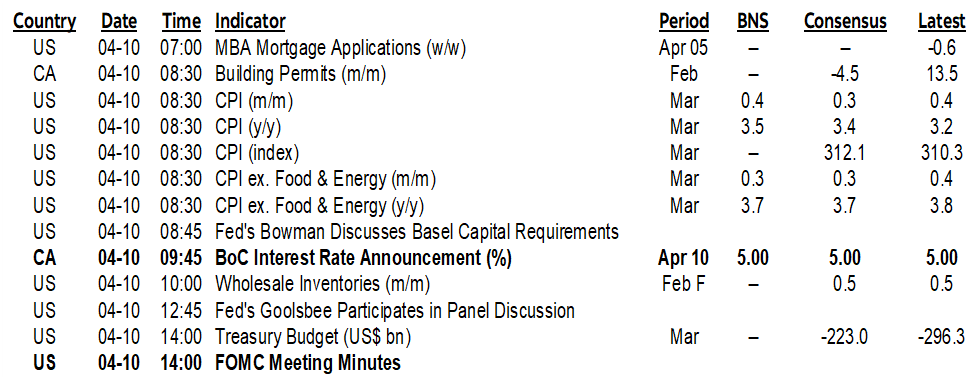

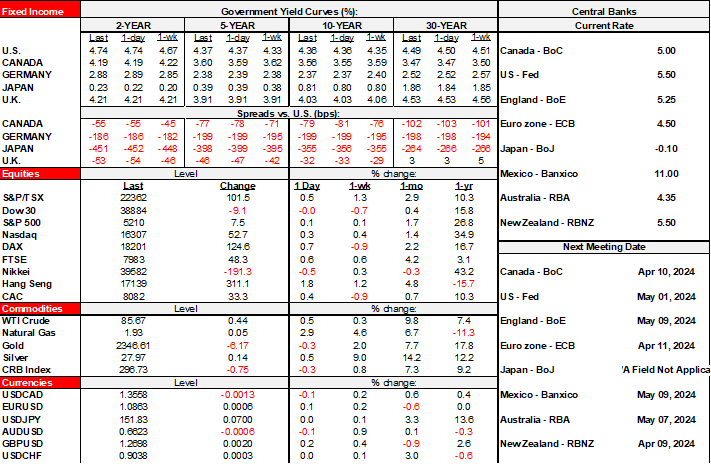

| ON DECK FOR WEDNESDAY, APRIL 10 |

KEY POINTS:

- Markets brace for potentially high volatility cycling through three key events

- US core CPI: A crowded field thinks this could be a fifth hot print

- BoC: Why it would be foolhardy to tee up June

- FOMC minutes to reveal further discussion on QT modalities

You won’t need coffee. The adrenalin rush should be enough today. Position squaring as markets roll through three key events in preparation for the next one could prompt high market volatility and mixed effects that may make it difficult to weed out individual influences. Fuller previews of what to expect for US CPI, the Bank of Canada and FOMC Minutes are in the Global Week ahead here.

US Core CPI—Another Hot One Could Kill Off June Pricing

March’s numbers land at 8:30amET to kick it all off. Everyone’s at risk of being wrong together. There is a remarkable coalescing of opinions around the magical number 0.3% m/m SA for core CPI. It’s where almost all economists reside, plus it’s what markets are pricing and what nowcasts are suggesting. That makes me nervous given what I know about the high uncertainty and missing components. Some drivers are discussed in my weekly.

