| ON DECK FOR WEDNESDAY, APRIL 17 |

KEY POINTS:

- Markets stabilize following the week’s key developments

- Forget the Fed in June and maybe longer…

- …as Powell sounds less confident about hitting inflation goals

- Powell revealed Fed economists’ estimate for core PCE

- BoC’s Macklem signals more confidence but requires more evidence

- Sell Canada? Hiking taxes on capital gains is exceptionally unwise

- Gilts underperform as UK core CPI surprises higher

- BoE’s Bailey to speak, armed with updates on jobs, wages and inflation

- BoE’s Greene and Haskel on tap

- NZ rates curve sells off as a domestic inflation gauge rises

- ECB’s Lagarde probably won’t say anything new today

US Treasuries are catching a mild bid this morning in a partial reversal of the week’s sell-off that was driven at first by US retail sales and then by Chair Powell’s guidance against nearer term cuts. Gilts are underperforming on the back of a mild upward surprise in core inflation. Oil is slipping again with WTI and Brent down by just under 1% on the hope that Middle East tensions have subsided at least for now; we’ll see. The USD is broadly softer. Stocks are mostly higher.

GILTS UNDERPERFORM ON MILD CORE CPI SURPRISE

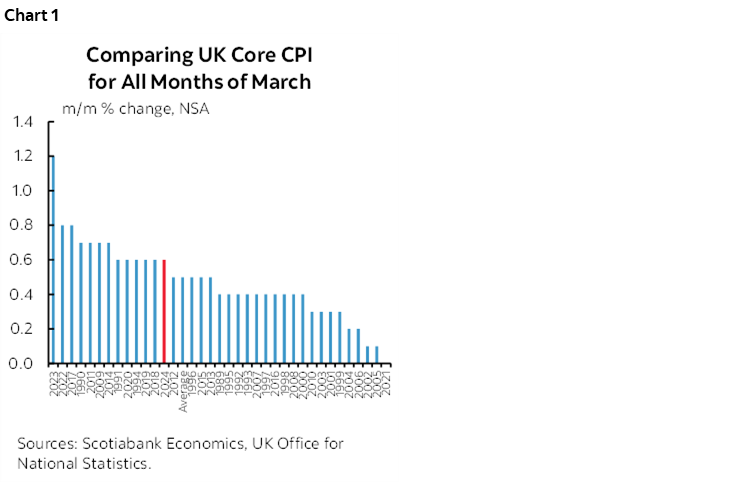

UK CPI surprised a little higher than expected overnight. Core CPI was up by 0.6% m/m NSA which was slightly firmer than the historical seasonally unadjusted (NSA) average for the month of 0.5% (chart 1). This follows a similarly slightly hotter than normal m/m core CPI NSA reading for February. The result was to support the year-over-year rate a little more than most had anticipated (4.2%, 4.5% prior, 4.1% consensus).

BoE OFFICIALS TO REACT TO RECENT DATA

Now it’s over to Governor Bailey to share his freshened thoughts and perspectives when he speaks at the Institute of International Finance at noon ET today while attending the IMF/World Bank Spring meetings in Washington. Deputy Governor Megan Greene speaks before him at the same event at 8amET. The BoE’s Haskel speaks at a separate event at 2pmET. Each of them will have an opportunity to reflect upon whether or not hot wages and another slightly warmer than usual core CPI print change anything relative to market pricing for a first cut by the BoE later this summer and as early as partial pricing for the August meeting.

ECB’S LAGARDE IS UNLIKELY TO REVEAL ANYTHING NEW

ECB President Lagarde speaks at 2pmET but may be somewhat less impactful than Bailey given that the ECB updated its communications last week.

