ON DECK FOR THURSDAY, AUGUST 22

KEY POINTS:

- Markets are passing the time ahead of Powell’s speech tomorrow

- Powell is unlikely to be a 50bps kind of central banker…

- ...which merits paying overpriced Fed meetings

- Global PMIs signal quicker growth

- Euro area negotiated wages reinforce already priced ECB cut in September

- Canada’s rail strike intensifies pressures on global supply chains

- BoK holds, signals movement toward cutting

- NOK underperforms after soft GDP

- Jackson Hole agenda due tonight

- A distorted start to Canada’s bank earnings season

- Light US data on tap

Still waiting. For Powell at Jackson Hole that is. In the meantime, markets are toiling away, digesting data that in the grander scheme of things is of lesser to no consequence. Sovereign bonds are mildly cheaper across major markets after mixed overnight data and after the FOMC minutes said nothing to surprise what was already priced for the September FOMC meeting anyway.

PAY OVERPRICED FED MEETINGS

Some of this morning’s bond cheapening could be a partial and more cautious rebalancing of positioning into Powell on the expectation that he’s really only going to further tee-up an already priced September cut with a possible “likely” or “soon” reference that the Committee supported in the July minutes. He’s unlikely to say much else beyond noting greater confidence and more progress toward achieving dual mandate goals. Still, he’ll balance that with the same messages on not wishing to be too restrictive for too long versus history’s cautions against loosening too rapidly and prematurely. “Gradual” and “data dependent” and “measured” are all likely key words as opposed to anything that would have markets thinking he’s leaning toward a quicker pace. In my opinion, given information we have to date, September is worth paying as it’s overpricing odds of a half point cut that could backfire if delivered. So is the 100bps+ priced over the three remaining meetings this year which implies one of them would be a 50bps move.

I don’t see Powell suddenly abandoning all the talk in favour of a measured, careful, data dependent and gradual approach by suddenly adopting an accelerated pace. Doing so could backfire from a negative signalling standpoint that says to markets that the Fed’s worried. It would also require fully abandoning references to history’s cautions against loosening too rapidly and prematurely. The US economy remains in net excess demand measured by output gaps. We’ve had plenty of three-month soft patches for core inflation during the pandemic era and seen what happens afterward when folks get carried away. Supply chains are deteriorating once again. I think a sudden sharp deterioration in key data and/or significant market dysfunction (not just price discovery) would be needed to up the pace of cuts.

And remember: Powell wants evidence and doesn’t so much trust forecasts. Those forecasts and models severely let him down in serial fashion over the years. So did his own judgement though as a seasoned central banker—or economist or market participant—is supposed to know when to impose judgement over models that are rooted in the past amid serial out-of-sample shocks.

All of this might be why we have the new KC Fed President Schmid saying this morning that he wants more data before supporting a September cut. He doesn’t vote this year and commences voting next year, and clearly he’s an outlier relative to what yesterday’s minutes revealed.

CANADA’S RAIL STRIKE ADDS TO DETERIORATING GLOBAL SUPPLY CHAIN

One note of caution is that supply chains are blowing up ahead of Powell. Canada’s railways shut down overnight and with that will be ripple effects across N.A. especially given uncertainty toward potential strikes at US ports and given soaring global shipping costs driven by avoidance of the Red Sea and Suez Canal. Some of these shocks could be transitory (strikes, though of uncertain length and magnitude) and some longer-lived (geopolitical) but they risk feeding off of one another at an inopportune moment for sectors like agriculture and retail orders for the holiday shopping season. If I’m Powell, I’m thinking tread carefully on just a three-month soft patch when we’ve seen plenty of them throughout the pandemic era.

