ON DECK FOR THURSDAY, AUGUST 29

KEY POINTS:

- EGBs outperforming as inflation reinforces ECB cuts

- Inflation was weaker than expected across German states, Spain

- Markets shake off Nvidia’s earnings

- Canada’s bank earnings season drove wide divergences in relative performance

- US Q2 GDP, PCE revisions are expected to be minor

- Canada updates lagging payrolls…

- ...as wage measures remain hot

The dominant factor driving markets this morning is soft Eurozone inflation data for August. Otherwise, we’re left with light developments.

EUROZONE INFLATION TRACKING SOFTER THAN EXPECTED

Eurozone rates rallied when inflation data across individual German states hit at 4amET. The headline inflation readings were lower by -0.1% m/m to -0.3% across all of the states. Consensus had expected the national reading to be released at 8amET to land flat.

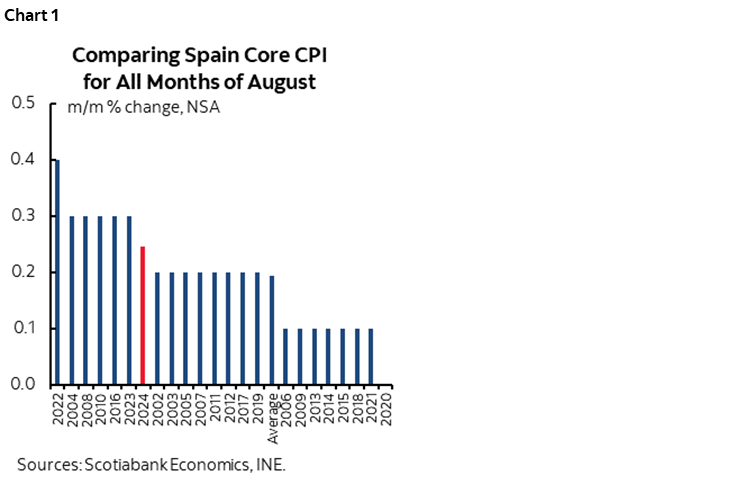

On top of that, Spanish CPI arrived one hour before the German figures and was flat (consensus 0.2% m/m). Spanish core inflation was 0.24% m/m NSA which is close to being seasonally normal for August (chart 1).

This is the last round of inflation data before the ECB’s next decision. There is still risk into tomorrow’s Eurozone-wide tallies that will be further informed by French and Italian figures.

As a result, EGBs are bull steepening with 2-year yields down by 4–5bps this morning. The euro is slightly depreciating and underperforming all other major crosses to the USD. Pricing for the ECB’s decision on September 12th reaffirmed expectations for a quarter point cut and added a couple more basis points to year-end pricing for almost -75bps of cuts over the three remaining meetings this year. There was little spillover on this side of the pond as the US two-year yield slipped only by 1–2bps after the German states released.

VOLATILE TECH EARNINGS SHAKEN OFF

Nvidia earnings are having a negligible impact on markets as the volatile share price is partially rebounding so far this morning from the after-market sell off. EPS was stronger than expected as earnings were robust and stock buybacks increased, but revenue guidance wasn’t quite as impressive as expected. Trade fact over fiction I say; if the pattern is earnings beats to conservative guidance, why not hair cut the guidance?

CANADA’S DIVERGENT BANK EARNINGS SEASON

CIBC pushed the beat score for the overall big bank earnings season to 4–2 with its earnings release this morning. EPS of C$1.93 smashed consensus expectations for $1.74, revenues also beat, and a share buyback plan was announced. That makes for strong beats by CIBC, National and RBC, a mild beat by BNS, and misses by BMO and TD.

On tap into the N.A. session will be the German national CPI print (8amET) and light US and Canadian data.

US REVISION RISK TO GDP, PCE

No revisions are expected to Q2 US GDP that was 2.8% q/q SAAR and core PCE that was 2.9% q/q SAAR (8:30amET) but this second swing at the numbers could carry surprises. Weekly claims (8:30amET) and pending home sales (10amET) are also due.

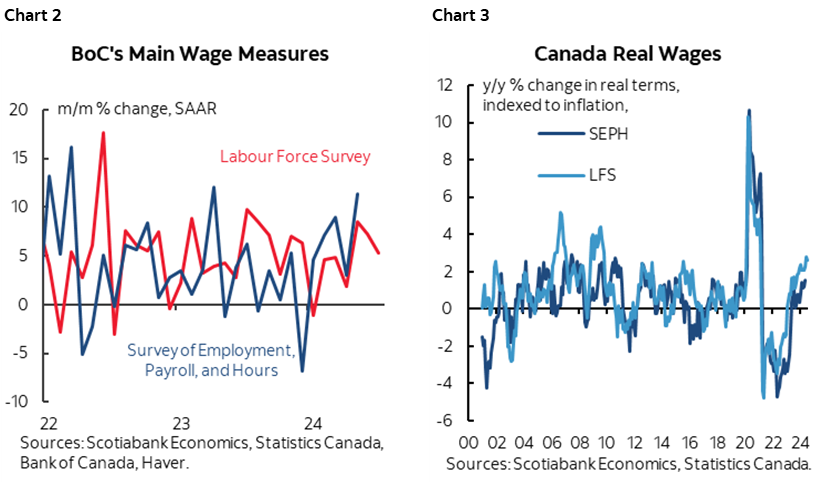

CANADA TO UPDATE LAGGING PAYROLLS, FOCUS ON WAGES

Canada only considers lagging payrolls to June (8:30amET) whereas next Friday’s LFS figures for August will be more important, though after the BoC’s communications on Wednesday. One thing to watch in this morning’s payrolls report, however, will be wages. Chart 2 shows that nominal wage growth remains hot in Canada as measured by m/m SAAR changes to the wages of permanent employees drawn from the fresher household survey and by m/m SAAR changes to average weekly earnings drawn from the SEPH report. Chart 3 shows that both wage measures are accelerating in y/y inflation-adjusted terms on the combination of solid nominal gains and falling inflation. Against the view that these are lagging measures is the fact that Canada faces ongoing rounds of collective bargaining wage resets that are tracking at 3%+ over future years and with many more expiring agreements still ahead that have not filtered into the LFS or SEPH surveys.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.