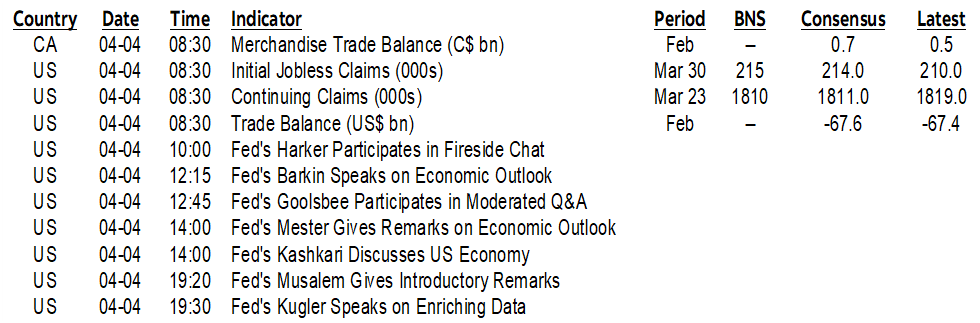

| ON DECK FOR THURSDAY, APRIL 4 |

KEY POINTS:

- Markets in a holding pattern before tomorrow’s US, Canadian jobs

- Powell said nothing new on monetary policy yesterday...

- ...but shoved back against mandate creep

- Soft Swiss core inflation heats up SNB cut bets

- US layoffs, claims on tap; watch for Good Friday distortions

- Canadian trade’s contribution to growth to be updated

- More Fed-speak today

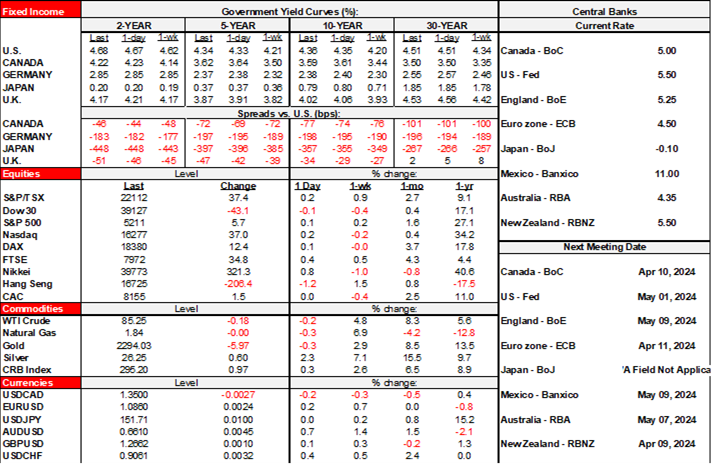

Overnight developments were very light in terms of markets and macro developments. Weaker than expected Swiss CPI reinforced pricing for another SNB cut. Oil prices are flat so far this session. Curves are marked by slight underperformance by US Ts. Equities are mostly higher across global benchmarks.

Powell Said Nothing New

I don’t see notable catalysts for this morning’s market moves and didn’t think Powell said anything new yesterday as his core message remained that they need more data to assess what’s going on with inflation and can take their time before probably cutting later. That’s entirely compatible with the -75bps in the dot plot and the clear skewness toward less in the distribution.

The opportunity was missed to ask Powell questions like how he views the large run-up in oil prices from the standpoint of opportunity to US oil producers versus inflation risk, particularly given somewhat of a rise in some measures of inflation expectations.

Beyond that, the rest of Powell’s short speech just pushed back against mandate creep by telling everyone to stop pressuring the Fed to get involved in determining climate policy, immigration policy, fiscal policy etc. Good for him! His message was that they have enough on their plate and it’s up to elected officials and others to manage the rest. Frankly, given the rather glaring imperfections in how the Fed conducts monetary policy, I wouldn’t want them touching the rest anyway!! It was mildly amusing that he delivered this message before Stanford’s ‘Business, Government and Society Forum’ at its business school that emphasizes a need to focus upon all manner of considerations beyond the business of running a business to its students.

