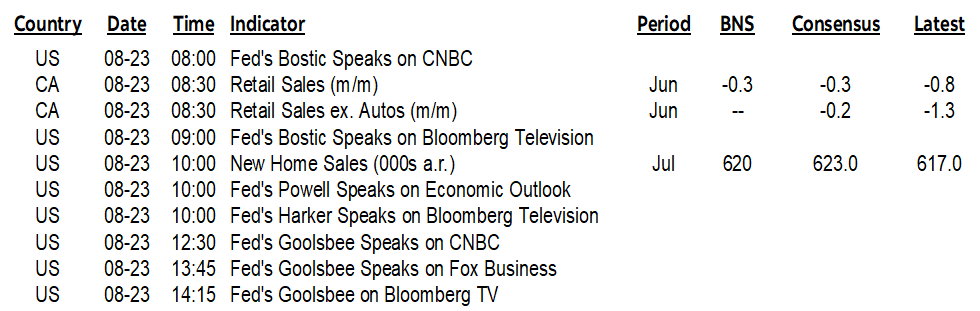

| ON DECK FOR FRIDAY, AUGUST 23 |

KEY POINTS:

- Jackson Hole, Jackson Hole, Jackson Hole.

- Powell’s speech is unlikely to sound dovish enough to what’s already priced

- BoE’s Bailey to follow Powell

- Canadian retail sales to partially inform the state of the Canadian consumer

- BoJ’s Ueda put on his best Teflon suit overnight

- ECB’s inflation expectations hold firm

Jackson Hole, Jackson Hole, Jackson Hole. That’s about all you need to know about the rest of the week. Light overnight developments didn’t do much to sway market sentiment and won’t matter at all in a few hours time. The dollar is broadly softer into it all, US Ts are flat, and global equities are gently higher.

JACKSON HOLE AGENDA REVEALS NO MATERIAL SURPRISES

The JH agenda was released last night and did not reveal much beyond the star power appearances of Powell (10amET) and Bailey (11amET) that we already knew. The only other central bankers slated to speak appear on the last panel on Saturday and include the Governors of Norges Bank and the Bank of Brazil plus the ECB’s Chief Economist Philip Lane. The rest are academics who may have useful insights but won’t be of direct relevance from a policy and markets standpoint. The theme this year is “Reassessing the Effectiveness and Transmission of Monetary Policy.”

POWELL’S SPEECH TO REAFFIRM SEPTEMBER CUT, EMPLOY ‘GRADUAL’ MESSAGING

Chair Powell’s economic outlook speech will be at 10amET. No Q&A or press conference. Watch it at live <go> on Bloomberg and/or with backup at YouTube here either through your work (if permissioned) or personal devices: https://www.youtube.com/KansasCityFed.

I expect Powell to use some variation of ‘soon’ to further reinforce cut expectations in September which seems like a slam dunk after his July 31st presser, FOMC minutes, and other Fed-speak.

I don’t expect much guidance thereafter and there will be no further opportunity to press him for more such as repeated nagging questions about size and pace. His speech may be peppered with references to “gradual” and “measured” while repeating the risks of being too restrictive for too long versus prematurely easing too rapidly. He’ll refer to the ongoing rebalancing of the US economy away from excess demand for labour and ongoing progress toward lower inflation. He will want a balanced message, pointing to resilience and ongoing strength of the US economy while gaining ‘greater confidence’ toward achieving dual mandate goals in a soft landing.

Yet absolutely nothing is screaming out for a 50 move that could backfire especially since, given once, the market tendency would be to pile on and price another large cut and that’s likely too much for Powell’s comfort. What’s currently priced to year-end is probably too much for them barring market dysfunction (not just price discovery) or a severe deterioration in the data.

Watch for a lot of other talk from the sidelines at Jackson Hole with only a few Fed speakers formally scheduled but I’m sure the media hordes will be jamming their mics in front of many others throughout the event into the weekend.

