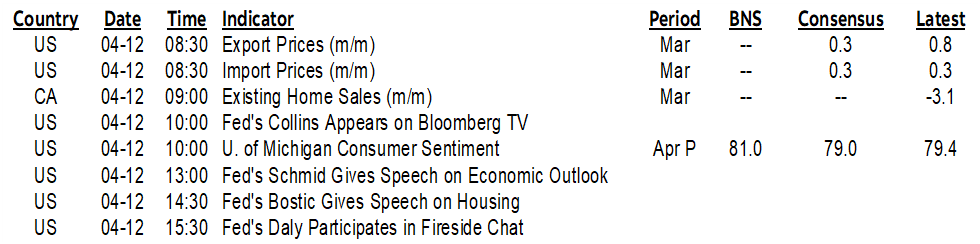

| ON DECK FOR FRIDAY, APRIL 12 |

KEY POINTS:

- Guarded markets don’t like the start of the US bank earnings season

- UK economy rebounds, markets ignore

- Peru surprises with a rate cut

- BoK takes a dovish step forward

- Riksbank priced to cut next month post-CPI

- Chinese financing was strong last month, exports were not as bad as they looked

- Distorted Canadian home sales probably softened last month

- Ottawa’s mortgage easing will add more demand pressure…

- ….and worsen housing affordability after a first-mover advantage…

- …while further reducing the room for the BoC to cut rates

- Canada’s housing obsession comes at a high and rising cost

- Ottawa very likely to raise taxes next week

The main focus to end the week is the start of the fiscal Q1 US bank earnings season and developments in oil markets. Markets are guarded with sovereign bonds richening, US equity futures a little lower and the dollar stronger across the board. Oil is up on a report that a strike by Iran against Israel is likely into this weekend.

Markets Don’t Like US Bank Earnings

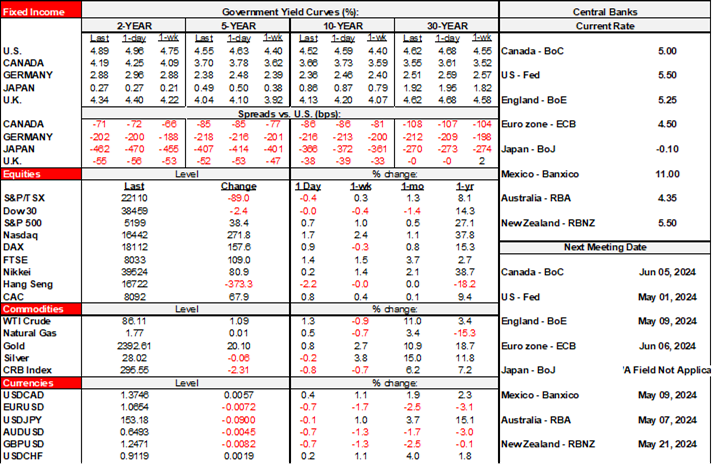

Markets are not liking US bank results so far. JP Morgan appeared to beat on revenues and EPS this morning but details like net interest income drove its share price lower in the immediate aftermath. The market also didn’t like Wells Fargo’s earnings. State Street disappointed on earnings but markets drive its share price higher as its NII beat. Citigroup beat on earnings and revenues and markets lifted its shares. Beyond earnings, the US also updates UMich sentiment including measures of inflation expectations this morning (10amET).