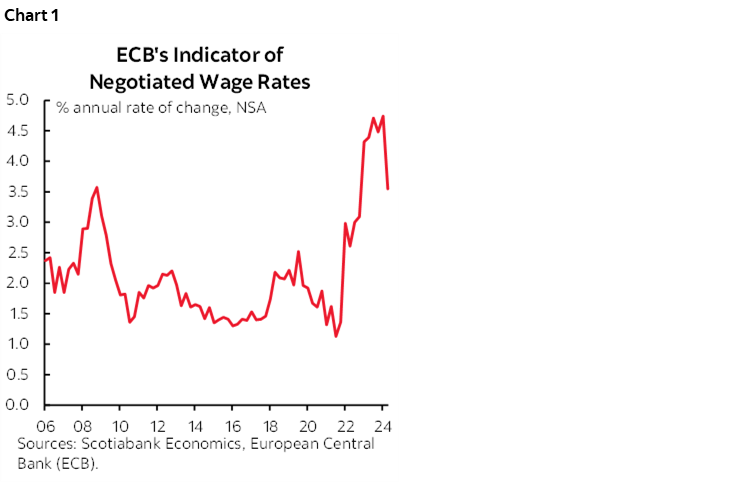

EURO-AREA NEGOTIATED WAGE GROWTH DECELERATES

The ECB’s Q2 measure of negotiated wages posted the slowest—but not slow—gain in six quarters but merits caution when interpreting it. It was up by 3.5% y/y, down from 4.7% in Q1 (chart 1). It reinforces already priced expectations for a 25bps ECB rate cut next month. Still, the concentration of collective bargaining efforts into the start of the year, the role of year-ago base effects driven by the accelerated trend at the start of last year, and the fact it’s just one data point should drive caution when interpreting the figures especially in light of so many expiring agreements that are still ahead.

