| ON DECK FOR TUESDAY, APRIL 9 |

KEY POINTS:

- Markets in a holding pattern ahead of the week’s big day

- BoJ jawboning tries to short up the yen, with little success

- US small business less optimistic…

- …while planning to hire less, hike prices more

- Yellen should look in the mirror the next time she lectures China

- Mexican CPI lands a touch softer than expected

- B.C.’s ‘meh’ ratings downgrade

There really is very little to consider this morning as global markets await the big day tomorrow when US CPI, the BoC, FOMC minutes and Chinese inflation all arrive. If anything spices it up today, then it would have to be off-calendar risk and/or positioning into Wednesday.

The BoJ’s Futile Jawboning

The BoJ’s Ueda and the BoJ rumour mill tried to spice up the yen overnight as it continues to trade well north of 150 to the USD. It didn’t have much effect. The usual ‘people familiar with the discussions” indicated that the BoJ may raise its inflation forecasts at its next decision on April 26th. They say it could be because of the Spring wage negotiations, yet the outcome was largely in line with what the BoJ would have anticipated in its last inflation forecast. The more likely culprit for an upward revision in my opinion would be higher oil prices and BoJ research has always said that’s a transitory lift.

Further, Governor Ueda said “We have to consider reducing the degree of monetary easing if the underlying price trend rises along with our outlook. We will carefully consider this at every policy meeting as it depends on incoming data.” I’m not sure how incrementally insightful that is. OIS markets were already priced by about another 20bps of tightening into year-end.

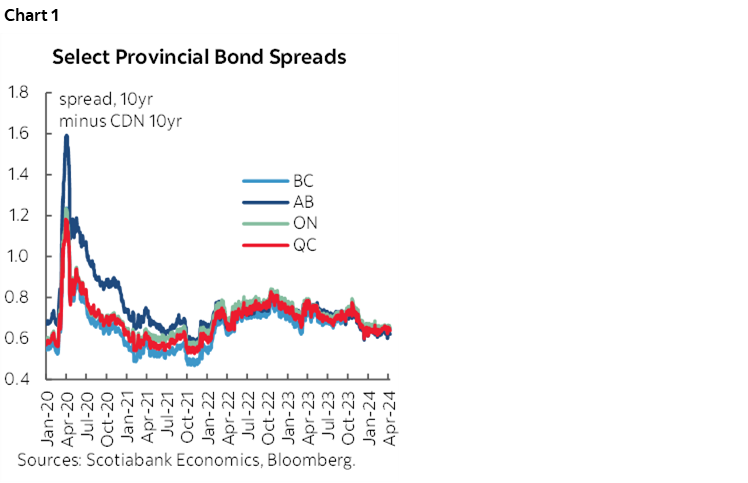

B.C.’s ‘Meh’ Moment

BC’s downgrade from AA- to AA by S&P with a negative outlook late yesterday may continue to be priced with reverberating effects. Meh. Ratings changes usually spark a few wiggles in spreads and then folks walk it off and go back to other more important drivers like the allure of low risk spread pick-up over the sovereign (chart 1). It’s a bit of a blow to the government’s pride and perhaps rather well-timed if the free spending Premier Eby thinks of taking a poke at the BoC’s management of monetary policy tomorrow.

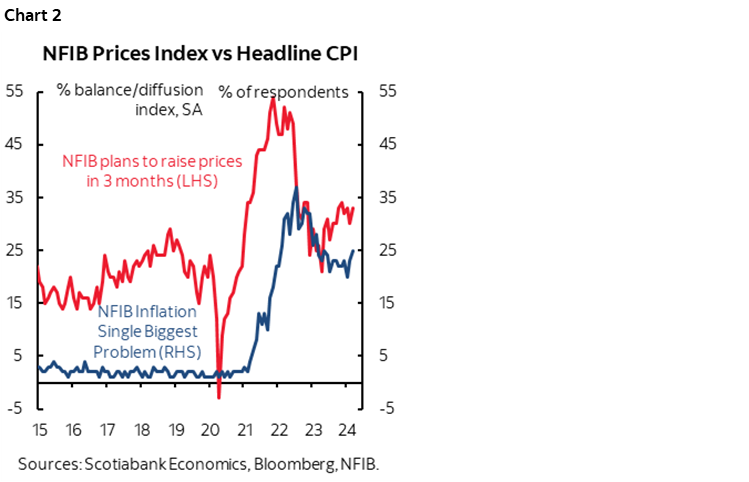

US Small Businesses Are Sending Warning Signs

US small business optimism slipped a touch in March. Inflation was a reason as shown in chart 2. The net percentage of firms planning to raise prices in the next three months edged a little higher to 33 from 30 and the percentage of small businesses saying that inflation is the single biggest problem they face moved up to the highest reading since last May.