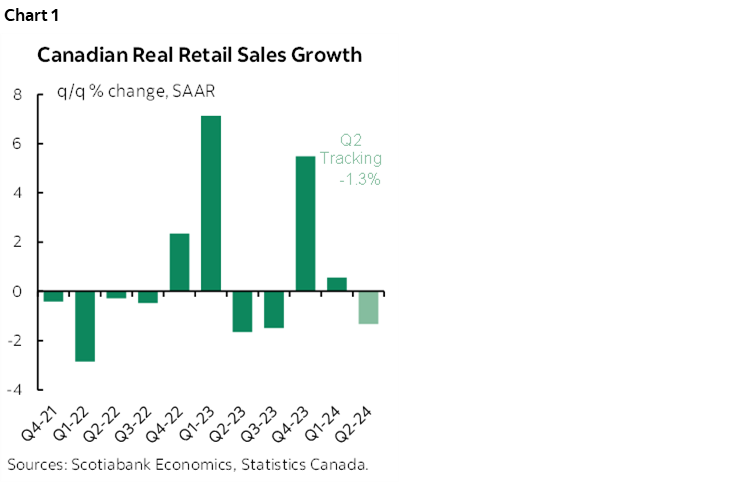

CANADIAN RETAIL SALES TO PARTIALLY INFORM THE STATE OF THE CANADIAN CONSUMER

Canadian retail sales get updated for June and July this morning (8:30amET) and might offer some local market effects at least until any market spillover from whatever Powell says arrives. Statcan previously guided that June’s nominal sales were down -0.3% m/m SA, but the early estimate is only based on half the sample of responses and is often subject to significant revisions. Also watch June details like volumes and breadth. We’ll also get the first glimpse at July with their preliminary flash reading but only for nominal sales. The figures are unlikely to have much of an effect on monthly GDP given the low weight in the production/income-based GDP accounts, but I’ll firm that up after the numbers ahead of next Friday’s GDP accounts.

Since retail sales in Canada only measure goods they only capture less than half of total consumer spending with the rest made up by an assortment of services. As such, whatever the numbers may be, bear in mind that a fuller perspective on the state of the consumer will arrive next Friday in the Q2 GDP accounts and in tracking alt-data for Q3.

BOJ’S UEDA SLOPES OFF RESPONSIBIILITY

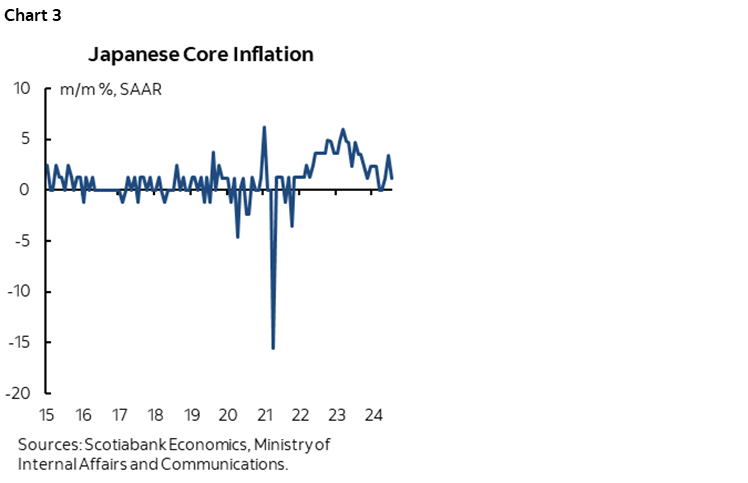

There were overnight comments by BoJ Governor Ueda that indicated further policy tightening could well remain on track and that downplayed the BoJ’s role in driving global market turmoil earlier this month. You wouldn’t expect anything else but a Teflon stance on the latter issue as he pointed the finger at the other guy (uncertainty over the outlook for the U.S. economy) while absolving himself of any responsibility for carry trade turmoil. There’s always a very fine line between central banker and politician. There wasn’t much reaction by the yen or across JGBs to his policy bias in part perhaps because he checked it by indicating there was no rush to further tighten policy as they wish to monitor financial markets for the time being. The overnight release of national inflation figures largely reaffirmed the signal from the earlier release of the Tokyo gauge; core inflation ebbed at the margin (chart 3).

MINOR DATA

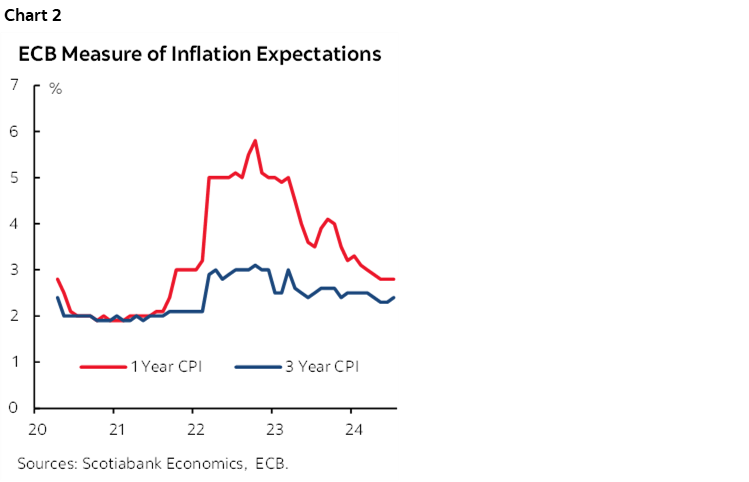

ECB 1- and 3-year CPI inflation expectations were firm in July. The 1-year measure held unchanged at 2.8% y/y and the 3-year measure ticked higher to 2.4%. The random consensus guesses are so sparsely populated for these measures as to be useless.

And fwiw (not much) US new home sales will be updated for July right as Powell’s speech is delivered.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.