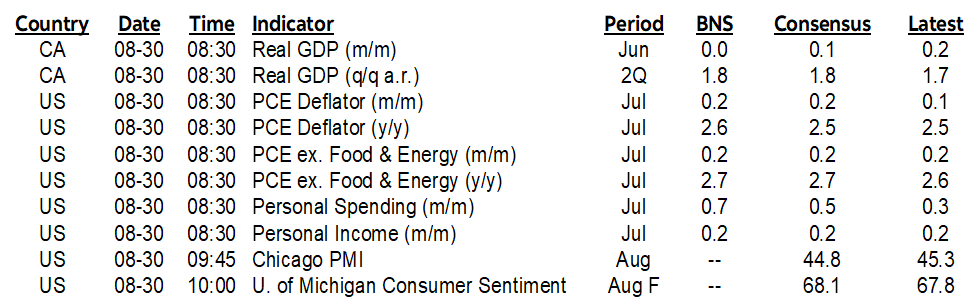

ON DECK FOR FRIDAY, AUGUST 30

KEY POINTS:

- Constructive market tone awaits key US, Canadian releases

- Hot Tokyo core CPI adds to carry trade risks

- Eurozone core inflation offers warning signs to ECB easing

- South Korean won hit by collapse in factory output

- US to post strong consumption, soft core inflation

- GDP figures will test Canadian resilience

- Early Canadian bond close

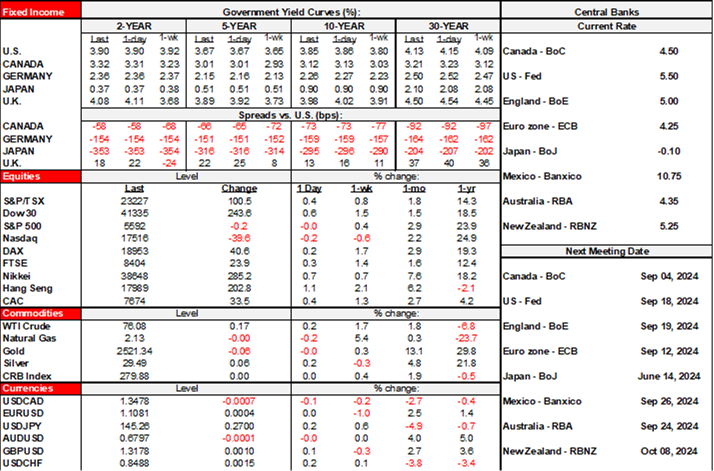

Risk-on sentiment is pushing equities gently higher, Brent just over US$80, and little change across global bond yields. That might change into the N.A. session pending significant macro risk.

A wave of developments will make US and Canadian market participants work for their money ahead of the long weekend and Canada’s early bond close. Key data out of the US and Canada should reveal muted core inflation in the US and strong consumption, plus mixed Canadian GDP figures for June, July, and Q2 overall that should paint a resilience picture.

All of this follows overnight developments that saw Japanese core inflation surge as markets shook off Eurozone inflation that hid ongoing warning signs in keeping with ECB Executive Board Member Schnabel’s relatively hawkish warnings. If that’s not enough, then market participants may also have to contend with potential month-end rebalancing effects.

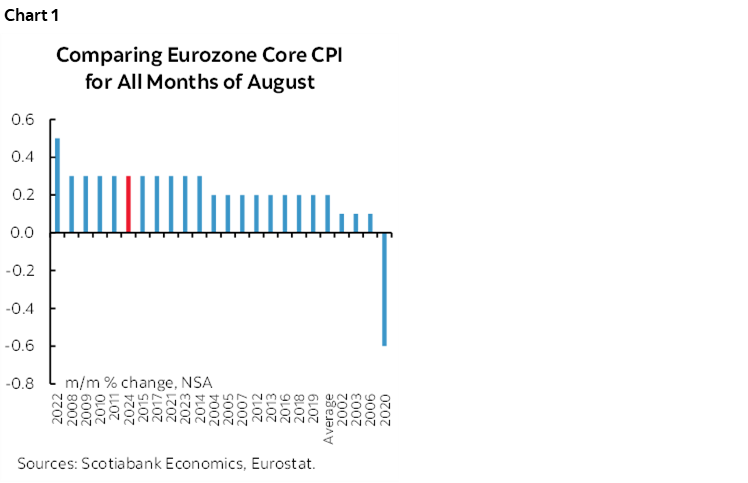

EUROZONE CORE INFLATION REMAINS WARMER THAN USUAL

Eurozone inflation readings were not terribly impactful to markets in part because the figures were generally in line with consensus expectations and because yesterday’s German and Spanish readings had already primed the market and driven a mild bull steepener in Eurozone yield curves.

Count me an ongoing skeptic toward Eurozone inflation getting on track toward the ECB’s targets in light of the latest numbers. Eurozone core inflation registered a slightly above-average seasonally unadjusted gain in August over July compared to like months of August in history (chart 1). It was up 0.3% m/m NSA compared to 0.2% as the average for the month over time. This extends what has been the general pattern throughout this year and serves as a caution to the ECB.

The year-over-year rate of core inflation slipped a tick to 2.8%. Much of the deceleration in this reading from a peak of 5.7% y/y in 2023 has been due to year-ago base effects.

As for headline inflation, it fell four-tenths to 2.2% y/y in August. That is just barely the lowest y/y inflation rate since mid-2021. Year-ago base effects and energy effects dominate as drivers of this cooling rate.