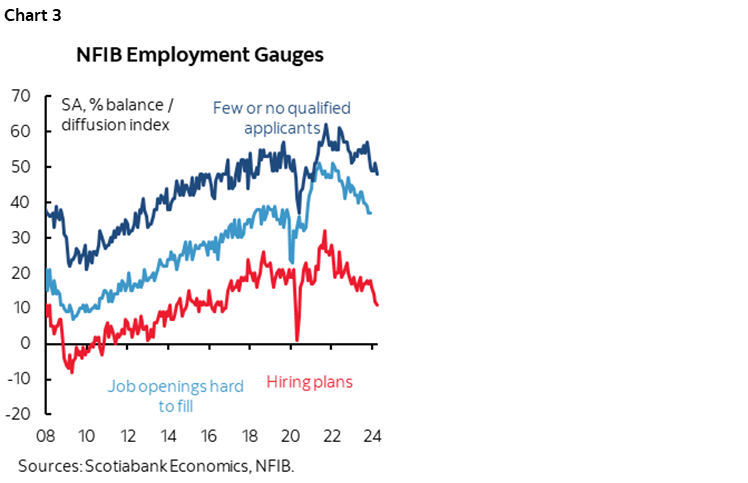

Small business hiring plans edged lower again to the lowest since the pandemic first began to unfold (chart 3). The ‘hard to fill’ measure of job openings also moved to its lowest since early 2021.

Mexican Inflation Lands on the Screws

Mexican CPI was a touch softer than expected at 0.29% m/m (consensus 0.36%). The year-over-year rate held at 4.4% (consensus 4.5%). Core inflation edged down to 0.4% (prior 0.5%, consensus 0.5%) and 4.55% y/y (4.6% prior and consensus).

Yellen’s Lecturing Falls Flat

US Treasury Secretary Yellen’s visit to China is over. Hallelujah. The ostensible purpose of her trip was to wag a finger at China for its aggressive policy goals to expand manufacturing through heavy state support and all of the distortions and complications that brings especially given the deeply intertwined ambitions of the state that go far beyond economics. Good for her. Although it was an obvious ploy in an election year and I hope that she’s as critical of her own administration behind the scenes, but of course she isn’t.

Yellen got about the reception that she deserved in my opinion; warm, respectful, and unlikely to lead to any changes. America isn’t treated the same way it might have once been when it goes about the world wagging its finger and beseeching others to let the free market determine outcomes. We should all view that as rather unfortunate because the world needs a strong example to be set by the US if we think beyond puerile nationalism and think more about what’s good for everyone especially in such a divided world with undemocratic forces.

There is a lot that I like about the US. It’s often a world productivity leader. Its companies are innovative. It has the deepest and most sophisticated capital markets anywhere. But to anyone who thinks beyond backyards and borders, the rest of the world has a justified issue with getting lectured by US administrations who should focus upon reforming themselves first.

And yet America’s own companies receive ginormous subsidies from US taxpayers and benefit from being protected from free market forces (here). The US Farm Bill and Europe’s Common Agricultural Policy are the two biggest trade distortions affecting agriculture for which consumers, taxpayers, and developing country farmers pay dearly; if governments truly care about food prices, then liberalizing trade in agriculture would be a good place to start. The Biden Administration’s curiously named Inflation Reduction Act is just a twisted name for government intervention including billions in subsidies for ‘clean’ stuff. The Biden administration’s heavy spending and debt issuance have contributed to higher term funding costs for everyone. The US routinely bails out a banking system with far too many inefficient and mismanaged small players. The southern states siphon off activity from the northern states and other countries with massive subsidies to manufacturing and other activities. America has turned more isolationist and protectionist under both the Trump and Biden administrations. And let’s not forget that the mismanagement that caused the Global Financial Crisis was then followed by US government and Federal Reserve policies that bailed out one sector after another and left us with the messy aftermath in distorted markets for years to come in a system that is full of moral hazard issues. American government policy entails bailing out just about anyone who stumbles; witness the multiple times its leading Presidential candidate has declared bankruptcy while turning it into an artform.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.