ON DECK FOR FRIDAY, SEPTEMBER 29

KEY POINTS:

- Month-end is being kind to bonds and equities so far

- Eurozone core CPI was among the softest on record

- US core PCE could undercut core CPI

- Canadian GDP: Soft July, better August?

- US consumer spending and income probably posted decent gains

- German consumers retreated

- BanRep expected to hold

- China to update PMIs into the weekend

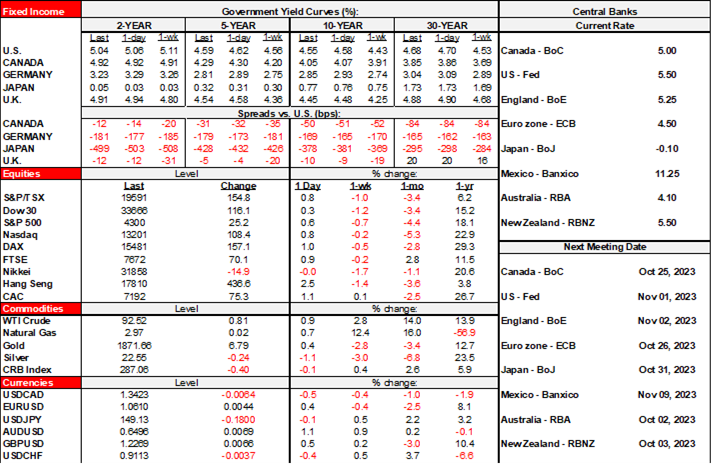

See ya, September! The month is going out on a bit more of a positive note following mutual sell offs in bonds and equities throughout much of the month. They’re both rallying this morning as we go into potential month-end rebalancing effects. Sovereign yields are down by 2–3bps across US Ts with gilts outperforming and EGBs even more so. Canada’s curve is slightly underperforming all of them. The dollar is weaker. The dollar is weaker. The dollar is weaker. I figured it was worth repeating what we haven’t heard much about of late. Most major currencies are up. Stocks are also broadly higher with N.A. futures gaining by around ½%, European cash markets up by roughly ½% to just under 1%. China and South Korea were both shut.

Now we’ll see if such moves hold up into data releases that are favourable so far.

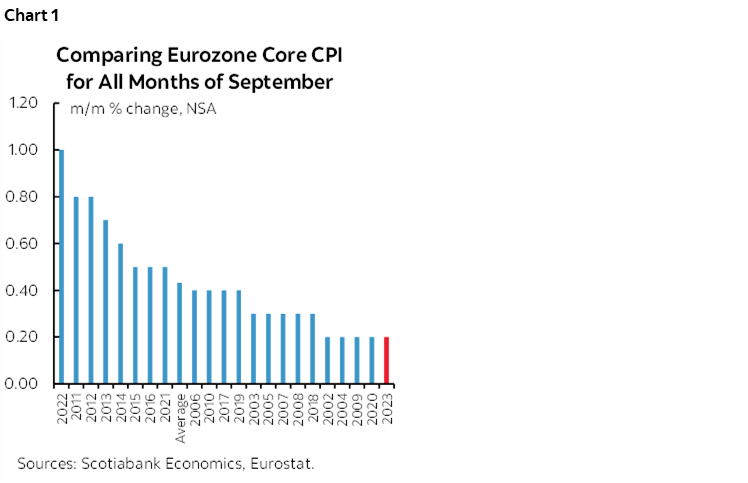

Eurozone inflation was softer than estimated in September. CPI was up 0.3% m/m (0.5% consensus) and 4.3% y/y (4.5% consensus, 5.2% prior). Core CPI was up 4.5% y/y (4.8% consensus, 5.3% prior). More important is that core CPI was up only 0.2% m/m NSA which is below average compared to other months of September in time which is the way to look at the seasonally unadjusted data. It was not only below average, it was way below average and one of the weakest on record (chart 1). In fairness, it’s just one month and nobody should overreact to this compared to a long string of readings that were hotter than typical like months in time. There remain legitimate concerns that wages and commodities will be passed through in second round effects on core inflation through winter months. So, rejoice for now, but be careful toward future months.

The results reinforced the drop in EGB yields that began unfolding just before France released ahead of the simultaneous release of the Eurozone add-up and Italian figures. Soft German data preceded the eurozone inflation figures that showcased weak German consume spending.

German retail sales volumes fell 1.2% m/m in August (+0.5% consensus) but part of the reason is that the prior month was revised up from a drop of 0.8% m/m to being flat, so a higher than previously understood jumping off point made it harder to post growth the next month.

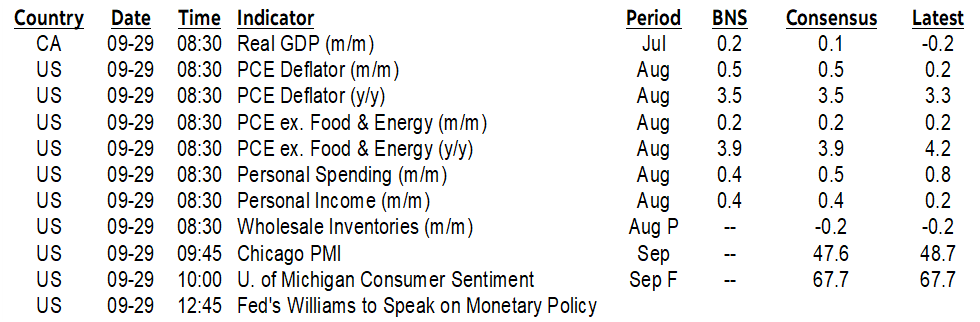

Canada and the US will release significant gauges into the N.A. session and ahead of Canada’s Federal holiday on Monday:

1. US core PCE (8:30amET): PCE’s lower weight on shelter’s solid rise in CPI could mean that August’s core PCE lands a little softer than the 0.3% m/m SA rise in core CPI earlier this month. There are several methodological differences between the two sets of inflation readings and the Fed’s preferred PCE gauge has tended to undercut CPI.

2. US consumers: Watch for solid nominal gains in income and spending in August’s data (8:30amET). I’ve estimated that the wages and salaries component should lead a 0.4–0.5% m/m gain in incomes with a similar rise in spending partly aided by what we know about retail sales but also by services spending not included in retail.

3. Canadian GDP (8:30amET): Estimates vary between 0% m/m and 0.2% m/m for July’s final reading after Statcan had previously guided on September 1st that July GDP was “essentially unchanged.” Since then, we’ve gotten a few releases like hours worked that suggest maybe there was mild growth. More important will be the flash reading for August GDP sans details. A strong rise in hours worked and the reversal of the drag effects of July’s BC port strike could pop August higher.

4. Colombia’s central bank is unanimously expected to keep its overnight rate unchanged at 13.25% this afternoon in the wake of Banxico’s hold yesterday afternoon (2pmET). They are not seeing the same traction on inflation as some other LatAm neighbours, like Brazil, Chile and Peru.

5. China updates its state PMIs tonight that may inform nearer term growth momentum but with any market reaction carrying into the Monday Asian open (9:30pmET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.