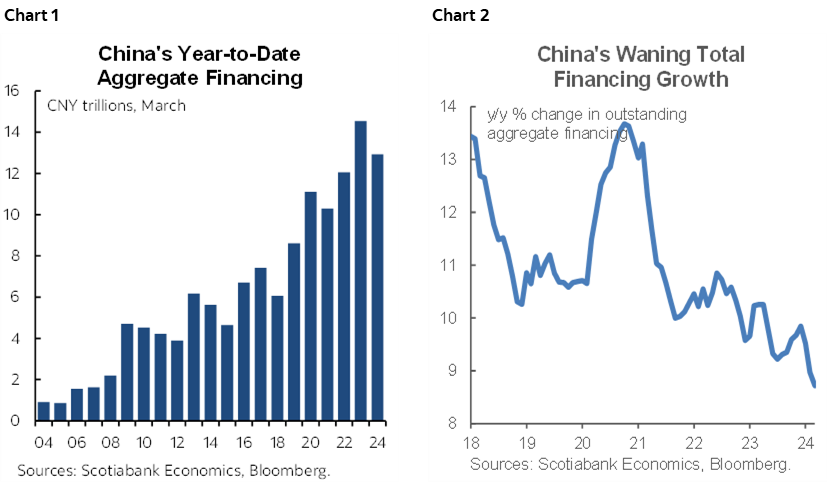

Chinese Financing Was Strong, Exports Soft

China updated total financing figures this morning. They were strong for the month of March and are driving the second fastest rate of expansion on record in year-to-date flow terms (chart 1) while the percentage growth rate in outstanding amounts across all financing products continues to wane (chart 2).

Chinese exports were weak last month in y/y terms but base effects from a year ago, shifting timing of the annual Lunar New Year and its effects on production, and currency valuation effects merit caution in interpreting the figures. Exports were down 7.5% y/y in USD terms and -3.8% in yuan terms. In m/m terms, exports were up by 27% and imports were up by 22.5% as they rebounded from Spring festival shutdowns.

Regional Central Bank Developments

Data and regional central banks are spicing up some currency and rates moves.

- Peru’s central bank delivered a surprise rate cut of 25bps that brought the reference rate down to 6%. Only one out of 13 economists in Bloomberg’s consensus got the call right. The central bank dismissed recent upward pressure on inflation as—brace yourself for the ‘T’ word—transitory. Not that word again…

- The Bank of Korea held its base rate unchanged at 3.5% as universally expected. The won weakened after Governor Rhee Chang-yong said that if inflation declines as they forecast over 2024H2 then they could cut, and the statement replaced reference to restrictive rates for a “sufficiently long” period with just a “sufficient” period.

- Riksbank watchers got a treat this morning. A considerably weaker than expected inflation reading for March (0.1% m/m, 0.4% consensus) including underlying inflation (0.1% m/m, 0.4% consensus) drove the krona to be the worst performer to the USD across majors and semis, while Sweden’s rates curve is outperforming everyone else’s with double digit basis point declines across maturities. Markets are now mostly pricing a cut at the May 8th meeting.

The UK Economy is Rebounding

UK macro data for February was mostly a little better than expected but largely ignored by markets. GDP was up 0.1% m/m as expected but revised up a tick to 0.3% the prior month. The UK economy has grown in back-to-back months and three of the past four. Industrial output strongly beat at +1.1% m/m with minor revisions. A services index was up0.1% (0% consensus) with a slight positive revision. Construction output disappointed at -1.9% m/m (-0.4% consensus) as it reversed the prior month’s gain. Exports slipped (-0.1% m/m) and imports were flat.

Distorted Canadian Existing Home Sales May Have Temporarily Softened

Canadian existing home sales might decline for the month of March over February when the figures are released at 9amET. I would dismiss a soft patch after strong sales in January and February and ahead of a probably strong Spring market over April to June. March break and an earlier than normal Good Friday holiday weekend likely robbed realtors of sales that would have otherwise occurred. Fear not in any event, as Ottawa is rolling out even more housing stimulus between yesterday’s announcement and another one that is expected today.

Canada Massively Eases Mortgage Financing—The Short and Longer Run Effects

Canadian Finance Minister Freeland announced a material easing of mortgage lending terms yesterday (here). The measures will drive more demand into a market with deep supply shortfalls and will worsen housing affordability over time. They are likely to add to housing’s contributions to GDP growth. There may be significant unintended consequences that also arise from the changes. Further housing measures are expected to be announced today by Canada's Minister of Housing etc, Sean Fraser. Make little mistake, these measures are political and designed to address the federal government’s sagging appeal to younger Canadians—note the way they were delivered—on the assumption they won’t grasp the economics of the likely outcomes.

Here’s what was announced:

- The mortgage amortization period for insured mortgages taken out by first time homebuyers buying newly built homes including multis was raised from 25 to 30 years effective August 1st this year. At least that part is out of the Spring housing market, but that was probably intended to support home sales into an election year instead of just now.

