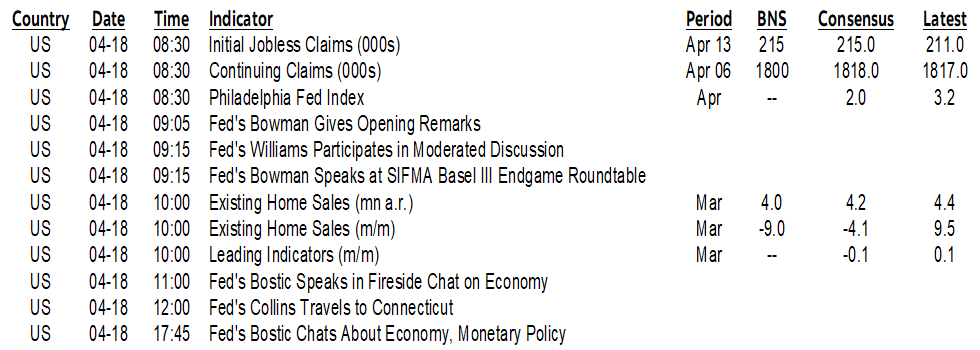

| ON DECK FOR THURSDAY, APRIL 18 |

KEY POINTS:

- Falling oil prices buoy bonds and equities

- Oil prices continue to slip, but will it last?

- FX markets post little reaction to G7, Asian jawboning

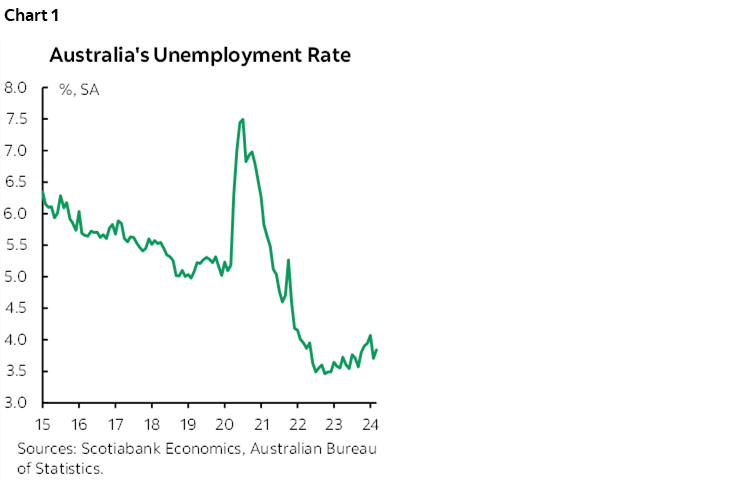

- Australia’s job market stopped to take a breath

- US to update a handful of minor releases

- More Fed-speak on tap

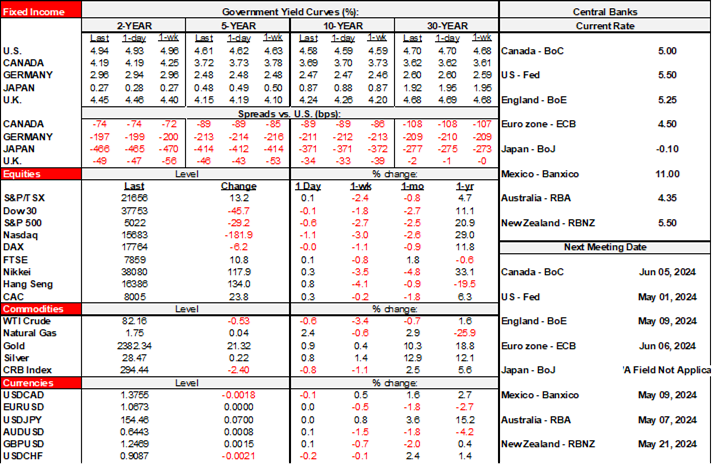

Stocks are mostly gaining across U.S. futures and European cash markets except for flat TSX futures and the Dax. Sovereign bonds were very slightly richer across US Treasuries and longer-dated EGBs but have since moved to being little changed. Gilts are outperforming except against most except Antipodean benchmarks following a soft-ish Australian jobs report. Weaker oil prices are somewhat helping perceptions of inflation risk, for now.

