| ON DECK FOR WEDNESDAY, AUGUST 21 |

KEY POINTS:

- Fed watchers have their eyes on the jobs part of the dual mandate this morning

- US payrolls may misstate job growth for many reasons…

- …one of which may be informed by annual benchmarking revisions this morning…

- …that are usually overhyped and typically a futile waste of time trying to predict

- FOMC minutes: Stale, and poised to be superseded by Jackson Hole

- Canada’s rail strike is part of a hat trick of coalescing supply chain shocks…

- …that may force Trudeau/Singh/Freeland to change their tune on getting involved

- The rail strike’s potential effects on Canada’s labour force survey

The main focus could be preliminary annual revisions to US payrolls this morning while FOMC minutes are likely to be of passing interest. There was little else of interest overnight. I’ll also write about how Canada’s looming rail strike must be viewed in a global supply chain context that is souring at the worst possible time for many industries.

US PAYROLL REVISIONS—ANOTHER TEMPEST IN A TEAPOT?

Have—or more likely, by how much—US nonfarm payrolls been overestimating US job growth? There could be many reasons for believing as much and only one of those reasons may be further informed today.

One reason payrolls could be overestimating job growth that will not be informed today is whether SA factors are appropriate; I argued in my August nonfarm payrolls report that July’s reported payroll growth was lowballed due to lower SA adjustments than may be appropriate and that by corollary payrolls earlier in the year were likely overestimated for similar reasons.

Other reasons for why nonfarm payrolls may over estimate job growth include the fact they exclude businesses without formal payrolls—like many small businesses—that may be better captured in the household survey, and nonfarm counts multiple job holders versus the household survey that counts employed bodies only once. So, if you’re unemployed this month and next month you get 3 part-time jobs, nonfarm counts you three times versus once in the household survey.

But the question of whether nonfarm payrolls are overestimating job growth that will be informed today comes through benchmarking revisions (10amET). US payrolls are subject to benchmarking revisions twice a year, once in August and then the final revisions the following February. These are separate from regular rolling revisions that are offered two-months at a time and that we get with each payrolls report. You’ll see the revisions to the level of nonfarm payrolls as at March 2024 at this link when they are out today (2023 is currently populated). The level revisions are then proportionately distributed to give you an average monthly revision to previously reported growth in payrolls.

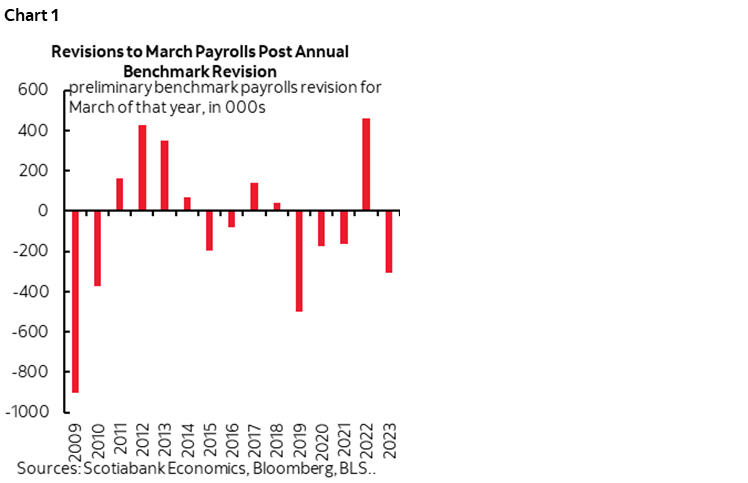

Chart 1 shows the magnitude of past revisions to the level of nonfarm payrolls in March of each year via this annual exercise dating back to 2009 and hence covering the GFC and pandemic periods. The biggest downward revision was –902,000 in 2009 for understandable reasons given the magnitude and uncertainty of the shock. The biggest upward revision was +462k in 2022 as the economy recovered from serial shutdowns in the depths of the pandemic. The average annual revision over this fifteen year period was –71k. When any of these past revisions are converted to a monthly equivalent the effect tends to be pretty modest on initially reported monthly changes to nonfarm payrolls.

Various shops have penciled in a range from around 300k to 1 million for an expected downward revision this time. I’ll explain why they’re wasting their time trying to devise estimates in the rest of what follows.

The purpose of today’s revisions is to try to reconcile what nonfarm payrolls say about employment against what state-level data says using the Quarterly Census of Employment and Wages (QCEW) report that is drawn from unemployment insurance tax filings by establishments at the state level. The payroll revisions frequently move lower each year during the benchmarking exercise, but the question is always by how much.