- The withdrawal limit for the Home Buyers plan is being raised from $35k to $60k effective on Budget Day next week. The HBP can be combined with the Tax-Free First Home Savings Account that allows contributions up to $8k per year to a lifetime limit of $40k.

- HBP participants between January 21st 2022 and December 31st 2025 are now allowed an extra 3 years to repay the amount to their RRSP for a total of five years.

- Lenders will now have to contact borrowers up to 24 months in advance of a renewal, imposing further regulatory costs.

- Temporary amortization extensions in the face of mortgage resets will now be possible to make permanent for all homeowners without fees or penalties. For example, a 25-year insured mortgage holder that temporarily extends to 35 years won’t have to renew back at the original 25 years and can now, depending on circumstances, make this extension permanent.

Some folks will stand to benefit from these changes but it’s vital to point out the following:

- The last thing that the housing market needs is more demand pressure on top of wildly excessive immigration, little supply, and a strong job market. This will complicate efforts to have supply catch up on the heels of the latest solid attempt (here) at estimating the gigantic shortfall of housing that existed even before these recent measures. Ottawa continues to pursue an odd mixture of demand and supply measures that are conflicting with one another if the goal is to improve affordability over time.

- Added housing demand probably lessens prospects for rate cuts by the Bank of Canada and pushes them out. It would be unreasonable to throw rate cuts onto the housing market especially after Ottawa just threw jet fuel onto the market.

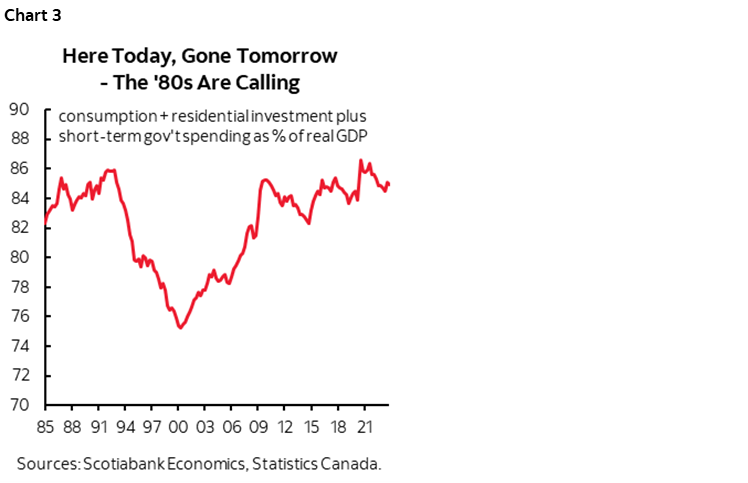

- As argued a couple of weeks ago (here) and previously, the more money and resources that get fed to the housing beast, the less that is available for addressing the nation’s productivity problem. There is evidence in the literature that housing plays a role in the productivity problem at home and abroad. With these measures, even more of the share of the economy will go to short-term spending including consumption, housing and short-term government spending (chart 3). That share is already running around its highest since the late 1980s and early 1990s when Canada was coming off of a major inflation and competitiveness problem.

- The conversion from temporary to permanent amortization lessens the impact of mortgage rate resets. That’s welcome to the affected folks who can lessen the near-term hit by taking longer to repay. It also means that the rate sensitivity of housing to BoC hikes has been dampened which could lessen the case for policy easing.

- The peak effects of these changes are designed to pump next Spring’s housing market in an election year more so than this Spring’s market. That’s why they delayed the 30-year extension to August 1st. The HBP changes are effective next Tuesday, but I suspect that few first timers have $60k kicking around in their RRSPs to use in the HBP right away. They’ll reallocate savings and income over the coming year into RRSPs to get the tax deduction and then face the 90 day waiting period before they can withdraw the amount. The RRSP season could be pulled forward and amplified by these changes at least until the withdrawals hit.

