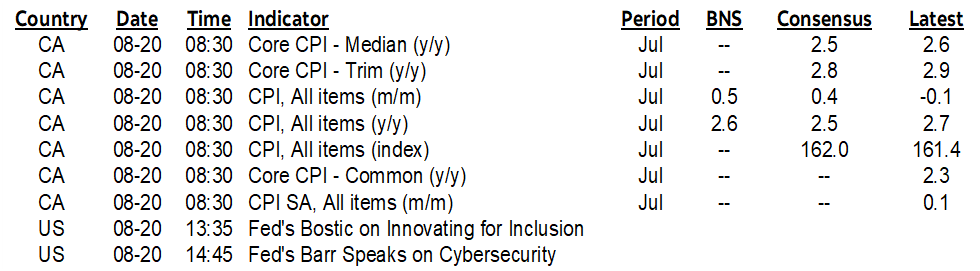

| ON DECK FOR TUESDAY, AUGUST 20 |

KEY POINTS:

- Global markets tread water before Jackson Hole

- Canadian core inflation: was the Jan–April soft patch transitory…

- …or was it the reacceleration over May and June that was transitory?

- Sweden’s Riksbank cuts, guides potentially less cutting than priced

- Hawkish bias to RBA minutes drives higher Australian yields

- NZ curve catches spillover effects from Australia…

- …as government overhaul of carbon credits drives higher carbon prices, passthrough

Overnight developments were light and focused on Australia, NZ, and Sweden and perhaps Japan. Global markets are generally little changed with Jackson Hole the focal point. Canadian inflation may spice up the local market.

Riksbank Cuts, Signals Market Pricing is a Ceiling

Sweden’s Riksbank cut its policy rate by 25bps as widely anticipated, but the statement guided that “If the inflation outlook remains the same, the policy rate can be cut two or three more times this year.” Markets were pricing three more cuts this year in addition to the cut that was just delivered, and so “two or three” guidance was a bias toward possibly less than is priced. The krone appreciated a touch and the rates curve was little changed overnight.

Hawkish RBA Minutes Drive Higher Yields

RBA minutes to the August meeting drove mild cheapening across the Australian and Kiwi curves overnight. The minutes had a hawkish tone and stated a bias toward “holding the cash target steady at its current level for a longer period than currently implied by market pricing may be sufficient to return inflation to target in a reasonable timeframe.” Note the emphasis on tighter than is priced. A hold for an “extended period” was guided while emphasizing a higher risk of not achieving the 2–3% inflation target within a reasonable period of time. There was a considerable amount of time spent discussing a rate hike during the meeting. Markets retained pricing for a quarter point rate cut by year-end and the A$ was little changed while yields pushed 3–4bps higher across most of the Aussie curve.

NZ Rates Feed Off RBA, Government’s Carbon Overhaul

The NZ rates curve and kiwi dollar may have also been influenced by auction announcements and by the NZ government’s overhaul of carbon trading. The government announced that it would halve the number of credits next year and that drove carbon prices up by 7% overnight to the highest since March. Mild, temporary pass through effects could ensue.

There were also headlines out of Japan overnight but they didn’t materially impact JGBs or the yen. A research paper by BoJ economists argued that inflation risk is still supported by shifting business pricing behaviour and wage setting exercises which may continue to lean toward further policy tightening. The views expressed by staff do not necessarily align with the leadership.

Canadian Inflation

But the main focus this morning will be upon Canadian inflation figures for July (8:30amET). There may also be casual interest in the oddly delayed release of the BoC’s latest Senior Loan Officer Survey (here) that showed that mortgage lending conditions slightly eased in Q2 while non-mortgage consumer lending conditions continued to tighten and so did business lending conditions. The survey is skewed toward responses into the end of Q2.

A combination of seasonal pressures, slight positive contribution from gas prices, and an expected bounce back from some of the soft components in the prior month—like the 10% weight on lower prices for the rec/reading/education category that includes multiple leisure activities—are behind my 0.5% m/m NSA headline estimate alongside persistent shelter pressures.

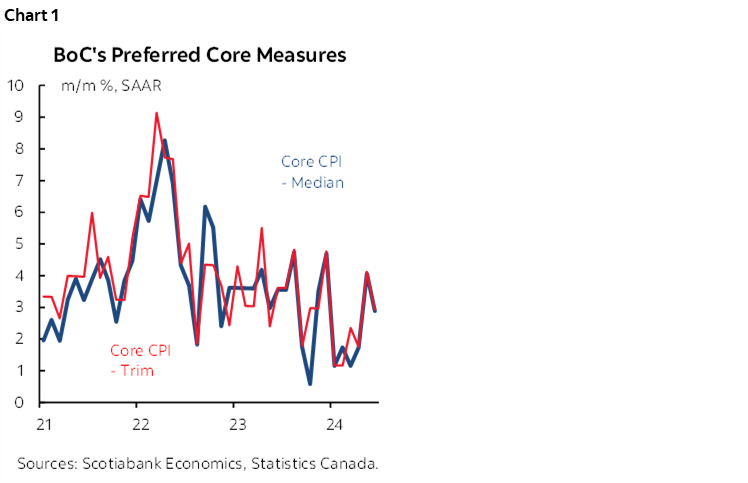

Key, however, will be the core trimmed mean and weighted median CPI measures. Those core CPI measures have been spiking higher over the past two months with the BoC’s two main preferred readings both landing at 4.1% m/m SAAR in May and 2.9% in June (chart 1).

That observation leans against the consensus narrative that focuses only upon falling y/y headline inflation without respecting the evidence on core price behaviour at the margin. The BoC targets headline CPI over the medium-term but uses the core gauges to operationalize achievement of this mandate which is why core inflation matters. Ergo, hot readings for core measures at the margin would give them reason to be more careful if they persistently move away from the four-month soft patch that we had earlier this year.

And so the debate that remains intact is whether that four-month inflation soft patch was temporarily driven by weather (El Nino effects on categories like clothing and travel) plus quasi-regulated prices under political pressure into the Federal Budget (like telecommunications, groceries), or whether it was the past two months of accelerating m/m core gauges that were driven by temporary factors. Only more data will settle the debate, but I still find that there remain ample reasons to be concerned about upside risk to inflation.

Those factors include ongoing fiscal policy stimulus to growth that may intensify into an election year, excessive immigration into severe housing shortages, nominal wage growth and accelerating real wage gains that continue to run at absurdly strong rates compared to tumbling productivity, and my skepticism toward the BoC’s fudged arguments for potential growth in a still resilient economy.

Will today’s inflation figures matter apart from perhaps driving short-term August market volatility? The BoC is on a straight-line path toward delivering a material amount of easing with a high bar set for being knocked off course. Where that straight line may eventually pause is uncertain, but -50bps to date is no circuit breaker relative to the communicated reaction function. So, a cool reading makes another cut on September 4th a slam dunk. If another hot set of m/m SAAR core readings makes it three in a row, then it should still leave a rate cut possible but the decision may be accompanied by a more circumspect and cautious policy bias thereafter.

Please see the Global Week Ahead for more.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.