NZ RATES RISE AFTER KEY INFLATION GAUGE INCREASES

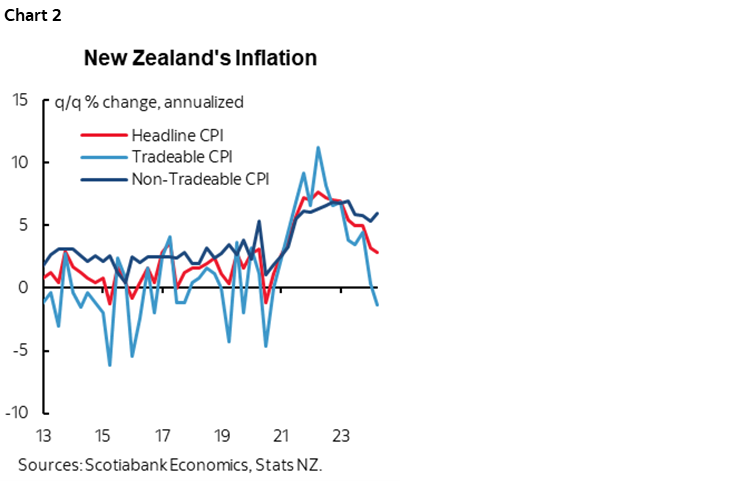

The kiwi 2-year yield spiked about 6bps higher after a key domestic measure of price inflation increased. New Zealand’s total CPI landed on the screws at 0.6% q/q SA nonannualized and 4% y/y in Q1. Tradeable goods CPI—which more directly reflects imported items and commodity influences—was down -0.7% q/q but non tradeable CPI—that more directly reflects locally produced goods and services—was up 1.6% q/q (chart 2).

A LIGHT N.A. SESSION AHEAD

The N.A. calendar faces light developments today. Canada will focus upon the aftermath of the Budget and Governor Macklem’s comments with nothing further ahead today. The US will monitor the Fed’s Beige Book (2pmET) and then Treasury market participants will keep an eye on February figures for TIC flows (4pmET).

POWELL DAMPENED RATE CUT EXPECTATIONS

Federal Reserve Chair Powell crushed pricing for any near-term rate cuts when he said two things during his panel appearance with BoC Governor Macklem yesterday. Here’s what he said:

"Recent data have clearly not given us greater confidence and instead indicate it will take longer to achieve" 2% inflation and showcase "a lack of further progress on returning our 2% inflation goal."

And

"It's appropriate to let restrictive policy further time to work."

Markets are pricing holds on May 1st and June 12th and about half of a quarter point cut at the July 31st meeting. Markets are also pricing less than a half point cumulative cut into year-end.

POWELL REVEALED THE FED’S CORE PCE ESTIMATE

Powell also revealed what Fed economists estimate for next week’s core PCE when he said it is expected to come in unchanged at 2.8% y/y. Barring revisions, that implies m/m core PCE at 0.35% and hence on the border between 0.3 and 0.4. That, in turn, leans against some of the comments from other economists that suggest core PCE could come in as low as 0.2% m/m after core CPI landed at 0.4%. Fed economists proved to be on the mark the prior month.

BoE’S MACKLEM NEEDS MORE EVIDENCE

BoC Governor Macklem went in the other direction when he said the following things that indicate greater confidence in falling core inflation while they still seek evidence that this progress will be sustained.

"We don't have to do what the Fed does. We can do what Canada needs."

"Headline inflation came in close to 3%. Importantly measures of core inflation ticked down again. That does suggest that underlying inflationary pressures continue to ease."

"There are limits to how far the BoC can diverge from the Fed" but a flexible exchange rate gives Canada flexibility to conduct policy somewhat independently from the Fed. That suggests he’s not fussed by letting CAD fall even further.

“We're looking for evidence that this will be sustained."