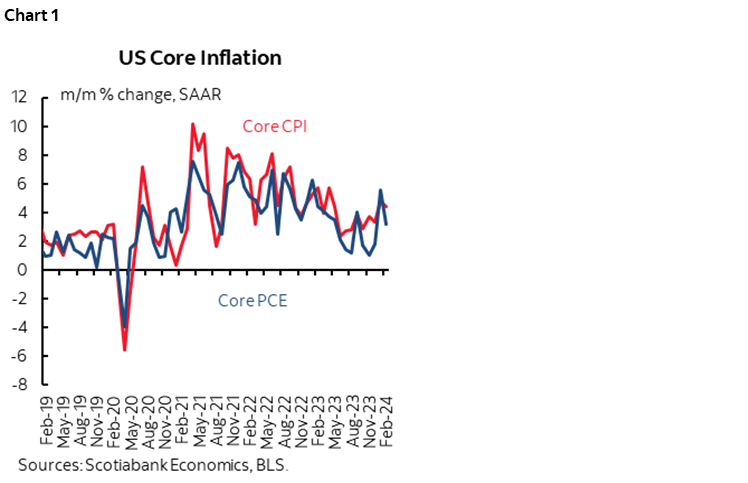

Another 0.3% or higher print would add to the four such readings we’ve gotten and further lessen the scope for a June Fed cut. Recall that core CPI was up by 0.3% m/m in each of November and December and then 0.4% in January and February. Using the exact figures and expressing them in m/m SAAR terms shows core CPI running at 3.8%, 3.4%, 4.8% and 4.4% from November to February respectively. That’s too hot for the Fed this far into a tightening cycle.

Of course, we all know it’s not CPI that matters so much to the Fed as it is their preferred PCE inflation gauges. On that count, the evidence is also sending warning signals, but over a shorter period (chart 1). Core PCE was up by 5.6% m/m SAAR in January and 3.2% in February but was one-handled in each of November and December. Whatever happens to core CPI will have to go through the data meat grinder to assess prospects for core PCE but the narrative doesn’t change much; after two hot months, any further pressure on core PCE could push cuts down and out while any relief could require more data.

Bank of Canada—Don’t Expect Firm Hints About June

The statement and Monetary Policy Report including fresh forecasts arrive at 9:45amET. Governor Macklem’s written opening comments to his press conference arrive at the beginning of the presser that starts at 10:30amET.

Please see my weekly for the fuller doves-versus-hawks cases and where I stand that won’t be repeated here.

On net, I’m not looking for any commitment to timing easing out of this one other than to repeat vague guidance that easing later in the year is feasible. Between now and the June 5th decision will see the release of two more CPI reports that could inform whether the last two were anomalies or that could extend the pattern and come closer to meeting the BoC’s criteria for a sustained period of softness. Five days before the June meeting will see the release of Q1 GDP growth that could be strong based upon current tracking and therefore provide an awkward backdrop against which to cut. There will also be further external developments such as another FOMC meeting and whatever happens to oil and the broader terms of trade between now and then.

In short, with all of that ahead of us before the June meeting, it would be foolhardy for the BoC to commit to the next meeting today.

Here are some additional things to watch for.

- Will they leave unchanged the reference to how they are “still concerned about risks to the outlook for inflation, particularly the persistence of underlying inflation” or soften it, perhaps by striking out the persistence part or softening it?

- I think they’ll leave intact reference to how they want “to see further and sustained easing in core inflation” and the references to what they are watching.

- They have to re-write the Canadian economy paragraph to recognize greater than expected strength and a stronger outlook partly based on greater fiscal easing and higher oil prices.

- On forecasts, I think they’ll revise up growth given tracking to date and more fiscal easing than they expected plus better terms of trade.

- They’ll probably leave intact the reference to how “underlying inflationary pressures persist” by quoting y/y core measures that are still over 3%. Mayyyybe they reference ‘signs of further progress’ or something like that. By contrast it would be hawkish if they referenced added upside risks to inflation and take your pick there (growth, oil, fiscal, etc).

- Watch for a staff research paper on the neutral rate and whether they raise their estimate. They have resisted in the past while saying it’s between 2–3% using four methodologies and with a 2.5% midpoint. Since then, Macklem and the since departed DepGov Beaudry have indicated they think it’s higher. A higher neutral rate would suggest they think policy may be slightly less restrictive.

- Also watch how they may revise potential GDP estimates. They may revise up the level, but the growth rate could be revised down.

FOMC Minutes (2pmET)

Any rate dialogue may be stale on arrival post-payrolls and wages and depending in part on what happens to core CPI. The QT discussion may inform what they are thinking of by way of the modalities, but we were told that no decision was reached at this meeting. Powell had said that a decision may be offered “fairly soon” back on March 20th which is open to interpretation. The minutes might inform how close they are to a decision and hence whether an announcement is likely on May 1st or June 12th.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.