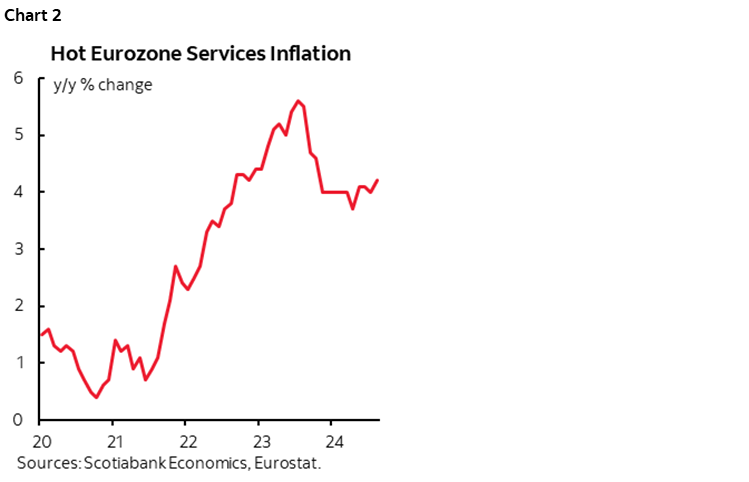

Services inflation picked up by two-tenths to 4.2% y/y and remains uncomfortably high (chart 2). Service prices were up by 0.4% m/m NSA which is double the long run average across like months of August. Services inflation remains hot in keeping with prior momentum, with a likely incremental boost from the Paris Olympics last month.

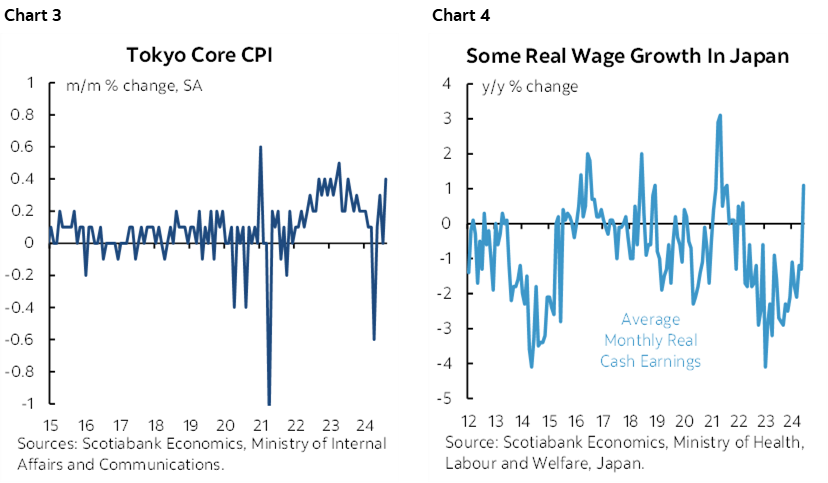

TOKYO CORE INFLATION SURGED, POSING RISK TO THE CARRY TRADE

Japan saw inflation accelerate in the freshest Tokyo measures for August. Key is the core gauge ex-food and energy as it was up by 0.4% m/m SA for the hottest reading since July of last year (chart 3). At an annualized rate this works out to 4.9%. Such pressure at the margin helped to boost the y/y headline rate from 2.2% to 2.6%. This hot core reading coincides with the earlier release that showed real wage growth has suddenly turned positive in y/y terms (chart 4).

And yet the yen depreciated a touch overnight. That may have been partly due to the fact that other macro indicators disappointed. Retail sales were up by 0.2% m/m in July, or half the consensus estimate. Industrial output rebounded from the prior -4.2% m/m drop by less than expected (+2.8% m/m, consensus 3.5%). The jobless rate ticked up two-tenths to 2.7% versus consensus that was unchanged.

Still, the stronger core inflation and real wage measures will likely further embolden the BoJ to tighten monetary policy subject to timing uncertainty and in sensitive fashion to market developments around the carry trade as officials have noted.

SOUTH KOREA’S WON FELT NO LOVE OVERNIGHT

South Korea’s currency won no prizes from traders overnight. The won is the worst performing cross to the USD partly due to the large drop in industrial output (-3.6% m/m, -0.6% consensus) during July.

On tap into the N.A. session are important readings out of both the US and Canada.

CANADA’S RESILIENT ECONOMY

Canada updates a wave of GDP reports at 8:30amET. I’ve estimated flat June GDP with downside risk in light of data we’ve received since Statcan issued its preliminary ‘flash’ reading of 0.1% at the end of July. I wouldn’t be surprised to see a strong gain in July, however, given tracking of various readings including a 1% m/m surge in hours worked. Q2 GDP overall is expected to grow by 1.8% q/q SAAR. A solid July number combined with a soft end to Q2 could bake in solid momentum into Q3 and perhaps support the BoC’s July MPR forecast for a strong 2.8% Q3 GDP growth rate. See the Global Week Ahead here for more colour but otherwise let’s just see the numbers shortly.

Canada’s bond market shuts early at 1pmET today ahead of the Labour Day weekend on both sides of the border.

US TO POST STRONG CONSUMPTION, SOFT CORE INFLATION

The US simultaneously releases July figures for consumption, incomes, and inflation using the Fed’s preferred readings (8:30amET). A modest gain in incomes of around 0.2% m/m SA is expected to be exceeded by a strong gain in nominal consumer spending (0.5% m/m SA consensus, 0.7% Scotia) in part based on what we already know about retail sales that month plus an expected decent gain in services spending.

Key, however, will be the core PCE inflation reading. I went with 0.2% m/m SA based on the earlier core CPI figures and how they translate into PCE’s different methodology. It’s unclear how yesterday’s mild downward revision to Q2 core PCE inflation to 2.8% q/q SAAR instead of the earlier 2.9% figure may impact expectations for July since we don’t know how the downward revision in Q2 impacted the monthly figures.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.