CANADA’S CONFISCATORY TAX HIKE

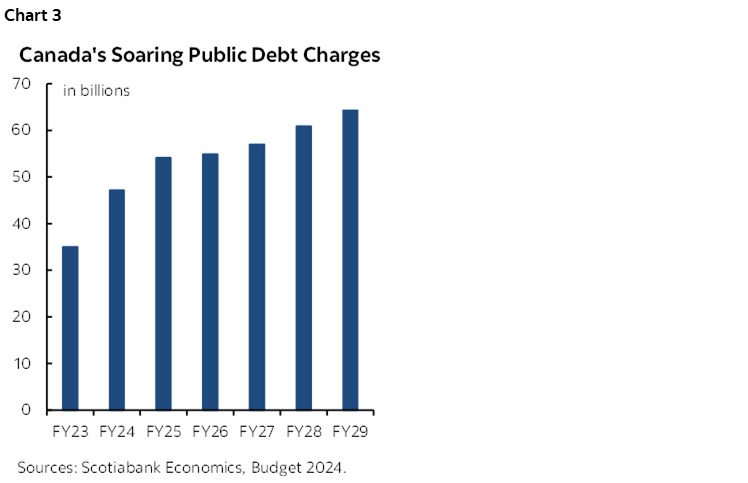

Canada’s Budget basically cements structural deficits forever as the interest charges on Federal government debt soar to over C$65 billion per year (chart 3). Trudeau Jr is clearly following in the footsteps of his father and aided by a highly complicit Finance Minister. If Canada stumbles into a worse economy than the rosy scenario laid out in the Budget for the next five years, then deficits will balloon, debt will rise even more, and the optimistic yield curve forecasts contained within the budget will deliver even more money paid to bondholders instead of other priorities.

That, folks, is not being generationally fair. Trudeau and Freeland are ripping off Canada’s youth who will be the ones left to face the bills for many years to come. It’s an insult to portray such a Budget as being in the best interests of Canada’s youth who have fled from the Liberals in droves.

Nevertheless, the show stealer in yesterday’s Canadian Budget was that Canada dramatically jacked up capital gains taxes and that merits fuller treatment. Effective June 25th, capital gains taxes will rise in the following ways:

- For individuals, the inclusion rate on capital gains above C$250k will be hiked from 50% to a whopping two-thirds before then multiplying by one’s tax bracket. Capital gains below C$250,000 will continue to be taxed at the 50% inclusion rate times the marginal rate.

- For ALL companies and trusts, the capital gains inclusion rate will rise to two-thirds from 50%.

- Small businesses are once again treated preferentially with a lifetime capital gains exemption that has been raised to C$1.25 million from C$1.016 million, but unevenly applied which is sparking pushback. Above C$1.25 million of capital gains triggers the higher inclusion rate, therefore why the government calculates that targeted small businesses with less than C$2.25 million in capital gains will be better off on net but above that they will be worse off.

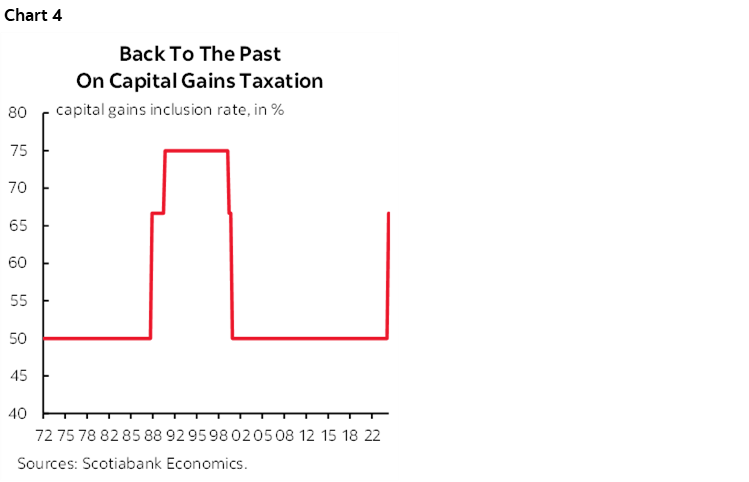

I’ll share the following thoughts on various aspects of this unwise move that take Canada back to when capital gains were taxed more heavily decades ago in the aftermath of 2+ decades of irresponsible fiscal policy (chart 4).

1. Why They Did It

The capital gains tax hike is estimated to raise about C$6.9 billion in the dying days of FY23–24 as investors are assumed to be in a rush to sell and just under $20 billion over the full five-year planning horizon. This is a massive tax grab, but how did they come up with the estimate especially for this year?

It’s simple. $6.9 billion was the magical plug figure to avoid having to break Minister Freeland’s promise to keep the deficit under C$40.1 billion this year in the wake of all of the heavy spending that has been announced at various photo ops of late. They are taxing savings to fund more program spending. Her numbers just barely achieve that promise, unless their revenues disappoint. Stay tuned. One possibility is that perhaps investors may defer realization of capital gains on the hope that a more sensible government will cut the inclusion rate in future which would in turn probably have to be accompanied by sharp cuts to program spending and the bloated Federal civil service that escaped yesterday’s Budget largely unscathed.