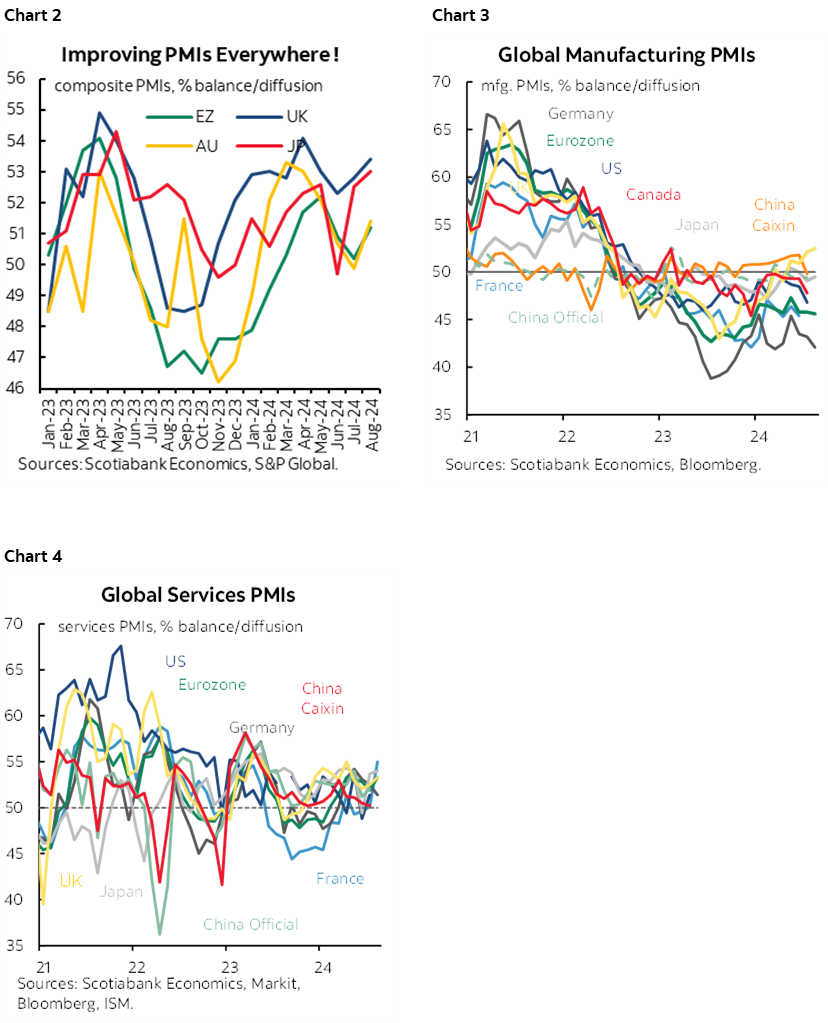

GLOBAL PMIS SIGNAL QUICKER GROWTH

Global PMIs moved higher everywhere (charts 2–4). Given their correlations with quarterly GDP growth they suggest that the global economy gained a little momentum as late summer unfolded. Composite PMIs are in expansion territory everywhere except for Germany’s troubled economy. In some cases we can pin the gains on transitory factors like the impact of the Paris Olympics on France’s readings, but there are correlated positive gains across other markets that appear to be more broadly based.

- Australia: The composite PMI moved up by 1.5 points to 51.4 and hence into above-50 expansion territory after temporary slipping in July. The rise was mostly driven by services with a smaller contribution from manufacturing.

- Japan: The composite PMI edged up a half point to 53 with small contributions from both services and manufacturing.

- India: The composite PMI was little changed at 60.5, down two-tenths as an up-tick in services to 60.4 was offset by a two-tenths dip in manufacturing to 57.9, both of which remain strong readings.

- Eurozone: The composite PMI climbed a full point to 51.2 entirely on the back of a higher services reading that jumped 1.4 points to 53.3. France’s composite PMI jumped 2.8 points higher to 52.7 and was led by about a five-point jump in the services PMI to 55 as manufacturing fell by about two points and hence further into sub-50 contraction at 42.1. Germany’s composite PMI fell to 48.5 and is therefore contracting faster with decelerations in both services (51.4, 52.5 prior) and manufacturing (42.1, 43.2 prior).

- UK: The composite PMI increased 0.6 points to 53.4 mostly due to a higher services reading but manufacturing was also up.

- The US S&P PMIs arrive later this morning (9:45amET).

BOK HOLDS, TEES UP CUT BIAS

The Bank of Korea stayed on hold with a base rate of 3.5% as widely expected. Its policy bias turned toward a more dovish stance by following up “greater confidence that inflation will converge on the target level” with how it will “examine the proper timing of rate cuts while maintaining a restrictive monetary policy stance.” That may tee up a rate cut as soon as the next meeting on October 11th.

CANADA’S BANK EARNINGS SEASON COMMENCES WITH A HEAD FAKE

Canada’s quarterly bank earnings season got off to a soft start as TD missed expectations with Q3 EPS of C$2.05 ($2.07 consensus) alongside a mess of AML litigation and other issues. The rest including Scotia will arrive next week. TD isn't likely to be representative of the broader group, but never wag a finger at a challenged competitor as today’s extraordinarily complex world of banking has c-suites on constant alert toward nasty surprises.

NOK WEAKENS ON GDP MISS

Norges Bank watchers took down a slightly softer than expected Q2 GDP report that continues to indicate a stalling economy. GDP was up 0.1% q/q SA nonannualized (0.2% consensus) and the prior quarter was revised down a tick to 0.1%. Very little trend growth has been posted since the start of last year. NOK is underperforming a touch.

LIGHT US DATA ON TAP AHEAD OF JACKSON HOLE AGENDA

Other light US data will include jobless claims (8:30amET) and existing home sales (10amET). Hopefully we don’t have to phone to get those numbers after yesterday’s mess (reminder). I remain deeply concerned about uneven access to key US data after several mishaps and the fact that some Wall Street economists seem ok with that. That’s not the hallmark of a trustworthy capital market.

We’ll get the full agenda to the Fed’s annual Jackson Hole symposium tonight at 8pmET at the KC Fed’s website. It will reveal other global central bank officials who are scheduled to speak (we know Bailey goes right after Powell) plus academics etc.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.