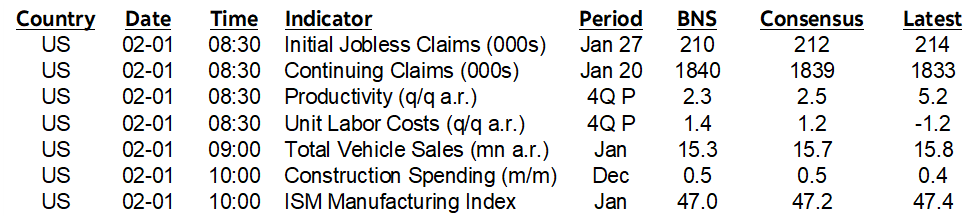

Eurozone core inflation was hotter than seasonally normal for a second month in a row (charts 1, 2). Core prices normally drop in January, but the -0.9% m/m NSA decline this January was a materially smaller drop compared to like months in history. The same was true in December when what is normally a seasonal up-month for prices was stronger than usual. EGBs were already cheapening before the data as they were playing catch-up to yesterday afternoon’s Fed communications, but the data pushed yields higher across all maturities and countries. The net effect of the Fed and Eurozone CPI also shaved pricing for an ECB cut in April by a few basis points and March has been pretty much wiped out.

Sweden’s Riksbank kept its policy rate unchanged at 4% as universally expected. Guidance was kind of muddled and sounded like a central bank that doesn’t know what the heck to do and when. Join the club. The statement said “There is less risk of inflation becoming entrenched at levels that are too high,” and that “The policy rate can therefore probably be cut soon than was indicated in the November forecast” which pointed to easing over 2025H2. It also said “If the prospects for inflation remain favourable, the possibility of the policy rate being cut during the first half of the year cannot be ruled out.” Alrighty then, so they might cut over 2024H1, or at least sooner than 2025H2 which seems like a pretty wide open window! They did not publish updated forecasts that would fill in this window and the next forecasts with explicit forward rate guidance will be published on March 27th.

Enter the BoE that delivered a statement at 7amET along with a full forecast update. While reference to further potential tightening was removed, two MPC members continued to vote for another hike with one voting to cut. Key, however, is that they retained reference to remaining restrictive for sufficiently long and for an extended period while they ‘keep under review’ how long to keep Bank Rate unchanged at 5.25%. This part of the statement (here) is key:

"As a result, monetary policy will need to remain restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term in line with the MPC’s remit. The Committee has judged since last autumn that monetary policy needs to be restrictive for an extended period of time until the risk of inflation becoming embedded above the 2% target dissipates.

The MPC remains prepared to adjust monetary policy as warranted by economic data to return inflation to the 2% target sustainably. It will therefore continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation. On that basis, the Committee will keep under review for how long Bank Rate should be maintained at its current level."

Versus previously when they said this in December:

"The MPC will continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation. Monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the Committee’s remit. As illustrated by the November Monetary Policy Report projections, the Committee continues to judge that monetary policy is likely to need to be restrictive for an extended period of time. Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures."

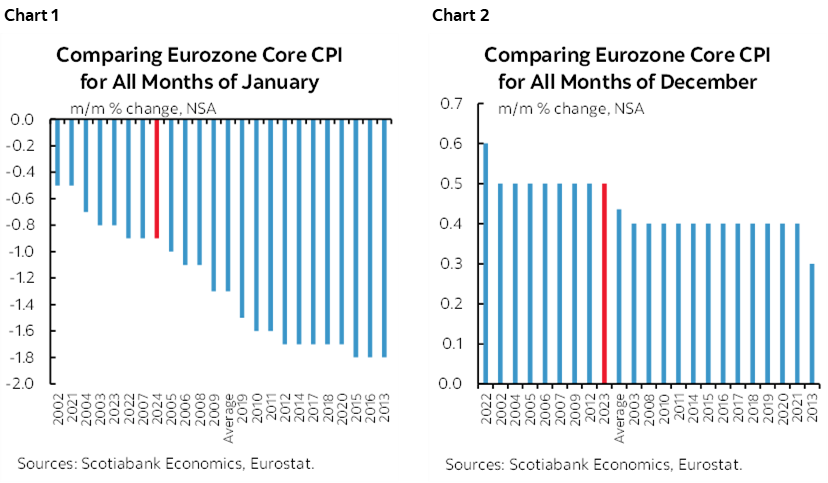

I don’t know why there was such a grand expectation that the MPC would suddenly provide easing signals in any event. Had they done so, it would have bucked the trend across central banks and arguably been a mistake. The Fed, ECB, and Bank of Canada are among the significant central banks that have pushed back against easing any time soon, but somehow the country that had the worst inflation experience of all is going to feel comfortable to embrace cut guidance? Pfft. They don’t have the recent data in their favour if they decide to do so. UK core CPI in m/m NSA terms in December was among the hotter months of December in history (chart 3). Ditto for wage growth that sharply rebounded in December in m/m SAAR terms (chart 4).

