| ON DECK FOR TUESDAY, APRIL 30 |

KEY POINTS:

- Macro risk heats up alongside month-end rebalancing

- Canada’s economy in focus with GDP estimates

- US labour costs are probably still growing strongly

- US consumer confidence still range-bound?

- Mexico’s economy is expected to post no growth

- Eurozone core CPI was among the hotter months of April on record

- The Eurozone’s slight technical recession came to an end in Q1

- China’s PMIs weaken, prompting policy jawboning by officials

- BanRep expected to cut again

- Yen shakes off intervention, resumes weakening

Macro drivers heat up alongside month-end rebalancing as the FOMC begins its two-day meeting. Stocks and bonds both have a mild cheapening bias across countries and benchmarks. The USD is gaining against most majors except the euro and MXN. The yen resumed weakening overnight and is approaching 157 as some of the effects of the prior night’s apparent intervention—seemingly confirmed by BoJ data this morning—were shaken off.

I wouldn’t say that overnight macro releases significantly affected market sentiment, but we’ll see if that rings true into a round of releases across N.A. and with BanRep on tap.

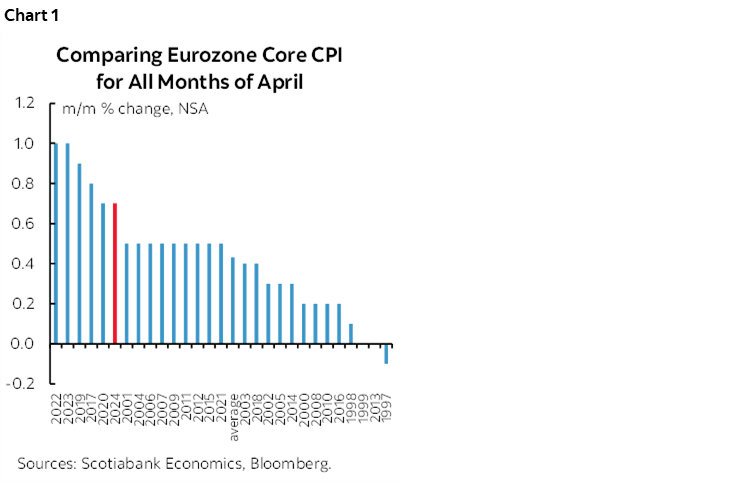

Eurozone core CPI was up by 0.7% m/m NSA in April. That is the fifth strongest reading for a month of April over time (chart 1) which indicates persistent pressure, but was neither here nor there in terms of having little impact on markets or pricing for the June ECB meeting. Year-over-year core CPI ebbed to 2.7% (2.6% consensus, 2.9% prior).

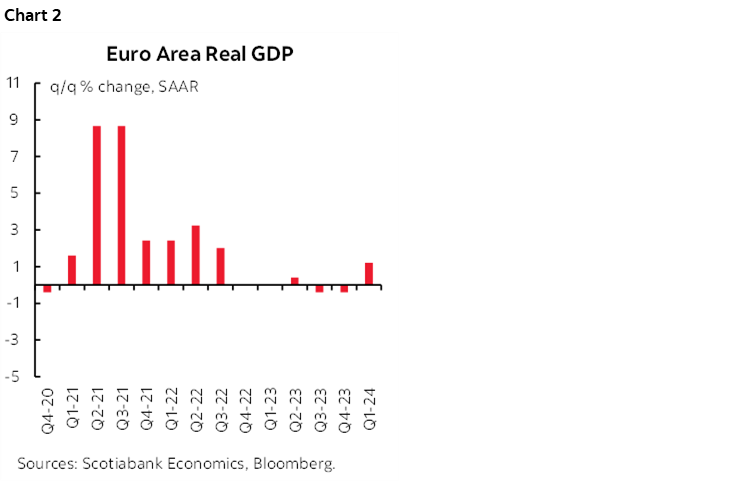

Eurozone GDP growth slightly beat expectations at 0.3% q/q SA nonannualized in Q1. That barely ended the slight technical recession that had been marked by back-to-back -0.1% q/q SA declines over the prior two quarters (chart 2). There are preliminary signs that better momentum into Q2 may be in store as German retail sales volumes and French nominal consumer spending beat expectations for March which offers positive hand-off effects to Q2.

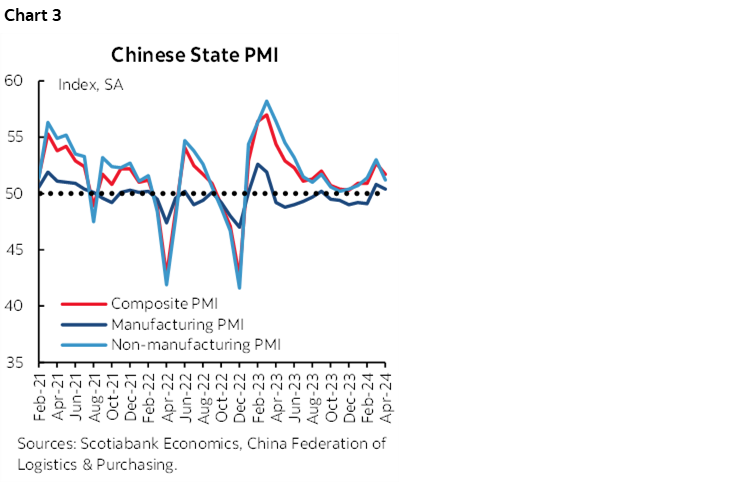

China’s state purchasing managers’ indices fell in April (chart 3). The composite reading slipped by a full point to 51.7 which signals slower overall economic growth. Most of that was due to a deceleration in the non-manufacturing PMI (51.2, 53 prior). Manufacturing continued to hover just above contraction at 50.4, down four-tenths.

China’s Politburo—Chaired by President Xi Jinping—jawboned policy easing options with some interpretations seeing it as teeing up monetary easing using the policy rate and required reserves. That seems a stretch if the Fed is going nowhere as monetary easing by China could destabilize the yuan.

There will be elevated data risk Into the N.A. session:

1. Mexico updates Q1 GDP that is expected to post no growth after barely staying positive in Q4 (8amET).

2. Canada updates GDP with potential revisions to Statcan’s earlier 0.4% m/m SA flash guidance for February and a first glimpse at the estimate for March (8:30amET). See my Global Week Ahead article for more on this and other readings.

3. The US employment cost index is expected to extend the streak of relatively warm readings with another gain of around 1% q/q SA (8:30amET).

4. US consumer confidence is due for an April update (10amET). Repeat sale home prices probably posted another slight gain (9amET).

5. Colombia’s central bank is unanimously expected to cut by another 50bps (2pmET).

Also watch earnings with key being Amazon in the after-market.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.