- The extended amortization period and raised HBP withdrawals limits will bring more cash into the market to drive house prices higher. There will be a first mover advantage on the changes. Second and subsequent round effects will see higher house prices that eat away at the benefits of the changes for subsequent entrants who are likely to witness worsened affordability. All you have to do is plug some numbers into your handy dandy mortgage or bond calculations and see what happens to the extra amount of house that can now be purchased as a result of the changes; applying leveraged likely means an extra six figures of housing can be purchased. The hot air and ink that Ottawa spends on the importance of improving affordability through debatable supply side measures is in marked contrast to policies that have induced wildly excessive immigration, very strong government spending, and now easier mortgage terms. It’s an unparalleled lack of policy coordination.

- Because of the requirement that RRSP contributions cannot be withdrawn under the Home Buyers’ Plan for 90+ days, the effects of this change will occur in two or more stages. Those who already meet that criteria can start withdrawing the extra amount from next Tuesday onward. Anyone else will have to wait including people making fresh contributions that won’t be accessible until July.

- Extending amortizations to 30 years for new but not resale homes is a gift to builders who will capture some of the incidence effects through higher new home prices that through arbitrage may indirectly raise resale prices over time but by less and slowly. They can’t build enough homes fast enough due to skilled labour and materials shortages so prices and features will ration some of the demand. The flow through benefits will also go to folks building the homes and supplying materials.

- Only making 1st timers eligible will create unintended effects. It discriminates against other individuals already in the market who may be facing affordability pressures. It could also be gamed by, for instance, getting the first timer in a household to buy a home and not the one who already has title. Or parents can gift bigger RRSP contributions for the HBP eligibility.

- More people will be incentivized to make the minimum downpayment to get insured mortgages in order to secure the extra five-year amortization period. This will pivot demand more toward insured versus uninsured mortgages over time. Bear that in mind in terms of issuance volumes and market implications.

- Bigger withdrawal limits and longer repayment periods for Homebuyers' Plan participants amount to a wealth transfer from the future. More retirement savings will flood into housing and raise potential challenges later.

- OSFI’s efforts to tighten mortgage finance markets over the years just suffered a setback. Ottawa continues to pursue totally uncoordinated housing policies by stimulating more demand amid severe housing shortages and driving risk higher.

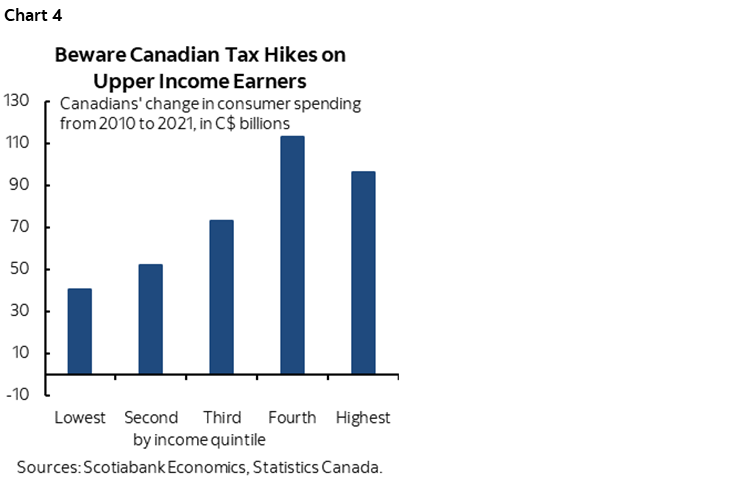

And on broader plans, Freeland reiterated that the deficit will not go higher and that they will respect the fiscal guardrails. Whether that means just the current ending fiscal year, the next one, or the full forecast horizon is unclear. But she did make it clear that higher taxes are coming for relatively higher income households and probably targeted industries. Asked if there will be any new taxes like a wealth tax, Freeland basically said yes there will be some forms of tax hike if you read between the lines. She only said that there will be no tax increases on whatever definition of the middle class they apply, but noted that they will make investments and campaigned on the basis of the relatively well off paying a little more. In plain speak, that means others faces tax hikes. As argued in this past week’s Global Week Ahead, raising taxes on relatively upper income earners could slow consumption growth into an election year and with it GDP growth given that most growth in consumption over time is driven by upper income households (chart 4). The net effect involves reallocating their spending toward funding high government short-term spending on social programs that Ottawa calls ‘investments’ instead of correctly labelling them as program spending.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.