US macro readings will be a source of further market volatility this morning.

- Job layoffs increased to 82k in JAnuary from 34k in December which takes us back toward layoffs that were being record in early 2023. Maybe that’s a point in itself by way of indicating that companies enter the year with fresh evaluations and pink slips and so I wouldn’t overreact to the rise as a trend-setter yet.

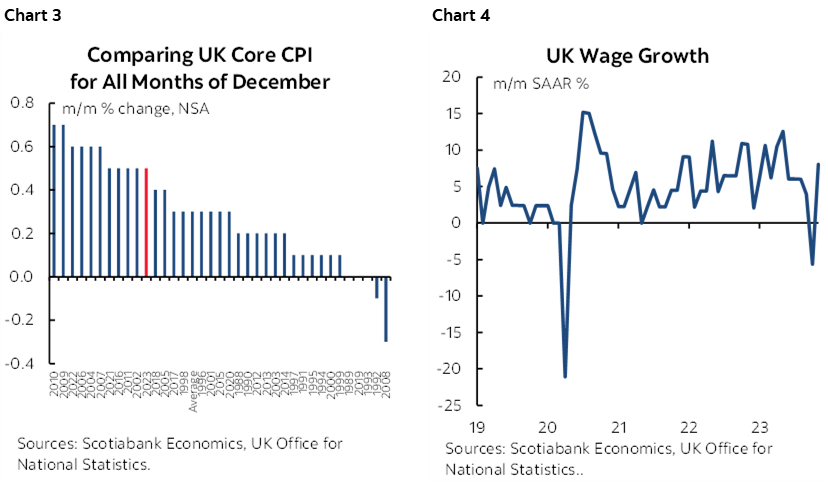

- US Q4 productivity growth (output per hour worked) is expected to slow to around half the prior quarter’s pace while still remaining respectable (8:30amET). Chart 5.

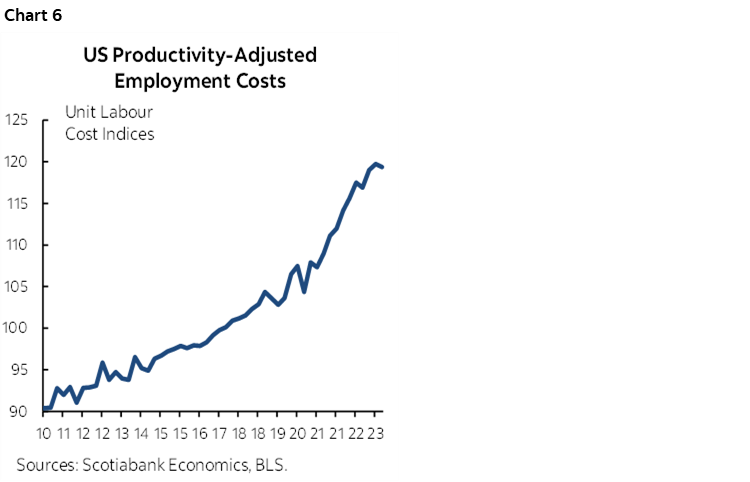

- Productivity-adjusted labour costs are expected to flip the prior quarter’s negative sign and rebound but in a relatively mild manner (8:30amET). Chart 6.

- US ISM-manufacturing for January is expected to be little changed in contraction territory along with new orders and employment. Prices paid largely follow commodities (10amET).

- Weekly US initial jobless claims (8:30amET) are outside of the nonfarm reference period and won’t influence expectations for tomorrow’s payrolls report.

- US vehicle sales during January will arrive toward the end of the day. Advance industry guidance points to an upward revision to December and a dip down to 15.3 million SAAR (e.o.d.).

BoC Governor Macklem and Senior Deputy Governor Rogers will deliver parliamentary testimony later this morning (11:30amET). It starts with opening remarks and then goes to Q&A. This might be worth a peak. Since the BoC’s communications a week ago yesterday, we’ve heard Powell and Lagarde push back against nearer term easing and Canadian GDP accelerated into year-end. Macklem is unlikely to be overly reactionary to these developments, but they continue to challenge any sense that the BoC is on track to cut any time soon.

Big names in US tech release earnings in the after-market and may heavily influence how the market tone ends the week along with tomorrow’s US nonfarm payrolls. Apple, Meta Platforms and Amazon are among the key names.

Peru’s inflation figures for January (10amET) are expected to soften ahead of next Thursday’s central bank decision that arrives in the wake of what has already been 125bps of cutting since September.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.