Antipodean Curves Outperform as Australian Jobs

Australia lost a small number of jobs last month (-6.6k) as a 28k rise in full-time jobs was offset by a 35k drop in part-time jobs. It’s hardly a bad report in the wake of 118k jobs that were added the prior month, most of which were full-time! The result edged the unemployment rate a tick higher to 3.8% as the participation rate ticked lower to 66.6%. The UR has been slightly but steadily trending higher (chart 1). Australia’s 2-year yield fell about 5bps post-data through the overnight session. A decent shot at an RBA rate cut starts to get priced by the August meeting but not even the final meeting of the year in December has a full quarter point rate cut priced.

Oil Prices Continue to Weaken

Oil continues to fall in the wake of yesterday morning’s US crude oil inventories release that showed about double the pace of increase that was expected. Since then, WTI has slipped by about US$2–3 which seems like an over-reaction. The perception that Middle East tensions have subsided is also weakening oil prices, until the next flare-up…

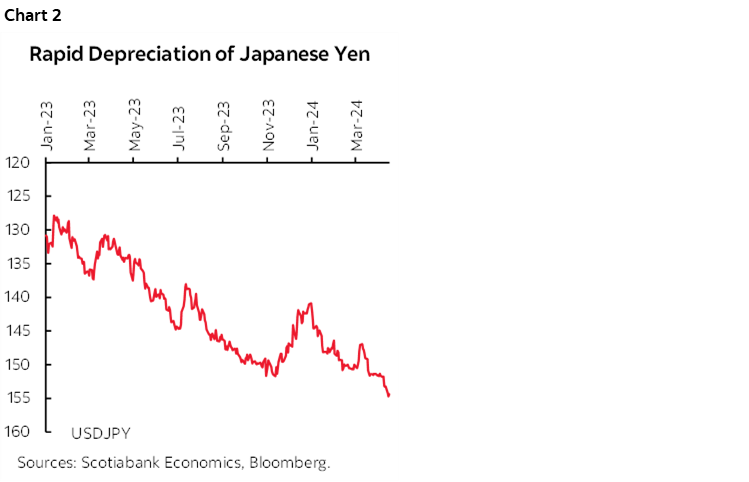

FX Markets Have Minimal Response to Jawboning

The possibility that the Fed might not cut at all this year has policy officials a tad spooked elsewhere. The strong dollar is the chief concern and, by corollary, their own weak currencies. The G7 statement that was issued yesterday (here) and the joint statement issued by the US, Japan and Korea (here) expressed concern about disorderly movements in markets with particularly emphasis upon the concern being expressed about the strong USD. The latter statement noted:

“We will continue to cooperate to promote sustainable economic growth, financial stability, as well as orderly and well-functioning financial markets. We will also continue to consult closely on foreign exchange market developments in line with our existing G20 commitments, while acknowledging serious concerns of Japan and the Republic of Korea about the recent sharp depreciation of the Japanese yen and the Korean won.”

What is to be debated is whether the USD is too strong relative to other currencies and how to define disorderly movements. As the Fed gets pushed out with the possibility of no easing this year, the USD has significant wind in its sails alongside the uncertainty into the US election. Whether Asian governments can really do much about it on a sustainable basis is the other key question and I doubt it. The won appreciated overnight while the yen posted little reaction in the wake of its massive depreciation to date.

Minor Developments into the North American Open

A few minor US releases are on tap into the U.S. session including the Philly Fed’s measure for April that feeds into ISM-manufacturing expectations (8:30amET), weekly initial jobless claims (8:30amET) and existing home sales for March (10amET). Several Fed-speakers will also offer remarks throughout the morning. Canada goes quiet. Tomorrow will also present a quiet N.A. calendar.

As for N.A. earnings, there will be 11 S&P500 companies releasing today but with few notable names.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.