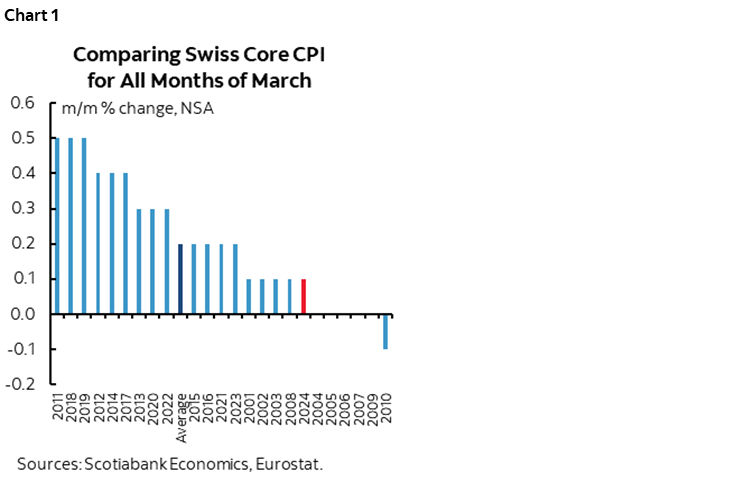

SNB Cut Pricing Heats Up Post-CPI

The Swiss franc depreciated and is the weakest performer to the dollar this morning in the wake of CPI for March. Core inflation landed at just 0.09% m/m NSA which was weaker than a typical month of March (chart 1). That put a little more downward pressure on the y/y rate to 1% from 1.1% previously. Contract pricing for the next SNB meeting on June 20th added a few basis points and is mostly toward another quarter point cut. The overall curve richened by 2–3bps across maturities.

A Pair of US job market Readings

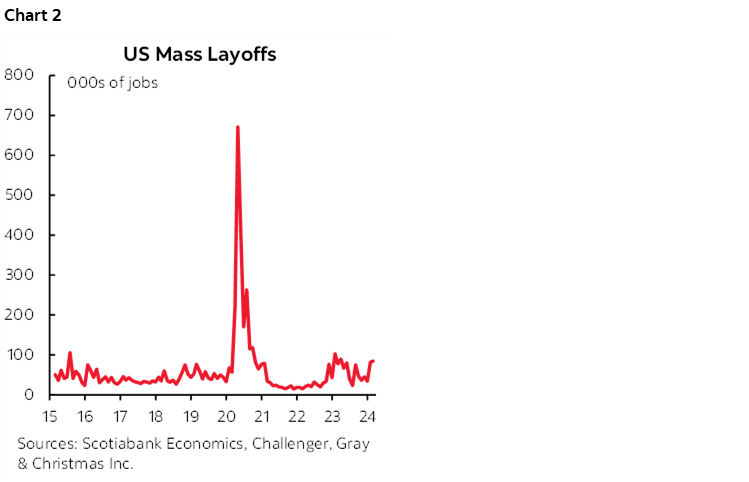

Watch Challenger job cuts (7:30amET) as they have moved up to about 85k per month of late which is still compatible with significant job gains (chart 2). The March reading will help to inform whether the past couple of months increased because of seasonal firings at the beginning of new fiscal years that are not adequately controlled for using standard SAs in light of the pandemic-related hiring binge. We’ll also see if firings were marginally lower because of the earlier GF/Easter holiday and these numbers are not seasonally adjusted.

Weekly claims will fall between nonfarm reference periods and offer no material information to tomorrow’s nonfarm call (8:30amET). Having said that, it's for last week, and so be careful with any potential mischief from the Easter Bunny! Again, Good Friday landed earlier than normal and so that could mess with SA factors by artificially depressing claims given one day less to file them.

Canadian and US trade

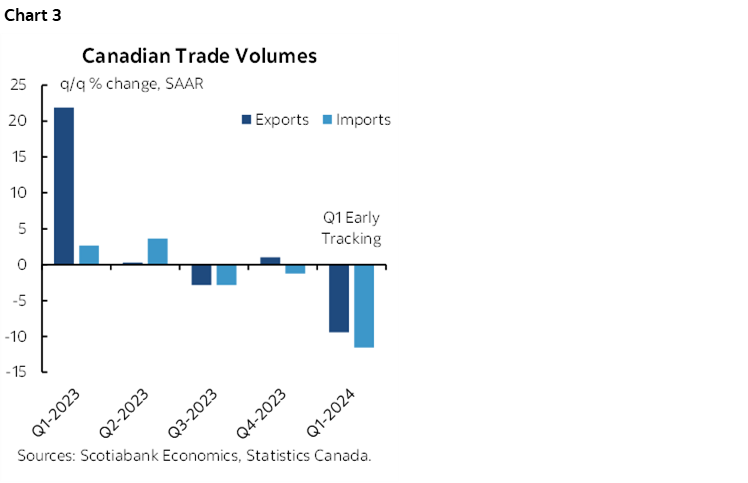

February’s Canadian readings could help to further inform Q1 GDP growth tracking (8:30amET). Net trade is tracking a modest contribution to growth (chart 3), but not for great reasons as import volumes are tracking a slightly bigger decline than export volumes (ie: a net reduction of the import leakage effect from GDP). That’s only based on January and Q4 and so February figures will add to our understanding.

The US trade figures (8:30amET) won’t matter much since we already know that the merchandise deficit widened a little to -US$91.8 from $90.5 billion (barring big revisions) to which a usually stable services balance is added. Fed-speak will continue to drone on. I’m hopeful that some of the regional presidents will push the arguments more than Powell did today. We’ll hear from Philly’s Harker, Richmond’s Barkin, Chicago’s Goolsbee, Cleveland’s Mester and Minneapolis President Kashkari all between about 10am–2pmET.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.