2. The ‘Fairness’ Fallacy

Minister Freeland says that a dramatic hike in capital gains taxation is motivated by the pursuit of tax fairness. She likes to argue that some earners can pay more in taxes than millionaires and billionaires because people who earn their income primarily from employment can get taxed at higher rates than people who earn more of their income from capital gains. This is a favourite argument of the left, of which Minister Freeland is a champion along with the NDP that has never heard of a reason to tax and spend idea that it didn’t like.

And yet at one time or another folks who used their savings to buy assets that hopefully generated capital gains were first taxed on their employment income and very possibly at the highest marginal rates of taxation.

Then they invested those after-tax savings into companies whose profits—if generated—were then taxed at relatively higher rates in Canada than the US.

Then companies that invest their after-tax profits into assets that generate capital gains will now have them taxed at a much higher inclusion rate of two-thirds and again taxed at higher rates of corporate taxation than the US.

Shareholder distributions out of any profits that remain through dividends and/or capital gains will be taxed again in the hands of the individual investor, the latter now taxed at more punitive levels.

Canada will now penalize capital gains with higher taxes than most other countries in the world (here).

Government has taken a slice at every stage of the wealth creation chain and that, dear reader, is where the total lack of fairness comes in.

And so I ask you why would you save and invest in such a country that penalizes work, effort, saving and investment at every possible stage? It’s confiscatory taxation. It’s a reason to sell Canada on top of other challenges such as overall competitiveness.

3. The Small But Mighty Few

The government downplays the tax hike by saying only an estimated 40,000 Canadians have capital gains of above $250k.

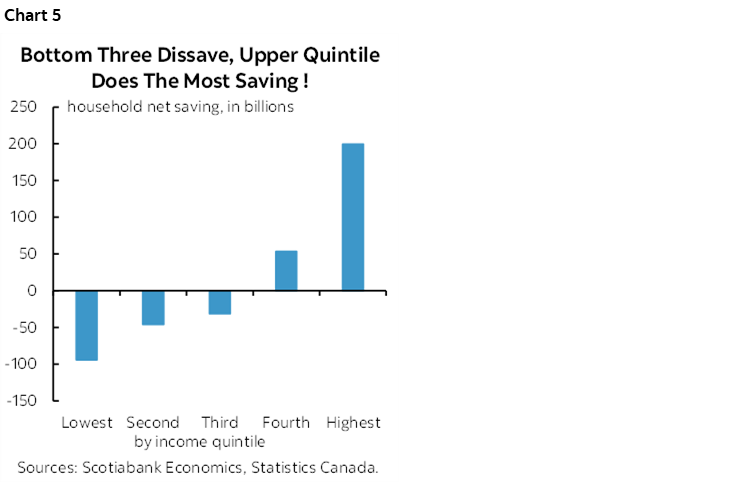

And yet the reality is that most saving in Canada is done by wealthier households that represent a minority of the population. Chart 5 shows that lower income cohorts dissave on net, leaving the supply of household savings to be delivered by relatively wealthier households.

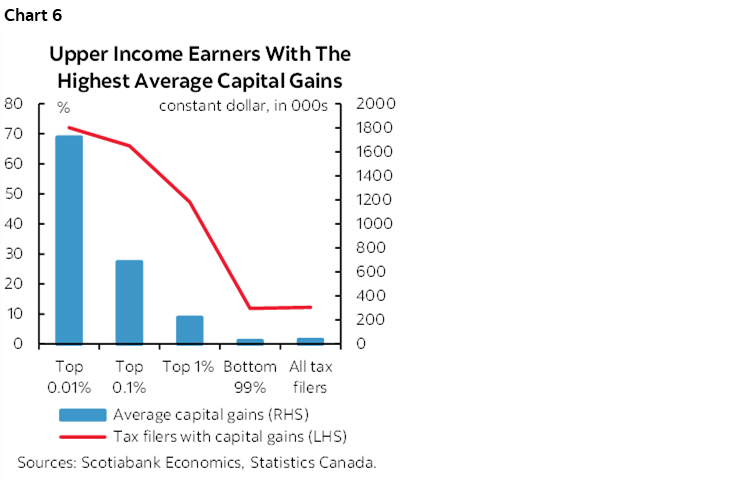

Capital gains are an extension of this. Chart 6 shows that the vast majority of capital gains are indeed held by relatively wealthy households that do the investing. Those who save more generate more capital gains. This saving and investing from a relatively few is important to funding investment.