What usually happens is that the hype around lofty estimates of potential revisions drawn up by the street—and subject to very wide brackets—gives way to relatively modest revisions. I’ve seen this time and again.

It’s next to impossible to try to estimate the revisions ahead of time and frankly folks who have been through this rodeo enough times know better than to waste much time trying. One reason for this is that we do not have the QCEWS data for Q1 as of yet and that’s what the nonfarm payrolls revisions are going to be benchmarked against. That Q2 QCEW estimate arrives just before the nonfarm revisions tomorrow morning. Economists at the Philly Fed try to provide early benchmarks for the Q1 QCEW that in fact do go up to April of this year, but they’re just estimates using yet other sources.

Another reason why estimating the payroll revisions through the benchmark exercise is difficult is that we’re trying to estimate revisions to payrolls by using QCEW data that itself can be wildly revised each quarter that it gets released and revised back in time. For instance, when we get the first Q1 estimate of QCEW data tomorrow morning it will include revisions to prior quarters that will affect the levels into Q1 themselves. If on top of that you use the Philly Fed’s early benchmarks for QCEW then that too gets revised for the Q1 figures as well as incorporating revisions to QCEW in prior quarters.

So, after all of that, in plain English, you’re trying to forecast revisions to nonfarm payrolls based on other data sources that are incomplete and that can be wildly revised themselves when they do become complete. That point often gets lost with shops that try to make big splashes with their payroll revision guesstimates.

Furthermore, we’re comparing aardvarks to orangutans when using QCEW data to estimate revisions to payrolls. That’s because payrolls use a birth-death model to compensate for the fact that nonfarm only captures current establishments and hence to compensate for sample bias, whereas this model is not applied by QCEW data. Ergo, you’re mixing methodologies when trying to use one source (QCEW) to predict revisions to the other (nonfarm payrolls). A side debate is always whether the birth-death model is appropriately applied and sure as sugar someone always tries to discredit every single nonfarm payrolls report by critiquing the b-d adjustments.

All of which is to say phooey on it all, it’s all just one big futile exercise as enjoyable as sticking bamboo shoots up your fingernails to try to estimate the revisions and so let’s just see what they turn out to be an assess accordingly. See ya at 10amET for that.

The reason why markets are focused upon this is two-fold. For one, it’s August, and other than Jackson Hole, market participants have little else to ponder. For another, the FOMC is ticking the box on reasons to begin easing in light of the recent trend toward lower core inflation and because the labour market has become more balanced away from high excess demand for workers. Supply chain shocks noted later in this note are among the reasons for Powell to tread very carefully on Friday. In my opinion, it would take a massive downside revision to reported growth in nonfarm payrolls to matter to them relative to momentum across their publicly stated views and relative to what’s priced. Furthermore, expect Powell to continue to point to many measures of the labour market and not just nonfarm payrolls.

FOMC MINUTES—STALE AND TO BE SUPERSEDED BY JACKSON HOLE

Minutes to the July 30th–31st FOMC meeting (2pmET) are likely to reinforce the Committee’s openness to a rate cut in September, but they will be partly stale on arrival and also quickly superseded by Chair Powell’s speech at Jackson Hole on Friday morning at 10amET. Recall that during the July 31st presser, Powell said:

“If we were to see inflation moving down, growth remains reasonably strong and the labour market remains similar to its current condition, then a rate cut could be on the table in September. If inflation disappoints then we would weigh that along with the other things. It's going to be the totality of the data and risks."

What happened since then is that yes indeed, core CPI did continue to move lower, landing at 0.2% m/m SA in July and slipped below 3% y/y. Data probably makes their discussion a bit dated.

CANADA’S RAIL STRIKE IS ONLY ONE OF THREE SUPPLY CHAIN SHOCKS

Canada will update producer prices for July (8:30amET). They tend to garner little attention. The raw materials index is just a reflection of already known changes to commodity prices. The industrial product index is more revealing but significantly reflects known swings in the terms of trade including via changes in the currency.

There is a bigger issue at hand when it comes to talking about risks to b2b and b2c inflation. It has to do with a hat trick of potential supply chain shocks. One of them is a domestic issue, one could arise in the US in the relatively near-term, and the other is causing turmoil across global shipping channels. The only positive development across supply chains is that the effects of an historic drought that crippled the Panama Canal this year appears to be waning with guidance pointing toward normal operating conditions expected to start next month.

