ON DECK FOR FRIDAY, AUGUST 2

KEY POINTS:

- Risk appetite enters Friday on its back foot

- What’s driving markets? It’s complicated!

- Nonfarm payrolls preview

Nonfarm payrolls (preview below) could make or break risk sentiment that is wrong footed so far this morning.

A combination of factors is driving equities lower with snps down by 1%, Nasdaq futures down by a little more, European cash markets lower by about ½% to about 1½% and following a weak Asian overnight session led by about a 6% drop in Japanese equities. The yen keeps charging higher as it is now below 149 to the buck. You won’t be surprised to hear that sovereign bonds are rallying, but not by that much with US Treasury yields down by 3–4bps alongside single digit basis point declines across EGB yields. Oil is up a few dimes again as energy markets watch and wait to see how Iran and its proxies may escalate the conflict in the Middle East.

WHAT’S CAUSING MARKET MOVES?

What’s driving negative sentiment in equities and lower bond yields? It’s complicated.

It’s August. Chill.

For one thing, always be careful toward month-end effects into thinning August volumes and liquidity. As PMs and other market professionals enter peak summer vacation periods in N.A. and Europe, they may well be playing it safer on their positions. You’d think we would all know better by now than to overreact to volatility around this time of year.

Exaggerated Tech Optimism Being Reined In

Mostly negative earnings from big US tech firms in yesterday’s after-market are also clearly driving some of the negative sentiment perhaps having more to do with how exaggerated the tech craze and AI sentiment had become. The market is also differentiating between winners and losers in tech, and may also be behaving in short-sighted fashion by looking only at the bottom line and ignoring investment surges that drove some of it and that could pay off handsomely over time.

Even on a personal level, do I really want to pay double for an AI laptop compared to a very good regular one when at present—and for probably quite a while yet—the benefits are either miniscule in a practical sense or downright absent? Do I really want to pay $2k+ for a new iphone when as near as I can tell the benefits are extraordinarily marginal?

Cherry-Picking US Macro Data

Fear of US payrolls may be behind some of the sentiment in the broader context of what’s happening with the US economy. On that note, there is cherry-picking of US data.

ISM-manufacturing reflects a small 10% direct share of US GDP and yet its decline sparked concern toward the health of the US economy while ignoring that its sentiment-based production gauge is misaligned with actual hard data on manufacturing output in the Federal Reserve’s figures for industrial production. We’ll see about next week’s ISM-services that is expected to rebound and that reflects a much bigger share of the modern US economy than manufacturing.

Markets ignored the lift to US productivity and soft unit labour costs yesterday despite their contribution toward a disinflationary backdrop for constructive Fed easing. They also ignored the solid gain in US vehicle sales despite being smaller than industry guidance.

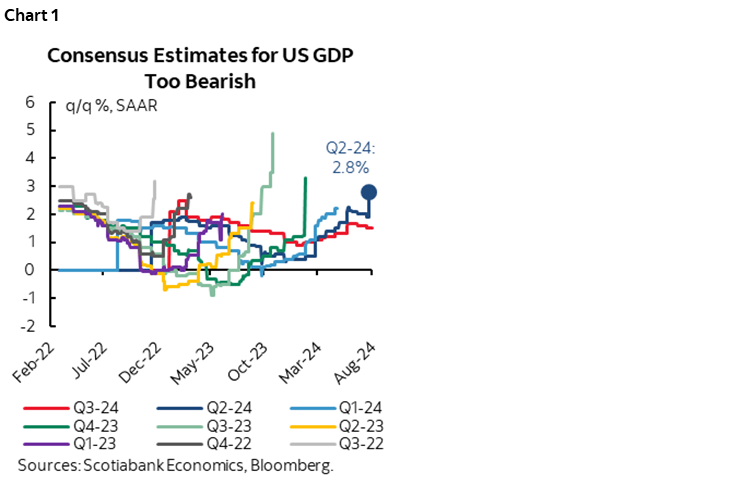

They are also ignoring solid—but highly tentative—nowcasts for Q3 US GDP on the heels of 2.8% q/q SAAR Q2 GDP growth. This is not an economy tracking a recession versus a soft landing. Markets have assumed a recession lies right around the corner and economists have under-predicted growth in the US economy for ages now and been wrong in serial fashion while spending each quarter chasing the numbers higher over and over again (chart 1).

The US Treasury Curve in Finally Waking Up to Fed Easing

And on rates, the US curve is coming back into alignment toward something more reasonable but with still some way to go in narrowing spreads over other global benchmarks. I’ve long argued that the US front-end is too cheap unless neutral rate estimates are off by massive amounts. The Treasury curve should be rallying as Fed easing comes into clearer sight. The first round spillover effects are putting downward pressure on yields elsewhere such as Canada, but it’s debatable whether this will persist as the Canada curve is getting very richly priced in 5s.