Targeting the households with the gains is not only an unfair approach that applies tax upon tax upon tax as already explained, but it also strikes to the heart of the reality that the Canadian economy needs savings and it’s the relatively wealthy that now have less incentive to save—or more incentive to move those savings out of the country.

4. Canada is Diverting More Savings to Current Government Consumption

In jacking up taxes, Canada is using the proceeds to fund more government spending on shiny, flashy things that meet political goals. Not only does the government take from incomes, they are now digging deeper to take more of your savings to fund their spending.

5. Forced Selling

Who benefits here? The folks who will generate commissions and fees related to any forced selling of assets ahead of the June 25th implementation in order to avoid the higher capital gains inclusion rate that kicks in afterward. That could put pressure upon CAD, credit, equities, non-primary housing, and commercial real estate.

6. Internationally Uncompetitive

Canada is now decisively uncompetitive on taxes. This international summary of capital gains taxation would now probably put Canada toward the top of the list of high rates alongside having lost its relative advantage on corporate taxation to the US about six years ago. This will harm Canada, whatever the left thinks which isn’t very much imo.

7. Someone Else Will Pay

A cardinal rule of tax policy is to consider that the initial target won’t necessarily be the one who ultimately bears the burden. Tax incidence effects entail assessing on whose shoulders higher taxes will fall. Higher capital gains taxation will ultimately be paid for by a combination of stakeholders from investors to workers to consumers and other businesses.

8. A Fundamental Shock to Trusts

Family tax planning took a major blow in the Budget because of the hike from 50% to two-thirds for the capital gains inclusion rate applied to trusts. Trusts are used by families to bequeath assets resulting from investments that have been taxed at multiple stages to future generations. In some cases, this can help those future generations cope with strained housing affordability.

Raising capital gains taxation is likely to further incentivize movement of savings out of Canada into lower taxed jurisdictions, like the long list of other countries that won’t tax capital gains at the same punitive rate Canada will going forward.

9. Vacation and Other Properties at Risk

About that family cottage you bought years ago, perhaps many years ago. Even if you planned for the tax burden that would be triggered for one reason or another, the tax burden just went up by quite a lot. Ditto for any non-primary residence. Two-thirds of that capital gain will now be taxed at whatever relevant marginal rate versus 50%. That could be exceptionally unfair to many households that don’t have the cash flow to foot such a higher bill in relation to their retirement needs. The same applies to investors who have provided capital to the condo market to feed rentals after decades of ill-advised rent controls destroyed the availability of affordable apartments.

10. More risk aversion

Less reward after-tax is likely to discourage risk-taking. Discourage investment. Discourage anything that might address Canada’s productivity problems.

11. Just Plow it All Into Housing

In the short-term, dramatically raising capital gains taxation may encourage more dumping of various assets like non-primary housing including many condos before the highest capital gains rate kicks in. But then what happens? The tax incentives to invest have been tilted even more toward illiquid housing and away from other investments that might have helped to generate greater productivity and improvements in longer-run living standards as opposed to current consumption.

In short, the government is using tax policy to dramatically favour further investment in housing and thereby encourage purchase of bigger, more expensive homes at the expense of diversification. At least for now. I still worry about how the Trudeau Government began collecting data on home sales with your tax filings starting years ago. They are establishing the infrastructure to maximize future policy flexibility toward the tax treatment of home equity. Would this government, for instance, tax home equity gains on primary residences held by relatively wealth folks? I wouldn’t trust them.

12. Trapped Gains

Higher rates of capital gains taxation can result in trapped capital. The decision to take profits on gains can be negatively impacted by higher taxation of capital gains. The result can be that capital is inefficiently tied up for longer than is optimal instead of being redeployed more rapidly toward more profitable purposes.

Furthermore, the discrete jump in the capital gains inclusion rate from 50% to two-thirds at the C$250k gains trigger point will create a barrier to growth and incentivize efforts to avoid the jump.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.