It’s unfortunate timing to add on a Canadian CN/CP rail strike because of a confluence of emerging potential supply chain shocks that could be highly disruptive. The timing couldn’t be worse as farmers are entering harvest season and retailers are ordering Fall/Winter lines and for the holiday shopping season. On top of it all, there is a very pro-union Federal government in Canada that has no desire to interfere – although they may be forced to change their stance one way or the other. I have no idea how long a strike could be, but with both sides saying they are far apart and given the noted context, I’d be pleasantly surprised if it’s a short disruption.

Key is that the Canadian rail strike is not occurring in a bubble. Potential looming strikes at US ports are an added complication facing supply chains. From what I understand, the deadline for negotiations involving the International Longshoremen's Association is October 1st. Maybe a potential (likely) Canadian rail strike will be over only to go into problems at US ports again.

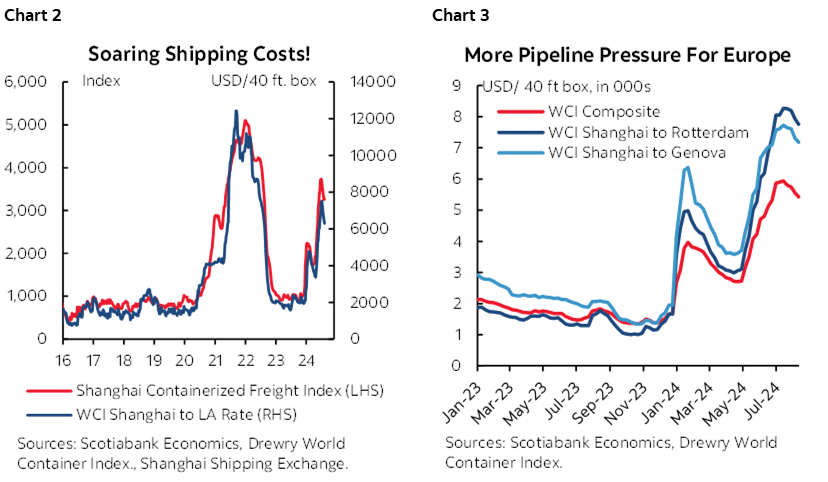

These two developments are set against soaring global shipping costs (charts 2, 3). Iran and its proxies have everyone avoiding transit around the Red Sea and Suez Canal and opting instead for much longer and costlier routes such as around the Cape of Good Hope that tie up containers, creating scarcity and driving costs higher. Another ship was taken over in the Red Sea overnight which continues the bias toward avoiding the area. Someone has to pay for those costs whether it be shareholders through tighter margins, consumers and other businesses through higher prices, or both plus others such as suppliers, workers, and governments.

A lengthy rail strike in Canada set against global supply chain challenges could carry highly disruptive effects over coming weeks and months. With an election year looming, the Trudeau-Singh-Freeland government may be forced into sacrificing its pro-union stance by intervening.

As an aside, how might a rail strike impact data? It’s a clear risk to inflationary pressures particularly when combined with the other points made above. It’s a downside risk to August GDP that will arrive in September and, depending upon the duration of the strike, could be an ongoing downside for September GDP. But what about the job market and hence the Canadian Labour Force Survey?

1. There will be no (or very minimal) effect on the August LFS numbers that we get on September 6th. That's because the LFS reference week is the week that includes the 15th day of each month which in this case was last week. They are not on strike yet, but the rail cos and suppliers have been preparing for a strike and so there could be minor effects across affected sectors. I’m not clear ono the extent to which strike preparations last week could have impacted the LFS reference week but think they’ll be small.

2. The strike would have to persist through the week of September 15th in order to have a directly disruptive effect on the jobs report. An indirect effect is feasible, however, if hiring intentions suffer and delay planned hiring because of strike uncertainty and its effects across multiple sectors.

3. If the strike were to persist into the September LFS reference week for the numbers we'll get in early October, then the direct impact would probably be more through hours than jobs. The rail workers wouldn't count as unemployed while on strike as they have the reasonable expectation of returning to work as long as the household survey properly measures their responses. There would be indirect negative effects on employment elsewhere. As for hours worked, if 9,300 workers are on strike into the Sept LFS reference week then the direct effect could be about -0.1% m/m SA on aggregate hours as a mild downside risk to GDP all else (never) equal. If the strikes severely disrupt sectors from autos to agriculture and retail etc then the indirect effects could dominate and bracketed assumptions could get to be quite large.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.