The BoJ’s Questionable Moves

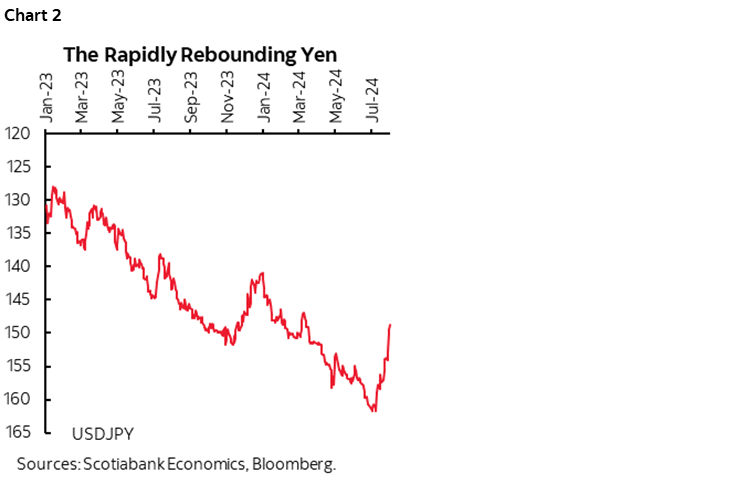

The BoJ’s tightening combined with the Fed providing clear signals that it is moving toward easing are disrupting the carry trade for now, but I’m still not convinced that the BoJ knows what it’s doing and it has a history of zigging when others are zagging. For now, the effects on the yen (chart 2) are hitting the Nikkei hard given its 15$ drop from the all-time high on July 10th that corresponded to the peak weakness in the yen when it was pushing toward 162. The Nikkei is taking out this overshooting of risk appetite that should have never happened in the first place as it was predicated upon the assumption that the yen’s fall would persist and build further.

Geopolitical Effects

We also clearly cannot dismiss geopolitical risk as markets watch rising tensions in the Middle East, and yet far more often than not this is not usually a durable weight against risk appetite.

US Election Volatility

There could also be a repricing of US election effects, assuming markets have the foggiest idea of how to do that. That’s likely to continue for quite a while.

NONFARM PAYROLLS PREVIEW

The breakeven rate for payrolls is just north of 200k in order to keep pace with the pick-up in population growth, although that’s subject to the extent to which all of the population surge is assumed to be equally employable and counted in the numbers. Consensus expects a number that on the surface looks a touch softer than that for payrolls, but that falls well within the statistical noise bands. All estimates within consensus are within such confidence interval bands despite the hubris around how one person’s estimate is better than another’s; let’s just see the figures folks.

How markets may react is unclear; a strong number could be a good news is bad news effect in terms of rate cut pricing, while a weak number could be taken as a bad signal for the economy even if it strengthens the easing case. With market sentiment where it is at this moment, it could be a case of tails I win, heads you lose. I mean that both a strong number (that leans against a rush to ease) and a weak number (that feeds concern about the economy and the Fed being slow) could be taken negatively by risk appetite, making the best scenario a plodding down-the-middle reading.

If it’s a soft number, then it will also depend upon why in terms of considerations like breadth, the degree of substitution between hours and bodies etc. If it’s just a Hurricane Beryl effect howsoever small, then walk it off as the impact will be temporary. Challenger layoffs were very low last month and fell, so this could offset the storm effect.

- Scotia: 205k

- Median: 175k

- Mean: 175k (so no skewness)

- Range: Most estimates range from about 150k to 220k

- Std dev: 23.5k

- Confidence interval: +/- 130k

- Whisper number: 170k

- UR: 4.1% median, tails skewed to 4%

- Wages: 0.3% m/m SA Scotia and consensus

Among the mixed drivers pieced together from other labour market readings are the following, bearing in mind that how nonfarm behaves often bears little resemblance to other indicators:

- consumer confidence ‘jobs plentiful’ slipped

- NFIB small business jobs ‘hard to fill’ increased

- NFIB small business hiring was stable at a higher three-month moving average than earlier in the year

- ISM-mfrg employment fell by about 6 points

- we won’t get the more important ISM-services employment gauge until next week

- ADP private payrolls were up by only 122k but offer poor tracking to nonfarm’s private payrolls component

- Challenger layoffs fell to about 26k, or about half the prior month’s layoff tally and the lowest in a year

- initial jobless claims were little changed between the June and July reference periods

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.