ON DECK FOR THURSDAY, AUGUST 1

KEY POINTS:

- Fed’s more balanced dual mandate focus shifts emphasis to tomorrow’s payrolls

- The BoE’s oddly apologetic cut

- Oil markets on tenterhooks pending Iranian retaliation

- One chart explains Trump’s increased nuttiness

- US layoffs hit the lowest level in a year

- Two of three LatAm central banks hold

- US to report mild productivity gain…

- …possible up-tick in ISM-mfrg and strong vehicle sales

- High US tech earnings risk in the after-market

The month-end transition is being greeted by more central bank decisions, high earnings risk, and potential event risk. The yen continues to appreciate in the aftermath of the BoJ and the Fed and is slightly below 150. Gilts are outperforming while sterling is the weakest cross to the USD entirely due to positioning before the BoE’s apologetic rate cut as UK markets were largely unchanged after the announcements perhaps given the weak guidance. Oil markets remain tense given developments in the Middle East with prices up by about ¾%. Just as this note is being published there appears to have been a multi-country prisoner swap involved Russia that released US hostages which is great, at least until we find out what terrorists were handed back to Russia.

Oil Still Gaining on Middle East Tensions

Reports that Iran is planning a retaliatory strike against Israel may take shape at any point. Israel reported overnight that it killed the #2 leader within Hamas about a couple of weeks ago. Oil is up another ¾%. It’s not clear if Iran will simply seek to save face with a relatively harmless measure like the last time when they fired off a bunch of wildly inaccurate missiles that got shot down, or something that further escalates tensions.

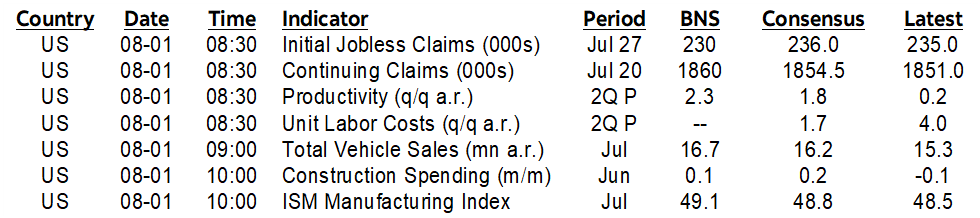

One Chart Explains Trump’s Crazy Remarks

Want to know why Trump is sounding increasingly unglued even by his own standards? Check out chart 1 and the evolution of various measures of Kamala Harris winning the US election. I don’t believe that markets are capable of forming well informed views on the potential consequences to either candidate winning the election, but fwiw, the S&P500 has largely moved sideways over the past month in which Trump’s odds have fallen while Treasury yields have also fallen over this period including the two-year measure as confidence in Fed easing has risen.

Bank of England Shows No Confidence in Cutting

The Bank of England delivered the least confident sounding initial rate cut imaginable. The MPC reduced Bank Rate by 25bps to 5% in line with most within consensus including shifting estimates at the last minute. The tight vote of 5 in favour of cutting and 4 against doesn’t signal high confidence behind the action. Nor does the accompanying statement here. The overall tone of the communications almost reads like “we’re cutting, sorry about that mate!” Among the five who voted for the cut, guidance noted that “For some of these members, the decision was finely balanced. Inflationary persistence had not yet conclusively dissipated, and there remained some upside risks to the outlook.” Thus, even the cutters lacked conviction.

If the BoE is truly data dependent, then they would have held, as m/m core CPI pressures remain high and so does m/m wage growth while GDP growth is solid. As near as I can tell, the case for a cut was based on a) the ‘finely balanced’ remark in June as a reaction function signal, b) the forecast belief that inflation will return to target despite past weaknesses of the BoE’s forecasting models.

Two out of Three LatAm Central Banks Hold

Last evening’s decisions by two more LatAm central banks were mixed. Brazil held its selic rate unchanged at 10.5% as widely expected. Chile also unanimously held at 5.75% against 16 out of 20 within consensus who thought it would cut, but BCCh’s forward guidance pointed to the resumption of cuts going forward. This follows BanRep’s widely expected decision to cut 50bps at the same time as the FOMC statement arrived yesterday.

US Data Risk—Mild Productivity, Up-Tick in ISM, Strong Vehicle Sales

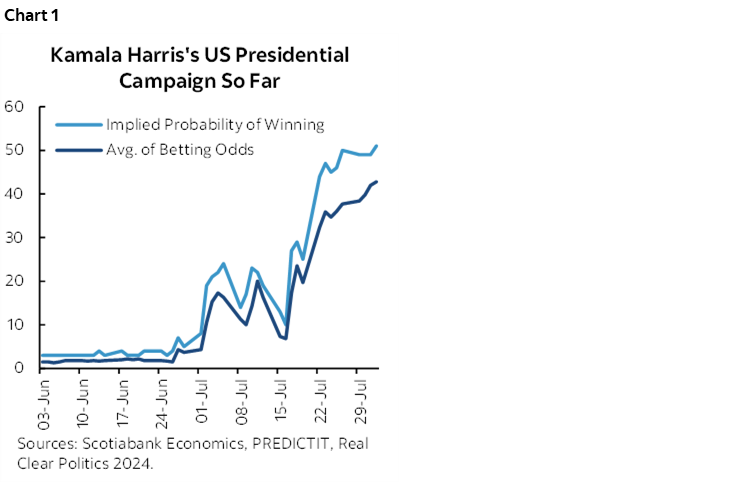

More US labour market teasers lie in store plus ISM-manufacturing, but tomorrow’s nonfarm payrolls and tech earnings are the dominant considerations to end the week. Challenger job cuts fell back to 25,885 in July from about 49k the prior month and extended the steady downward trend from 90k in March (chart 2). It’s the lowest reading for US job cuts in a year. This is a positive signal for tomorrow’s nonfarm payrolls, but only a small one given the small change in cuts month-to-month and because it says nothing about the hiring side of the picture.

Q2 productivity is expected to grow by 1.8% q/q (Scotia 2.3%) and that could drive softer growth in unit labour costs than the prior quarter (8:30amET). Weekly jobless claims are due at 8:30amET. ISM manufacturing is expected to inch higher for the month of July (10amET). The day could end with strong US vehicle sales during July based on industry guidance with Scotia’s estimate at 16.7 million SAAR from 15.3 the prior month.

High Earnings Risk in the After-Market

Apple, Amazon and Intel release earnings in today’s after-market.

LatAm observers will also have an eye on Chile’s monthly economic growth signal for June that is expected to register a slight gain (8:30amET) and Peru’s inflation reading at 11amET.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.