| ON DECK FOR TUESDAY, APRIL 2 |

KEY POINTS:

- Oil prices spike again, cumulative rise adds to inflation risk

- European markets are mostly just playing catch-up

- German headline inflation lands slightly softer than expected

- Canadian consumers don’t believe in the BoC’s 2% target

- Canada’s painfully slow turnaround on wage settlements is unacceptable

- Calgary’s housing market has no supply, prices spiking

- US to update lagging JOLTS, factory orders

- Banco Central de Chile expected to deliver another mega-cut

- Fed-speak on tap

Europe is catching up to everything that’s happened since last Thursday but otherwise the global market moves are relatively mild on light developments this morning. A small sell off across Eurozone front ends was tamped down after German states released CPI estimates and following updated Eurozone inflation expectations. Absent fresh developments, gilts are underperforming EGBs as they catch up to yesterday’s repricing in the US while ignoring an updated report that indicated softer UK supermarket prices. Today’s incremental developments will be focused upon light US data and another possible mega-cut from Chile.

German inflation was slightly softer than expect last month. CPI was up by 0.4% m/m SA (0.5% consensus) with the EU-harmonized measure up by 0.6% m/m (0.7% consensus). The first hint at this came a few hours earlier this morning when individual German states posted weaker than expected readings with two up by 0.3% m/m SA, three at 0.4% and one at 0.5%.

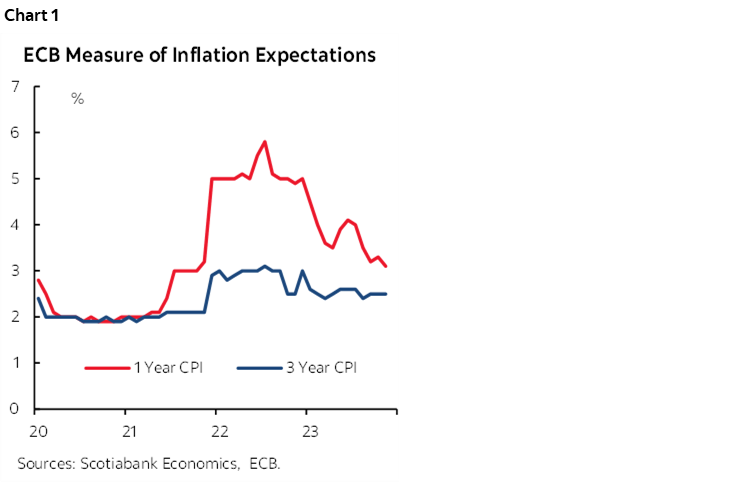

Eurozone inflation expectations remained sticky in February (chart 1). The medium-term 3-year measure was unchanged at 2.5%. The short-term 1-year measure edged a bit lower to 3.1% from 3.3%.

Energy market pass through effects into headline and core measures of inflation are part of the market’s worries. Oil prices are up sharply with WTI and Brent both gaining about 1½%. Middle East tensions are the main driver. WTI is up by about US$16 per barrel since early December. In Canada, WCS is up by over US$20 per barrel over a similar period as it gains from broad oil market developments and a narrowing of the WCS-WTI difference that is being driven by Trans Mountain.

Across the rest of Scotia’s footprint watch for another large cut by Chile’s central bank.

Light US data is also due out. Lagging JOLTS in particular can carry at least a fleeting market response as markets await Friday's payrolls (10amET). Factory orders (10amET) are mostly just expected to follow durables higher. Fed-speak will unfold throughout the middle part of the day with Governor Bowman, NY Fed President Williams, Cleveland’s outgoing Mester and San Fran’s Daly on tap between 10:10amET and 1:30pmET.

Canada is starting to see the first estimates for March existing home sales roll in. Calgary’s biggest problem seems to be a dearth of new listings as months’ supply fell below one month with inventories down by 21.7% y/y. The sales-to-new-listings ratio jumped to 84% for the tightest market since 2006. Prices were up by 10.9% y/y. Days on market fell to 20 which is 24% lower than the same month last year.

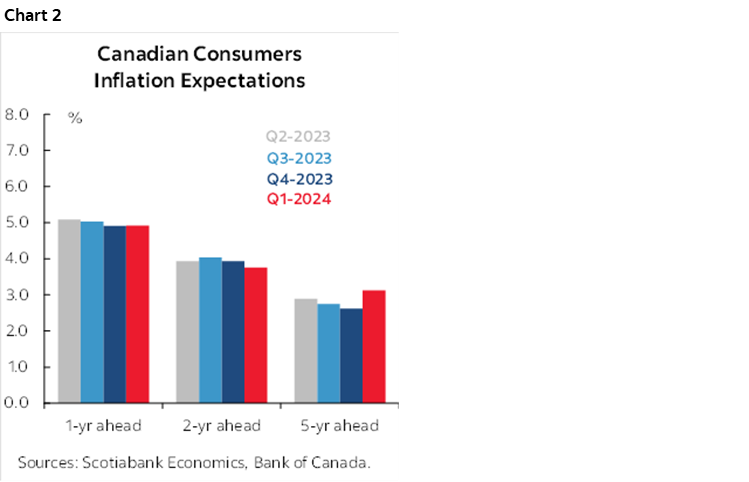

This follows on the heels of yesterday’s Bank of Canada surveys of business and consumer expectations (here, here and here). Governor Macklem has consistently said that expectations and price setting behaviour are on his watch list of key things to monitor. He probably didn’t like what he saw. Here are some observations:

- Consumers: The biggest change was to long-term inflation expectations. Consumers signalled they expect inflation to be 3.1% five years out which is up by half a percentage point since the last quarterly survey (chart 2). We all know that nobody can forecast where inflation will be five years from now, but the signal is that consumers don’t believe in the BoC’s 2% inflation target. That’s evident in wage setting behaviour within the collective bargaining process (more on that below). As for other horizons, consumers’ expectations for inflation over the coming year held unchanged at 4.9% and 2-years out moved marginally lower to 3.8% from 3.9%. Across all horizons, consumers just don’t believe that the BoC will achieve 2%. Of course, you can also have the debate about whether consumers truly understand inflation and how it is measured in any event!

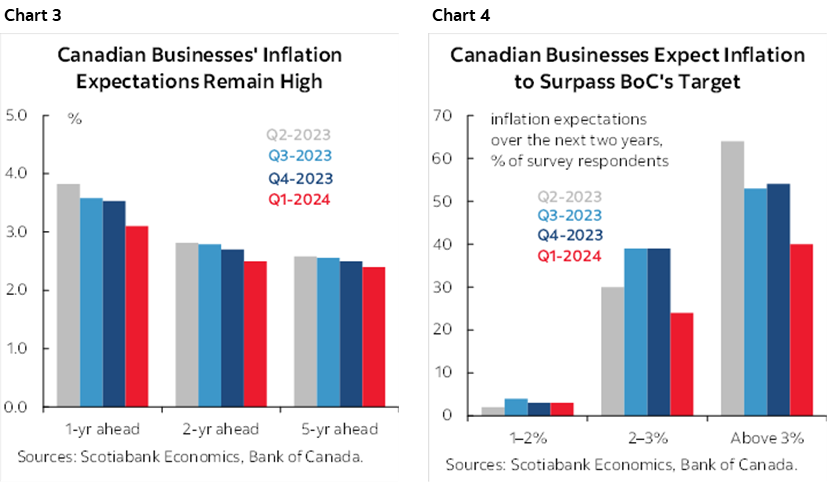

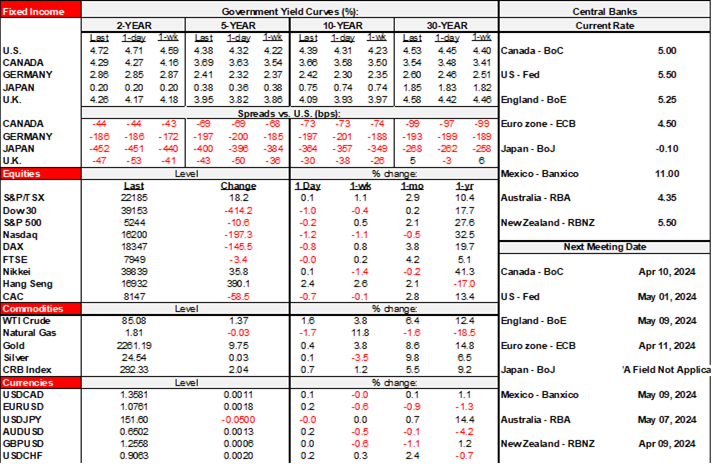

- Businesses: It’s a little better in terms of what businesses expect. Businesses think inflation will be at 3.1% over the next year which is down from 3.5% in the prior survey. They also edged 2-year expectations two-tenths lower to 2.5% and 5-year expectations down by one-tenth to 2.4%. Chart 3. These are all still in the upper half of the BoC’s 1–3% inflation target range. Businesses also reduced how much upside they think will unfold as the share of businesses who think inflation over the next two years will average above 3% fell to 40% from 54% and instead moved up the share of businesses in the 2–3% camp from 39% to 54% (chart 4). The share in the 1–2% range remained inconsequential at 3%. Also note that the share of businesses planning more frequent than normal and bigger than normal price increases fell for a third straight quarter.

- The business survey also edged up expectations for sales growth over the next year, raised their intentions to invest in machinery and equipment, signalled more hiring than in the last survey, signalled a little more difficulty meeting an unexpected increase in demand due to capacity pressures with the highest reading on this count since Q1 of last year, fewer labour shortages but slightly more intensity of those shortages, and slower wage growth than in the past year albeit still at about double the BoC’s inflation target. That last measure is garbage; businesses have been saying one thing on wages while doing the opposite in raising them.

Now, one of these centuries we will get fresh data on Canadian wage settlements and this will help to further inform my point about how consumers don’t believe in 2% inflation and are changing their behaviour through wage setting exercises. It’s April, however, and we still only have data up to November. Spring is in the air, but Ottawa’s data collectors still haven’t entered winter. From my understanding, the delay is not at the analyst level as the data was submitted for publication a long time ago. So what’s the hold-up? Bureaucracy? IT? Politicians? It would be helpful to have this information before the next BoC meeting one week tomorrow. It should not take this long and it’s a disservice that should be rectified by perhaps having Statcan take it over.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.